POSITION: Short SPY

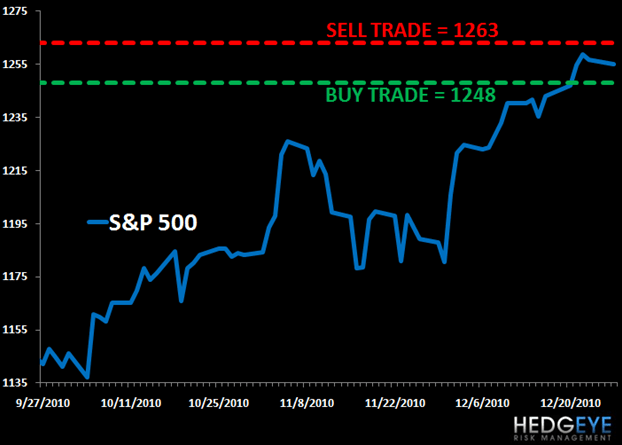

It’s hard to believe, but the SP500 is vying for its 2nd consecutive down day for the 1st time in December. That said, it’s not doing so without a fight. Despite the VIX breaking out above our immediate-term TRADE line of 16.82 today, the SP500 is holding our immediate-term TRADE line of support at 1248.

In order for the SP500 to close in the red for 3 consecutive down days, we’ll likely need to see 1248 violated on the downside. If that were to occur, I don’t see any meaningful support down to the 1218 level. Ultimately, if you’re short the US stock market here, that’s what you should be playing for in the immediate term. The bulls are as complacent as they’ve been since April, and they will not sell until they have to.

In terms of upside resistance, up at 1263 I’m still registering higher-highs versus the prior YTD closing high of 1258. That’s a bullish risk management signal and so is holding 1248, until it doesn’t.

KM

Keith R. McCullough

Chief Executive Officer