Position: Long Germany (EWG); Short Italy (EWI), Euro (FXE)

European equity indices largely closed in the red today, with negative divergence from the PIIGS; in particular Greece’s Athex fell -2.8% and Spain’s IBEX 35 declined -2.1%.

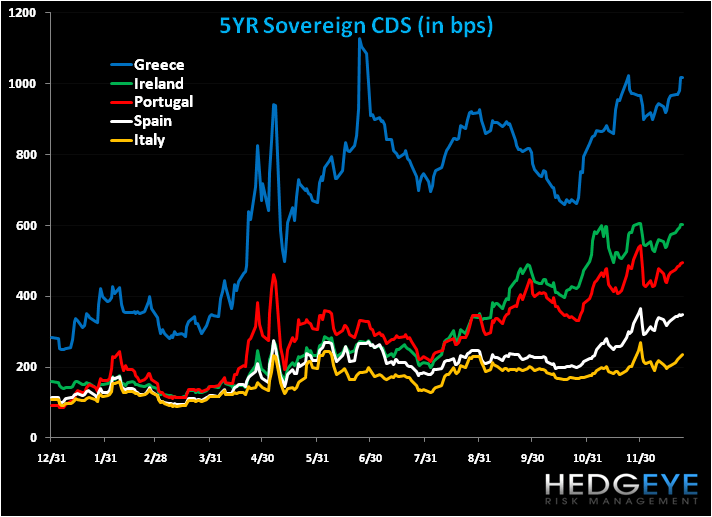

Below we refresh the charts of 10YR govt. bond yields and 5YR sovereign CDS, which show the continued heightening of risk from Europe’s periphery. Of note is Greece’s 10YR yield, which now stands at a mere 15 bps away from its previous year-to-date high of 12.449% on 5/7, a few days after Greece received a €110 Billion bailout and a few days before the EU and IMF established a €750 Billion aid package for the region to tap into.

Matthew Hedrick

Analyst