TODAY’S S&P 500 SET-UP - December 29, 2010

As we look at today’s set up for the S&P 500, the range is 16 points or -0.68% downside to 1250 and 0.60% upside to 1266. Equity futures remain above fair value as commodity stocks continue to benefit from investors hedging a declining dollar. In overnight news, China's central bank raised its rediscount rate 45 bps to 2.25%.

- Groupon has filed to raise as much as $950m in funding after spurning $6b offer from Google this month, according to VCExperts; financing would value Groupon at as much as $7.8b.

- New York and Ohio state pension funds will be lead plaintiffs in shareholder litigation against BP over Gulf of Mexico spill losses

- Leonard Green may launch hostile bid for BJ’s Wholesale if an auction isn’t initiated in coming weeks, the N.Y. Post reports

- Blackstone makes preliminary offer of unknown size for Australia’s Centro Properties, which owns 600 U.S. properties, WSJ reports

- U.S. flight delays threaten to stretch into weekend after as many as 1.2m airline customers were affected by worst Dec. snowstorm to hit New York City in six decades

- Hemispherx Biopharma (HEB) said it will restate financial statements for this year and last year

- Sara Lee (SLE) agreed to sell White King, Janola business to Symex for EU37.9m ($49.6m)

- Savient Pharmaceuticals (SVNT) said it initiated a search for a CEO; Paul Hamelin, co. president since 2008, will continue to lead the company until it hires new CEO.

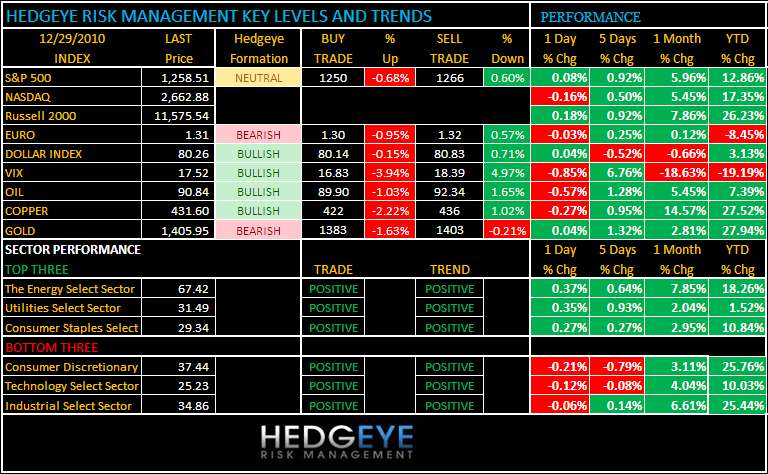

PERFORMANCE

- One day: Dow +0.18%, S&P +0.08%, Nasdaq (0.16%), Russell (0.36%)

- Last Week: Dow +0.72%, S&P +0.28%, Nasdaq +0.21%, Russell +0.34%

- Month-to-date: Dow +5.17%, S&P +6.60%, Nasdaq +6.59%, Russell +8.59%

- Quarter-to-date: Dow +7.30%, S&P +10.28%, Nasdaq +12.42%, Russell +16.76%

- Year-to-date: Dow +11.00%, S&P +12.86%, Nasdaq +17.35%, Russell +26.23%

- Sector Performance mixed (6 sectors up,3 down) - Energy +0.37%, Utilities +0.35%, Consumer Staples +0.27%, Materials +0.21%, Healthcare +0.06%, Financials +0.01%, Industrials -0.06%, Tech (0.12%) and Consumer Discretionary (0.21%)

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -125 (-445)

- VOLUME: NYSE 560.21 (+19.81%)

- VIX: 17.52 -0.85% YTD PERFORMANCE: -19.19%

- SPX PUT/CALL RATIO: 1.45 from 2.06 (-29.46%)

CREDIT/ECONOMIC MARKET LOOK:

Treasuries sold-off sharply on Tuesday, significantly more so following a disappointing $35B 5-yr auction which yielded 2.149%, or approximately 8bps above the prior trade. 10-yr notes added nearly 16bps, most of which in response to the auction, to yield 3.49%.

- TED SPREAD: 16.39 -0.101 (-0.615%)

- 3-MONTH T-BILL YIELD: 0.15% -0.02%

- YIELD CURVE: 2.65 from 2.76

COMMODITY/GROWTH EXPECTATION:

- CRB: 331.43 +0.70%

- Oil: 91.49 +0.54% - Trading down 0.69% in the AM

- Crude Falls From Near a 26-Month High on Pessimism About U.S. Stockpiles

- COPPER: 432.80 +1.12% - Trading down -0.18% in the AM

- Copper Advances to Record in London Trading on Speculation of More Growth

- GOLD: 1,405.35 +1.84% - Trading up small in the AM

- Gold Fluctuates as Concern About Europe Spurs Demand for Wealth Protector

OTHER COMMODITY NEWS:

- Rubber Advances to Near Record as Buyers Lured by Yesterday's Price Tumble

- Corn Drops on Speculation Investors Cash in Gains After Eight-Day Advance

- South Korea Raises Foot-And-Mouth Alert to Highest Level to Curb Outbreak

- Cotton Crops Washed Away by Flood Waters in Australia's Queensland State

- QR National Coal Shipments Are Curbed by Queensland Flooding, Derailment

- Smuggled-Diamond Revenue Flows to Robert Mugabe's Zimbabwe Before Vote

- Anglo Will Invest $770 Million in Brazil Iron-Ore Port With Batista's LLX

- Steel Authority India to Pay 8% More for Imported Coking Coal Next Quarter

- Dutch Cargo Ship Runs Aground in Finland, No One Injured, Broadcaster Says

CURRENCIES:

- EURO: 1.3127 -0.06% - Trading down -0.06% in the AM

- DOLLAR: 80.402 +0.04%% Trading down -0.16% in the AM

EUROPEAN MARKETS:

- European Markets: FTSE 100: -0.52%; DAX: +0.40%; CAC 40: +0.89% (as of 07:30 EST)

- European markets edged higher in light volumes with the UK lagging after its extended Christmas holiday. Fixed income markets were pressured by disappointing US auction results yesterday as well as China's increase in interest rates, including the rediscount rate today and ahead of supply from Italy.

- Oil and mining sectors lead gainers, up around +0.6% as all but one sector, technology (0.1%), trades higher.

- The region's economic and corporate news flow was very light.

- Germany Dec Preliminary CPI due at approx 08:30ET

ASIAN MARKTES:

- Asian Markets: Nikkei +0.5%; Hang Seng +1.5%; Shanghai Composite +0.7% (as of 04:57 ET)

- Most Asian markets rose today.

- Hong Kong rose +1.54% in thin trade. Car stocks recovered from early losses when China announced it will end tax incentives for small cars 1-Jan, as had been widely expected.

- Arnhold Holdings soared 24% on announcing a takeover offer, an asset disposal, and a special dividend.

- China Rare Earth Holdings soared 16% after China cut export quotas yesterday.

- China’s benchmark money-market rate advanced to the highest level in three years as lenders hoard cash before the end of the year.

- Bargain-hunting led China higher by 0.68% after five straight down days.

- Japan opened flat but ended up 0.50% on day.

- South Korea slid slightly at the start of ex-dividend day, though it ended up 0.50% thanks to gains by brokerages and retail stocks. High-dividend stocks including SK Telecom, KT Corp, and Korea Exchange Bank fell 4-5% each.

- Australia was flat (-0.04%) after a four-day break. Miners fell on the December rate hike in China, and heavy rains continued to affect them. Tower Australia Group soared 42% on accepting a $1.2B takeover offer from Dai-ichi Life Insurance.