Initial Claims Plunge 34k Breaking the 400k Line

Reported initial claims dropped sharply by 34k to 388k in the week ended December 25th. On a four-week rolling basis, they fell 12.5k to 414k. By any measure this is a positive print and should further perpetuate the Santa Claus rally in Financials. As we've written before, we expect initial claims will continue to have a tailwind through mid-January, consistent with the last two years. In other words, in spite of the seasonal adjustment factors, claims have a tailwind that starts at the beginning of December and runs through mid January. The charts below demonstrate.

We would remind investors that based on our analysis of past cycles, the unemployment rate won't improve until we see claims move into the 375-400k range. With claims in the 388k range as of this most recent print, that would suggest we could start to make some forward progress if claims remain in this range or move lower. That said, it is worth highlighting an important caveat. This recession has been different in that it has pushed the labor force participation rate down by ~200 bps, which has had a correspondingly positive improvement on the unemployment rate. In other words, the unemployment rate isn't really 9.5%, it's 11.5%. So when we say that claims of 375-400k will start to bring down the unemployment rate, we are actually referring to the 11.5% actual rate as opposed to the 9.5% reported rate. So, while we're heading in the right direction it will likely be a very long time before the headline unemployment rate improves.

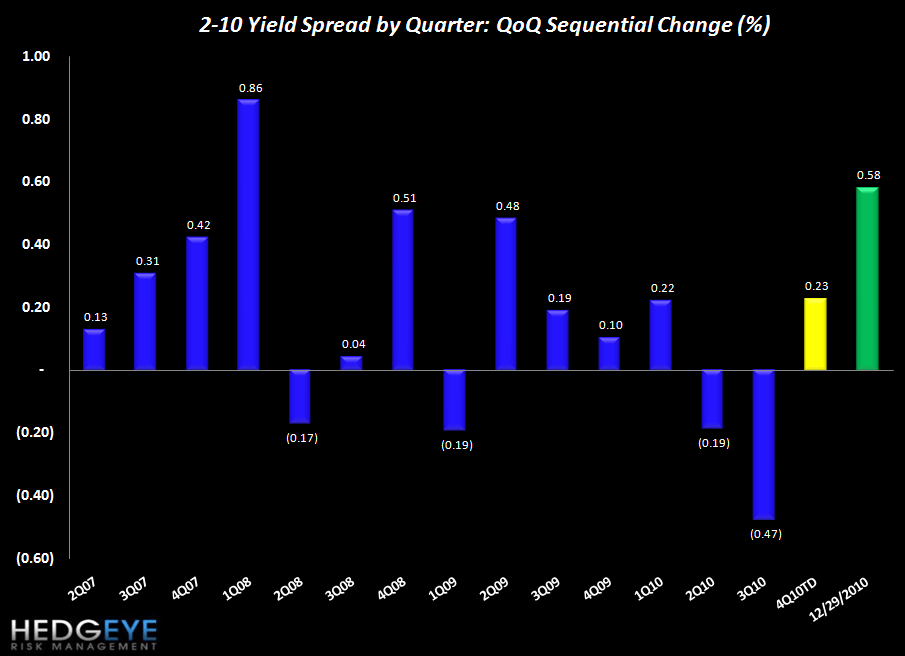

Yield Curve Widens 23 bps in 4Q10 Relative to 3Q10

We chart the 2-10 spread as a proxy for industry NIM. The spread in 4Q is tracking 23 bps wider than 3Q. The current level of 272 bps is flat with the 272 bps at the end of last week.

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over four durations.

Joshua Steiner, CFA

Allison Kaptur

{kind=link}

{kind=link}

{kind=link}

{kind=link}