Financial Risk Monitor Summary (Across 3 Durations):

- Short-term (WoW): Negative / 1 of 10 improved / 2 out of 10 worsened / 7 of 10 unchanged

- Intermediate-term (MoM): Negative / 3 of 10 improved / 4 of 10 worsened / 3 of 10 unchanged

- Long-term (150 DMA): Negative / 2 of 10 improved / 3 of 10 worsened / 4 of 10 unchanged / 1 of 10 n/a

1. US Financials CDS Monitor – Swaps were mixed across domestic financials last week, widening for 15 of the 28 reference entities and tightening for the other 13.

Tightened the most vs last week: PRU, MBI, AIG

Widened the most vs last week: CB, TRV, XL

Tightened the most vs last month: SLM, PRU, AIG

Widened the most vs last month: ALL, CB, TRV

2. European Financials CDS Monitor – In Europe, banks swaps mostly widened. Swaps widened for 23 of the 39 reference entities.

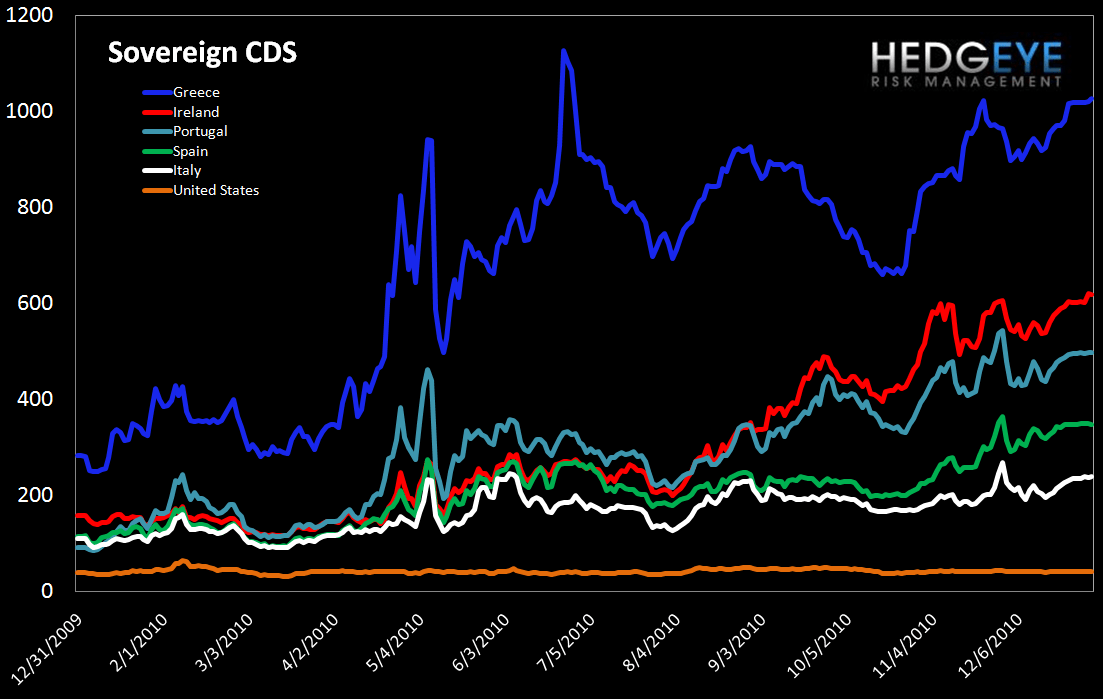

3. Sovereign CDS – Sovereign CDS rose 5 bps on average versus last week.

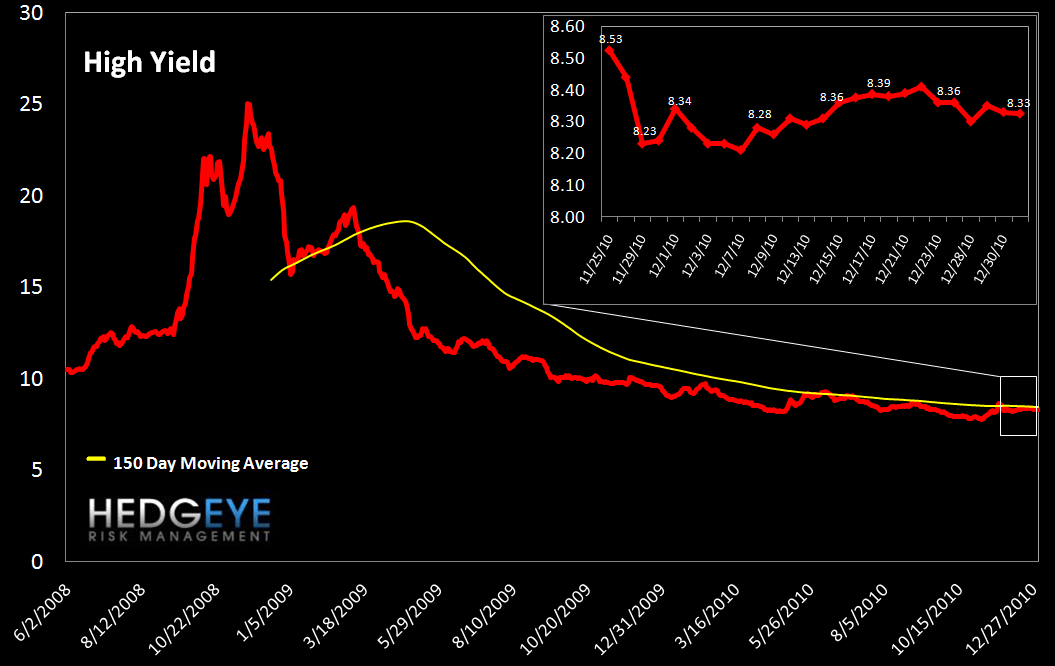

4. High Yield (YTM) Monitor – High Yield rates held nearly flat last week, closing at 8.33 on Friday.

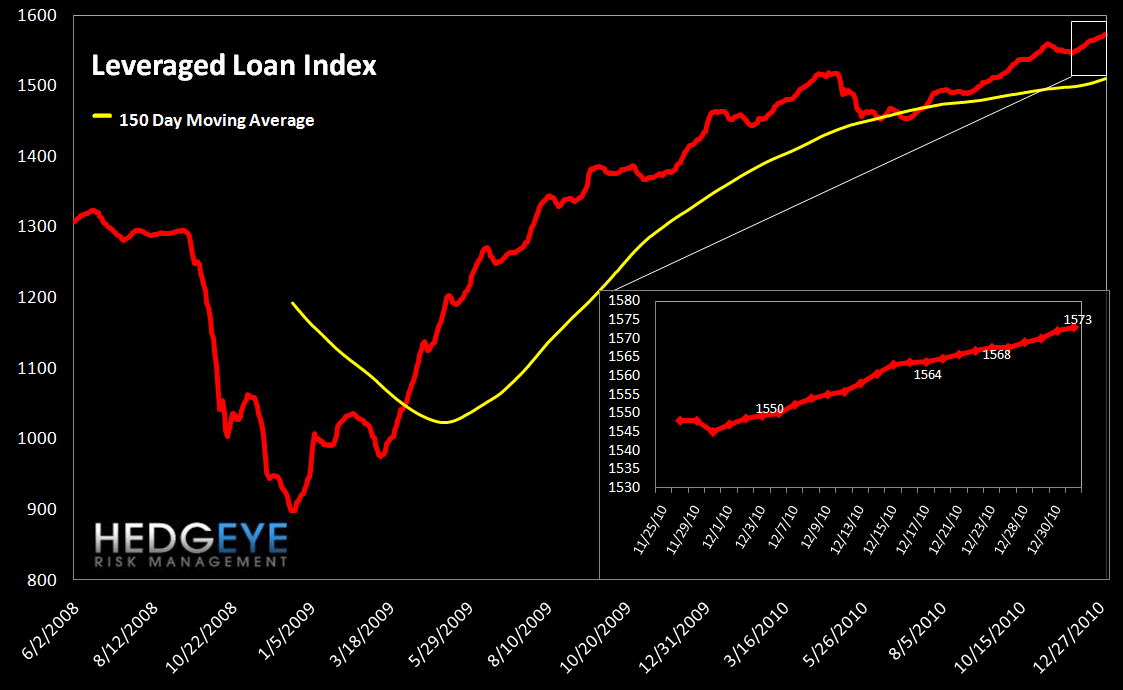

5. Leveraged Loan Index Monitor – The Leveraged Loan Index ended the year at its highs, rising 5.5 points to close at 1573.

6. TED Spread Monitor – The TED spread rose to 18.3, up from 17.1 the prior week.

7. Journal of Commerce Commodity Price Index – Last week, the index rose a point, closing at 27.3 on Thursday.

8. Greek Bond Yields Monitor – We chart the 10-year yield on Greek bonds. Last week yields rose 28 bps and ended the year at new highs.

9. Markit MCDX Index Monitor – The Markit MCDX is a measure of municipal credit default swaps. We believe this index is a useful indicator of pressure in state and local governments. Markit publishes index values daily on four 5-year tenor baskets including 50 reference entities each. Each basket includes a diversified pool of revenue and GO bonds from a broad array of states. Our index is the average of their four indices. Spreads were flat last week, closing at 209 bps, 1 bp higher than a week prior.

10. Baltic Dry Index – The Baltic Dry Index did not trade last week.

11. 2-10 Spread – We track the 2-10 spread as a proxy for bank margins. Last week the 2-10 spread tightened 1.5 bps, falling to 273 bps.

12. XLF Macro Quantitative Setup – Our Macro team sees the setup in the XLF as follows: 1.4% upside to TRADE resistance, 0.3% downside to TRADE support.

Joshua Steiner, CFA

Allison Kaptur