The Macau Metro Monitor, December 30th, 2010

DETAILS EMERGE ON FIRING OF SANDS CHINA EXECUTIVE Las Vegas Sun

Attorneys for LVS argued that while Jacobs had sued LVS and Sands China, he had failed to name an “indispensable” party as a defendant — his actual employer Venetian Macau Ltd. For this reason, his lawsuit in the US should be dropped and any disputes should be resolved in Macau.

Some causes of Jacobs' termination are:

- Negotiated “arrangements” for Sites 5 and 6 without approval; and commissioned a brand study for those sites involving changing their names without informing the boards of Sands China and Venetian Macau.

- Negotiated a transaction with Caesars for certain development sites (site 3 and or sites 7 and 8). It’s unknown what type of deal Caesars had worked with Jacobs on.

- Disagreed in public with Adelson’s position on the growth prospects for Sands China.

- Exercised LVS stock options and sold LVS stock without first informing superiors.

TOURISM SECTOR PERFORMANCE FOR NOVEMBER 2010 STB

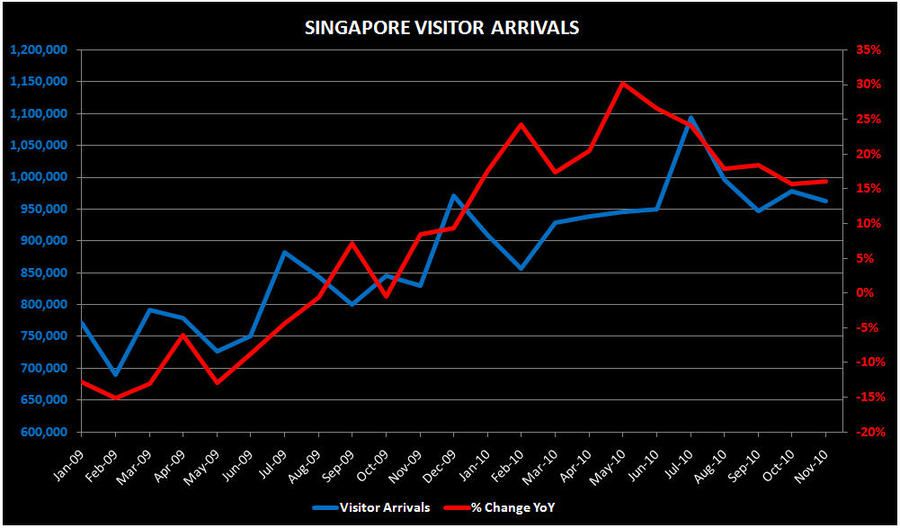

Visitor arrivals to Singapore registered 16.1% growth to reach 963,000 in November 2010. It is also the 12th consecutive month of record visitor arrivals.

Indonesia (176,000), Malaysia (100,000), P R China (94,000), India (73,000) and Australia (64,000) were Singapore's top five visitor-generating markets in November 2010. These markets accounted for 53% of total visitor arrivals for the month. India (+46.3%), Hong Kong SAR (+45.3%), and South Korea (+41.8%) registered highest growth out of the top 15 markets.

REGULATION FD DISCLOSURE Las Vegas Sands

As part of his individual long-term strategy for asset diversification, tax and family planning, acting Sands China CEO, Michael Leven, plans to sell up to 1,758,349 shares of company stock during 2011, with 133,349 stock option shares planned to be exercised and sold in January 2011, 125,000 stock option shares planned to be exercised and sold in February 2011 and 150,000 stock option shares planned to be exercised and sold in each month from March through December 2011.

LIGHT RAIL TENDER WINNER ANNOUNCED macaubusiness.com

Mitsubishi Heavy Industries has won Macau's LRT contract (1st phase) by bidding MOP4.688 BN (US$586 MM). Construction is expected to start in 2011 with the 1st phase of the system opening in 2015.