Conclusion: Overall no great surprises but LongHorn exceeded expectations while Red Lobster once again disappointed. I will have another post out tomorrow after the earnings call.

Darden International is not cited regularly as a bell weather for consumer spending, but I think the company’s performance offers an interesting, if small, glimpse at the state of the consumer. The news out of Washington of late has led to more questions than answers. From a MACRO perspective, it will be interesting to see if this momentum will continue once the holiday season high subsides and the hangovers set in. Whether or not companies continue to invest in their concepts will likely be a huge differentiator in 1Q11 as the holiday season ends.

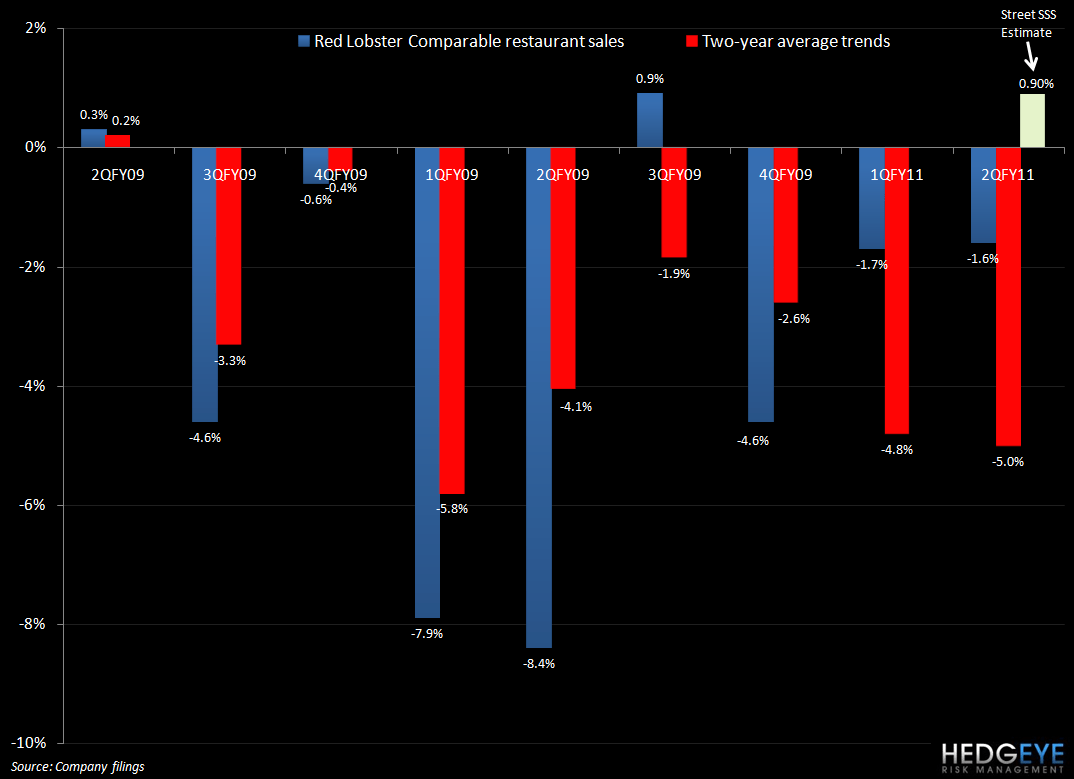

Clearly, for whatever reason, the mood of the consumer has been stronger of late and the better-positioned concepts are performing well. In Darden’s case, LongHorn is leading the way with mid-single digit traffic growth, The Olive Garden’s comparable restaurant sales are in the low-single digit range, and Red Lobster’s comparable restaurant sales figures have deteriorated on a two-year average basis for the past three consecutive quarters.

Darden has spent considerably amounts in investing in LongHorn and the results from that concept today are impressive. As you can see in the chart below, LongHorn almost beat the street consensus for comparable restaurant sales by a factor of two. The stellar performance of LongHorn will likely distract investors from the never ending turnaround that is Red Lobster. However, heading into tougher comps in 3Q11, coupled with the prospect of elevated beef prices, could put more of a deadline on Red Lobster’s ever-pending revival.

I expect management to strike a cautious tone with respect to top line trends. A sequential slowing was clearly evident in trends at LongHorn over the course of the quarter. One line-item that will need to be addressed is labor, which declined by ~120 basis points year-over-year.

Howard Penney

Managing Director