It’s been quite a ride but can LVS squeeze another 20% from Macau?

LVS stock may be a victim of its own success next year. The valuation is hefty at around 16x 2012 EBITDA which implies investors think the Street’s estimates are too low. We are pretty much in-line with the Street for Vegas and Singapore but somewhat below for Macau. The Street 2011 Macau EBITDA estimate of $1.4 billion for LVS is a best case scenario in our opinion, and likely not enough to satisfy investors’ appetites.

Here’s why we think LVS will grow its Macau revenues by 10% rather than the 15% or so projected by the Street:

- While we are projecting 30% market growth, table supply will be up 10% for the year with the opening of Galaxy Macau.

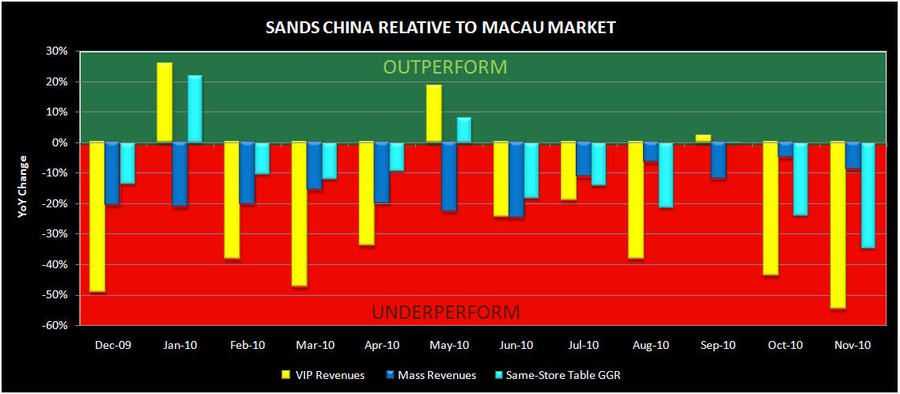

- LVS has underperformed the market (on a same store basis) by 12% in 2010. Their properties lost traction in both Mass and VIP. In October and November, the underperformance was particularly pronounced, -24% and -35%, respectively, and it may be even worse in December. Ex the supply impact, we are estimating that LVS will underperform by 10%.

- In 2010, VIP hold percentage was higher than normal at both Venetian and Sands and Mass hold was high at Venetian.

- Four Seasons faces an unrealistic comparison in Q3.

- Perhaps the largest discrepancy between the Street's projections and our own is that the Street factors in almost no cannibalization of LVS's existing properties when sites 5 & 6 open in 2012. History will tell us that when a company opens a second large property in Macau, its existing property(s) suffers the most. See our note "WYNN COTAI: A DONNER PARTY?" (11/11/10) for further details.

The following chart shows LVS’s massive underperformance relative to the market in terms of Mass, VIP, and relative to the market’s same store performance.

In terms of EBITDA, we are projecting approximately 5% cost inflation that we don’t think the Street is incorporating. Inflation is real in that part of the world, and there remains a labor shortage. Incorporating more moderate revenue growth assumptions and cost inflation, our 2011 Macau EBITDA estimate is more than $100 million below the Street and would be viewed as a disappointment.