Below is a thoughtful response from a Hedgeye subscriber on Volatility in reference to a post we published yesterday titled "Interesting Chart: Complacency and Slowing Global Growth".

---

Please note that I write these comments with the fear of being overly simplistic. If it is deemed to have any value whatsoever, I am happy to discuss further.

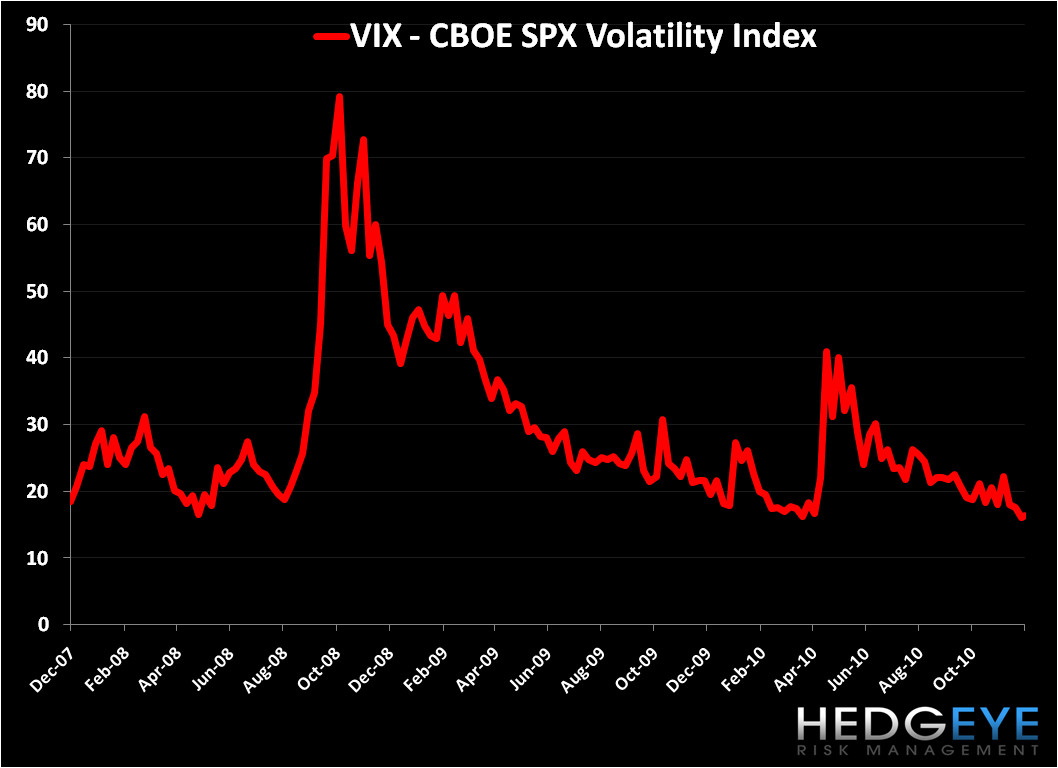

Volatility, like many instruments has seasonal factors that influence their market price. In my opinion, it is not easy to take away any meaningful information from short term volatility levels around holiday periods, especially the year end holiday season due to its length of time and social importance in many areas of the world. During this time frame, the increased risk of lower close to close variance coupled with the typically lower intraday volatility creates a much higher risk for volatility traders to hold long options positions.

With regards to the VIX in particular, it has the ability to be very misleading at times due to its short duration. It only looks at a 30 day time frame, and can be highly influenced by market holidays. In short, a typical 30 day period has 22 trading days. Many volatility traders are pricing SPX options with an adjusted number of trading days for the next month, but the VIX calculation is not. Therefore many traders value the current SPX options at higher volatility than the VIX indicates.

In short, I do think volatility is low and there is some level of complacency. However a level of 16 in April does not equate exactly to a level of 16 right now. The volatility term structure, or spread between 30 day and 90 day is still ascending and I would expect the VIX to show an increase in value after the holiday season assuming everything else equal.

-anonymous