The guest commentary below was written by Joseph Y. Calhoun, III of Alhambra Investments on 1/17/21. This piece does not necessarily reflect the opinions of Hedgeye.

What is the consensus about the economy today? Will 2022 growth be better or worse than 2021?

Actually, that probably isn’t the right question because the economy slowed significantly in the second half of 2021.

The real question is whether growth will improve from that reduced pace. The Atlanta Fed GDPNow tracker now has Q4 growth all the way down to 5% from the 6.8% rate expected just a week ago (a result of a less than expected retail sales report).

That’s still a pretty good rate of growth if it holds up, but my guess is that the final number will be somewhat less than that as the omicron wave took some juice out of the reacceleration from the end of Delta.

I think a decent estimate of second half 2021 GDP growth would be 3.5 to 4%. Interestingly, consensus for 2022 seems to be just about that range.

Morningstar’s estimate is 3.9%, S&P 3.9%, Kiplinger 4%, Conference Board 3.5%, Morgan Stanley 4.6%, Bank of America 4%, and Goldman Sachs 3.4%. So, the consensus, not surprisingly I think, is for more of the same. Most of Wall Street forecasting is just about this imaginative, by the way.

What about inflation? We just got the December report on CPI last week and the year-over-year change was 7.1%, a yearly rate not seen since 1982. The PCE deflator, the Fed’s favorite inflation gauge, was up 4.3% through Q3 2021 and will likely end the year around 5%.

The Fed believes this measure of inflation will fall to 2.6% by year-end 2022, which, if true, means either that their expected rate hikes really kill inflation or they won’t be hiking rates anywhere near 4 times this year. Morningstar has recently raised its estimate of 2022 inflation to 3.8%. Goldman Sachs is in line with the Fed with regard to PCE inflation. The general consensus seems to be that inflation will fall significantly in 2022.

Markets are busy validating this consensus right now. Interest rates, nominal and real, have risen over the first two weeks of the year, an indication that growth expectations have risen slightly.

And, yes, I’m aware others say that isn’t what it means, that rates are only up because of the expected change in Fed policy. Those same economic bears were happy to tell you how smart the bond market was when rates were going down and confirming their views.

I don’t think the bond market has gotten any dumber in the last few months. There is the matter of the yield curve and it is certainly not as steep as one bullish on the economy might like, but that game is far from over.

Whether it steepens or flattens from here depends on future changes in growth and inflation expectations as well as the impact of both on future Fed policy.

And inflation expectations have been falling since mid-November with 5-year breakevens now at 2.79%, 10-year at 2.44%, and the 5-year/5-year forward at 2.09%.

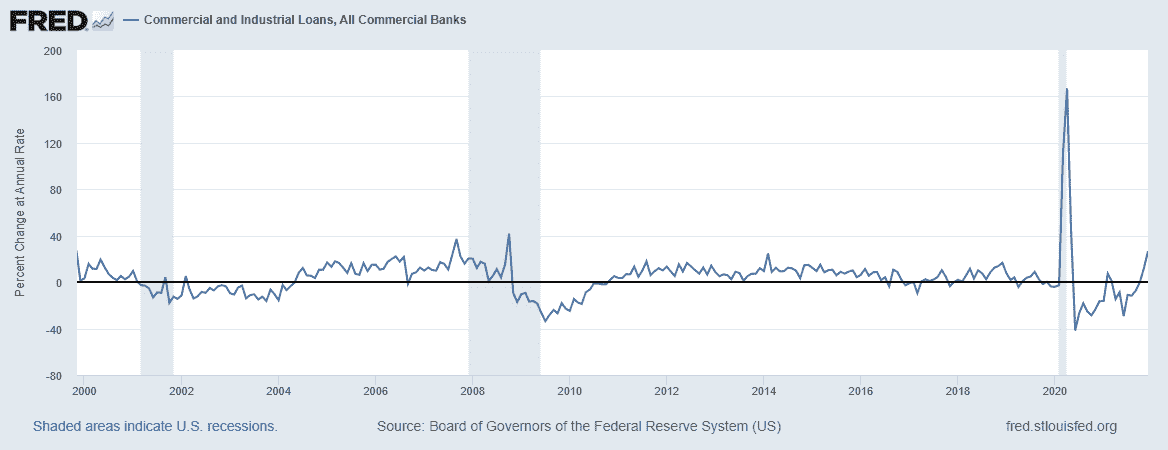

If we assume the current consensus will be wrong – and it rarely stays the same throughout the year – it would be nice to know how it might be wrong. Could growth be better than the expected 3.5 to 4% rate? There are some interesting items that could be pointing in that direction. For one, bank lending is finally turning up and looks a lot like what has happened in past cycles.

Commercial and industrial loans are rising at an annualized rate of 26.8%, a rate higher than any this century except right around recessions. C&I loans have risen in the last two recessions as corporations drew down credit lines to bolster liquidity.

Loan balances fell after each of the last three recessions and then resumed their previous trend higher. That appears to be what is happening now – unless you think we’re near recession right now.

Total loans and leases are also rising at a good pace, although moderating a tad last month:

If it is credit that has been missing from the expansion so far, that appears to be coming to an end.

Another, underappreciated positive is that US exports have recovered to a new all-time high. There has been a lot of attention on China recently and it is certainly an important economy. But China’s losses – many self-inflicted – may well turn out to be the gains of other emerging markets as manufacturing is shifted away from China.

Stock markets in Taiwan, Vietnam, India, and Mexico – all potential beneficiaries as other countries pull back from China – produced double-digit returns in 2021. Meanwhile, EU growth was similar to the US in 2021 and is expected to rise by 4% in 2022. Japan grew about 3% in 2021 but its success in containing COVID has them recently upgrading their outlook for 2022 to 3.2%.

The global recovery so far has been somewhat uneven with the US recovery the more robust. But that may be changing as the rest of the world plays catchup. Any domestic slowdown could be easily offset by better growth internationally.

What about inflation? How might it vary from the consensus?

With consensus that inflation will moderate in 2022, the surprise may be that it doesn’t moderate very much or at all. Everyone expects the supply chain issues to start being resolved this year and assuming less interference from the virus, that could be true. But the supply chain issues aren’t just about crimpled supply from COVID slowdowns/shutdowns.

Supply chain issues are just as much about excess demand, consumption that continues well above the pre-COVID trend. I don’t think we can assume that will change; it could well be the new normal with more spending on goods and less on services a more permanent feature of our economy, especially if the virus continues to limit in-person events.

Household and corporate balance sheets are in very good shape and consumption/investment could be funded from savings or increased borrowing, no new stimulus required. An easing of supply problems this year may well be a bad assumption.

There is also the potential for another big spending bill out of Congress. Senator Manchin has gotten a lot of attention for stopping the Build Back Better bill and rightfully so, but he hasn’t said he won’t support increased spending. He just won’t agree to the level requested by the Biden administration. There is certainly the possibility that some kind of increased spending passes Congress this year. In fact, in an election year, it seems more likely than not.

The Biden administration is going to want a “win” going into the midterms. If that happens, the budget deficit, expected to shrink again this year without a bill, may well expand. That could negatively impact inflation in two ways.

It could continue to fund a higher than normal level of consumption and it could lead to a weaker dollar.

A growing budget deficit leads to a growing current account deficit which is associated with a weaker dollar. And a weaker dollar is generally associated with higher rates of inflation.

I am not saying this is how 2022 will turn out. As I’ve said many times, I cannot predict the future and neither can anyone else.

But with the Fed and Wall Street’s track record on forecasting being what it is – lousy – it seems prudent to think about how they might be wrong. It would have been easy to lay out a scenario where growth comes up short but that is not a view that lacks promoters or fans.

After a decade of poor growth, bearish economic views are not outliers anymore. But better than expected growth in 2022 would certainly surprise a lot of people and move markets.

|

Click HERE if you want to continue reading the full note. |

EDITOR'S NOTE

Joe Calhoun is the President of Alhambra Investments, an SEC-registered Investment Advisory firm doing business since 2006. Joe developed Alhambra's unique all-weather, multiple asset class portfolios. This piece does not necessarily reflect the opinions of Hedgeye.