This note was originally published at 8am on December 17, 2010. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“A question that sometimes drives me hazy: am I or are the others crazy?”

-Albert Einstein

Per our friends at Wikipedia, “haze is traditionally an atmospheric phenomenon where dust, smoke, and other dry particles obscure the clarity of the sky.” That just about summarizes what I think about the US stock market right here and now.

When I say now, I mean yesterday’s closing price. The SP500 inched up another point above its YTD closing high, taking its YTD gain to +11.4%. If you’re looking at this market price through The Golden Haze of ‘everything is going to be ok’ from here, you must be saying that higher-highs in a market price are bullish. They are, until they aren’t.

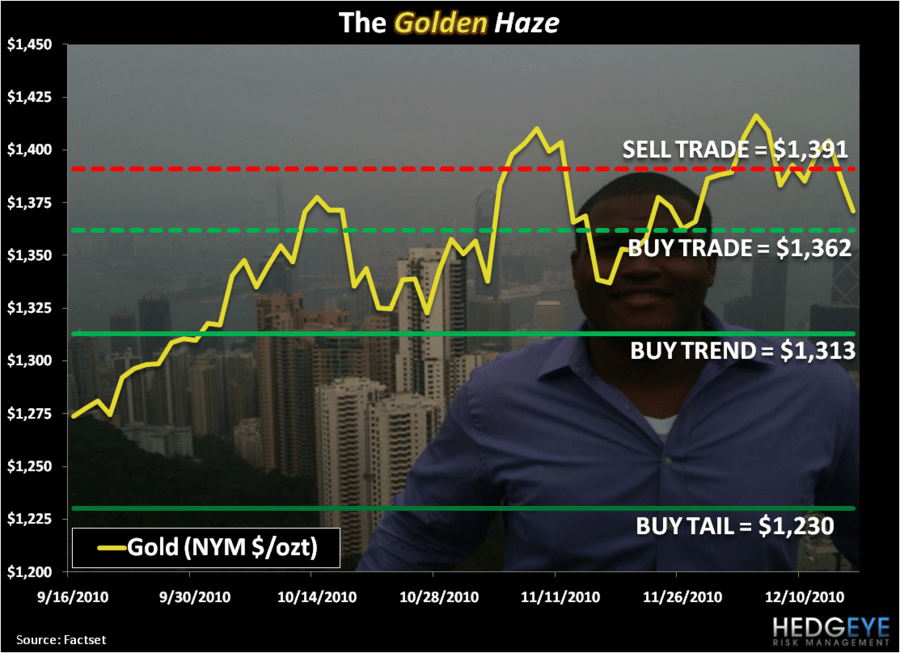

Up until 2 weeks ago, The Golden Haze was quite tranquilizing in another asset class market price – Gold. Then the music of bullish price momentum started to fade away. It didn’t stop suddenly. It didn’t stop hastily. It just started to stop…

The price of gold is now hitting a 2-week low this morning and is officially broken on my immediate-term TRADE duration. What were bullish higher-highs before December the 6th can now be considered bearish lower-highs. Again, until they aren’t.

Since I sold our entire gold position on December 6th (+3.4% higher at $138.55 GLD), I suppose I have some credibility in attempting to make another “call” on gold from here. So let’s take a shot at this and consider the why and where from here:

Why is Gold down?

- CORRELATION RISK: Over the long term, Gold tends to underperform when real interest rates are positive.

- RELATIVE STRENGTH: Real-interest rates (domestic and global bond yields) have been blasting to the upside since November.

- CURRENCY COMPETITION: Don’t look now, but the US Dollar is up in 6 of the last 7 weeks as Fed Fighting becomes fashionable.

Where does Gold go from here?

- Immediate term TRADE: as of this morning my immediate term TRADE lines of support and resistance are $1362 and $1391, respectively. Trade the range.

- Intermediate term TREND: I introduced this line to investors in Calgary and Vancouver in a slide presentation on December 5th and 6th and the TREND line hasn’t changed. There’s intermediate term mean-reversion risk in the price of gold down to $1313.

- Long-term TAIL: there is a world full of support down in the $1210-1230 range and I’d love to buy back my gold there.

Now anyone who knows me well knows that I probably won’t have the patience to wait for $1230 gold on my buyback program. Heck, I may not have the patience to wait for $1313 either. But, provided that I remain bullish on the US Dollar (long UUP) and US Treasury Yields (short SHY), I’ll have a very hard time explaining why I’d buy back gold anytime soon. Being short gold on the next rally to lower-highs may be the better bet. We’ll see.

Back to The Golden Haze that is being long US Equities here… I think it’s instructive to think through the same CORRELATION RISK, RELATIVE STRENGTH, and CURRENCY COMPETITION scenario analysis that I went through for gold.

- CORRELATION RISK: using an intermediate-term TREND duration (6 months), the SP500 has an inverse correlation to the US Dollar Index of -0.77 and an r-square of 0.60. In other words, sustained USD strength should be bearish for US equities.

- RELATIVE STRENGTH: since March of 2009, the SP500 has outperformed gold by a lot (SP500 is +83.7% from its March lows, whereas gold is up 53%). So if Gold can go down in the face of Fed Fighting (competing with higher real interest rates), US stocks can.

- CURRENCY COMPETITION: seasonal spikes in the US Dollar Index have happened in both of the last 2 years (2009 and 2010). It wasn’t cool to be levered-long US Equities in either of those January-February periods.

Never mind the obscurity of making the “valuation” case for stocks here; valuation isn’t a catalyst. Never mind the atmospheric phenomenon of short-term politicking and its effect on stoking “growth” hopes in the US economy either. That’s now consensus.

Take the “call” to sell US stocks here from a man who is already -3.37% too early in his short position (that would be me), as every Big Broker’s “strategist” is now officially calling for the US stock market to be up next year.

My immediate term support and resistance levels for the SP500 are now 1234 and 1248, respectively. If the SP500 makes another higher-high in the coming weeks, look for me to short it again. Yesterday I moved to a 70% position in Cash in the Hedgeye Asset Allocation Model.

Enjoy your weekend and best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer