TODAY’S S&P 500 SET-UP - January 5, 2011

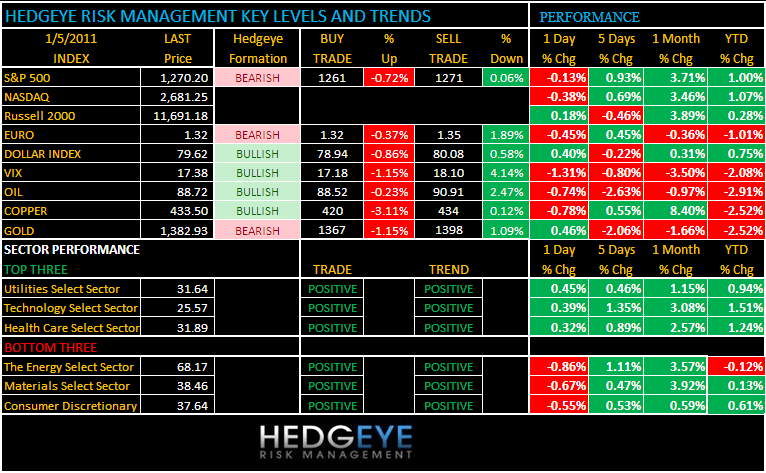

As we look at today’s set up for the S&P 500, the range is 10 points or -0.72% downside to 1261 and 0.06% upside to 1271. Equity futures are trading below fair value, tracking losses across Europe equities and a lower close among major Asian indices.

MACRO DATA POINTS:

- 7 a.m.: MBA mortgage applications, Dec. 31

- 7:30 a.m.: Challenger job cuts, Dec.

- 8:15 a.m.: ADP employment, Dec., est. 100k vs prev. 93k

- 10 a.m.: ISM non-manufacturing index, Dec., est. 55.7 vs prev. 55

- 10:30 a.m.: DOE inventories

- 11 a.m.: U.S. Fed to purchase $1.5b-$2.5b notes/bonds

- 11:30 a.m.: U.S. sells 56-day cash management bills

- 1 p.m.: Kansas City Fed President Thomas Hoenig speaks at Central Exchange in Kansas City

TODAY’S WHAT TO WATCH:

- Qualcomm may offer $3.5b to purchase Atheros, the NYT reported yesterday

- New Jersey Supreme Court will hear arguments today on whether the governor unlawfully cut $1b in school aid during a budget crisis

- Portugal sells EU500m of 6-month bills; avg. yield 3.686%; bid to cover ratio 2.6 vs prev. 2.4

- Republicans take control of the House today for the first time in four years, with plans to vote on a repeal of the health-care overhaul and to approve $100 billion in spending cuts

- Concho Resources (CXO) rated new buy at SunTrust Robinson Humphrey

- Danaher (DHR) rated new outperform at Oppenheimer

- Fluor (FLR) rated new outperform at Oppenheimer

- FTI Consulting (FCN) will take 4Q non-cash charge 36c to reflect retirement, write off of certain brand names

- Hatteras Financial Corp. (HTS) reported offering of 9m shrs

- MedAssets (MDAS) named Chuck Garner CFO, Neill Hunn unit president

- Mosaic (MOS) 2Q adj EPS, rev beat estimates

- Sonic (SONC) 1Q EPS ex-items 10c vs est. 10c.

PERFORMANCE: ALL 9 SECTORS BULLISH ON TRADE & TREND

- One day: Dow +0.18%, S&P (0.13%), Nasdaq (0.38%), Russell 2000 (1.59%)

- Last Week: Dow +0.03%, S&P +0.07%, Nasdaq (-0.48%), Russell (-0.67%)

- Month/Quarter/Year-to-date: Dow +0.98%, S&P +1.00%, Nasdaq +1.07%, Russell +0.28%

- Sector Performance - BEARISH (Only 3 sectors positive) - Energy (0.86%), Consumer Disc (0.55%), Materials (0.67%), Consumer Spls (0.27%), Financials (0.15%), Industrials (0.14%), Tech +0.39%, Healthcare +0.32%, Utilities +0.45

EQUITY SENTIMENT: MIXED

- ADVANCE/DECLINE LINE: -787 (-2556)

- VOLUME: NYSE 1090.34 (+2.84%)

- VIX: 17.38 -2.08% YTD PERFORMANCE: -2.08%

- SPX PUT/CALL RATIO: 1.50 from 1.41 (-6.40%)

CREDIT/ECONOMIC MARKET LOOK:

Treasuries were mixed with the belly of the curve outperforming. Some support was said to come from the pricing of corporate deals.

- TED SPREAD: 17.10 -0.203 (-1.173%)

- 3-MONTH T-BILL YIELD: 0.14% -0.01%

- YIELD CURVE: 2.73 from 2.75

COMMODITY/GROWTH EXPECTATION:

- CRB: 327.73 -1.59%

- Oil: 89.38 -2.37% - trading -0.95% in the AM

- Oil extended its biggest drop in seven weeks on signs that snowstorms in the U.S. curbed gasoline demand

- COPPER: 436.90 -1.99% - trading -1.01% in the AM

- Copper fell the most in 2 weeks - stockpiles are swelling

- GOLD: 1,376.65 -3.06% - trading +0.35% in the AM

- Gold tumbled the most in six months on speculation that an economic recovery will curb demand

OTHER COMMODITY NEWS:

- Gold Imports by India May Increase This Year on Rising Investment Demand

- At Least 40% of LME Copper Shorts in March Held by One Company, Data Show

- World Food Prices Surge to Record, Passing Levels That Sparked 2008 Riots

- Rubber Futures Climb to Record on Thai Supply Concerns Amid Strong Demand

- Palm Oil Slumps After Rising Above Soybean Oil First The Time Since 2007

- Oil Extends Biggest Drop in Seven Weeks as U.S. Gasoline Demand Slackens

- Copper Futures in London Decline for a Second Day as Record Deters Buyers

- Whole Milk Powder Auction Prices Climb to Three-Month High, Fonterra Says

- China Inflation Concern May Delay Coke, Lead Futures Launch, Analysts Say

- Oil Price Advance May Put Recovery at Risk, FT Cites IEA's Birol as Saying

- Steelmaking Coal Price May Exceed $300 on Australian Floods, Daiwa Says

- Gold Fluctuates After Slump Amid Signs of Economic Recovery, Rising Dollar

- La Nina Rains May Stretch Into March, Cause Further Flooding in Australia

- Europe Commodity Day Ahead: Gold Imports by India May Increase This Year

CURRENCIES:

- EURO: 1.3243 -0.45% - trading -0.54% in the AM

- DOLLAR: 79.444 +0.40% - trading +0.25% in the AM

EUROPEAN MARKETS:

- European Markets: FTSE 100: (0.55%); DAX (1.40%); CAC 40: (1.20%)

- European indices started the day mixed with a bias to the downside as an uptick in the US dollar hit commodity plays and profit taking.

- Financial stocks were also weighing on sentiment ahead of Portugal's €500M 6-month T-Bill auction.

- Investors were also looking to see what sort of market appetite there was for core European paper with the German Finance Ministry set to auction EUR5B of the on the run 10yr Bund.

- Some decent retail numbers from Next helped London to outperform.

- News that China was willing to buy more Spanish debt had little impact on the Spanish IBEX which was off (1.4%) while mixed Final Services PMI data for Dec offered only modest support.

- Continuing thin markets were blamed for some of the early volatility

- Domino's Pizza reports 13-week system sales +17.8% y/y to £132.5M

- German car manufacturers report US Dec sales, see double digit gains in US during 2010

- Eurozone Dec Final Services PMI 54.2 vs Prelim 53.7 and prev 55.4

- Eurozone Nov PPI +4.5% y/y vs cons +4.4% and prior +4.4%

- Eurozone Oct Industrial orders +14.8% y/y vs cons +17% and prior +13.5%

- Germany Dec Final Services PMI 59.2 vs Prelim 58.3 and prev 59.2

- France Dec Final Services PMI 54.9 vs Prelim 54.1 and prev 55.0

- UK Dec Construction PMI 49.1 vs Prelim 50.9 and prev 51.8

ASIAN MARKTES:

- Asian Markets: Nikkei (0.17%); Hang Seng +0.38%; Shanghai Composite (0.49%)

- Asian markets were mixed today, with resource stocks down on lower commodity prices.

- Taiwan the biggest looser down 1.68%, with Acer falling 4% after saying snowstorms in Europe will cause it to miss Q4 guidance.

- Hong Kong recouped early losses as some banks rebounded from a report that China might tighten some reserve requirements.

- China Eastern Airlines jumped early, but then lost almost all of its gain; saying it expects its 2010 net profit to be ten times that of 2009.

- Commodity stocks fell, but coking coal producers outperformed again on worries about the floods in Australia.

- Property stocks rallied on expectations the market will support higher prices.

- South Korea was -0.12%, with Tech and Financials down on profit-taking.

- Japan fell -0.17% - Steelmakers were hurt by an expected rise in coal prices due to floods in Australia. Megabanks fell on profit-taking.

- Mining stocks took Australia to a loss of 0.58%. Qantas lost early gains and finished 1% lower despite confirming it plans to resume A380 flights to Los Angeles by January 17th.

- Japan December monetary base +7% y/y to ¥104.02T.