This note was originally published at 8am on December 16, 2010. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Conformity is the jailer of freedom and the enemy of growth.”

-John F. Kennedy

I’ve heard a lot about “growth” in recent weeks. After a March 2009 trough to December 2010 peak rally in the SP500 of +83%, the US centric stock market bulls say “growth is back.” As a result, conforming to an institutionalized consensus weeks before our profession receives its year-end bonus check is a mounting pressure in my inbox. I’ve seen this movie before.

The Enemy of Growth isn’t going away. It’s called debt. Sovereign debt. And, no matter where you go in the new year, there will be more and more of it…

You don’t have to take my word for it on this. The longest of long-term data series we can find on sovereign debt default cycles and their correlations to fiat currency issued debts and structural inflation can be found in Reinhart & Rogoff’s “This Time Is Different.”

No, this is not a new thesis this morning. It’s a critical reminder. Because US stock market consensus is choosing to ignore it for a few more weeks doesn’t mean it ceases to exist.

The Enemy of Growth isn’t a Thunder Bay bear. It’s marked-to-market on your globally interconnected macro screens every day. While it’s convenient to assume that a +10% YTD return in the SP500 is a leading indicator for growth, one can easily argue that US style Jobless Stagflation won’t lead America to sustainable economic growth in 2011.

Remember, “inflation is a policy.” Or at least that’s what an ole school Austrian economist by the name of Ludwig von Mises said. Before your big Keynesian cheerleader of a global liquidity trap leads you to believe otherwise, don’t forget that it was von Mises who already called out Bernanke’s strategy to inflate 50 years ago when he said:

“The fact is that, in the not very long run, inflation doesn’t cure unemployment.” (Economic Policy, 4th Lecture, “Inflation”, page 53).

The Enemy of Growth is inflation. We know that, much like Jimmy Carter and then Fed Head, Arthur Burns, once tried to argue in the 1970s, some people think inflation is cool for some people. Some of those people aren’t the poor or middle-class however.

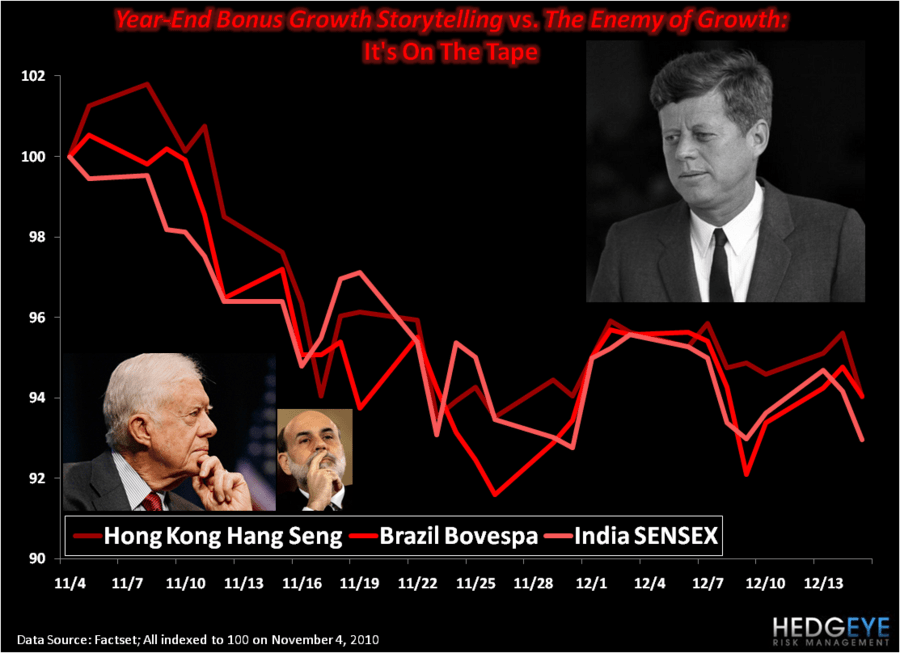

Currently, there is no more obvious threat to Global Growth Slowing than what you are seeing in emerging markets. Heck, some of these markets (like Hong Kong) might not even be considered “emerging” anymore. That’s not the point – what’s happening on the global macro scoreboard to emerging market stocks and bonds in the last 6 weeks is…

Since the beginning of November, here’s the score:

- Hong Kong’s Hang Seng Index has dropped -8.1% since November the 8th.

- India’s BSE Sensex Index has dropped -8.3% since November the 5th.

- Brazil’s Bovespa Index has dropped -7.1% since November the 4th.

Now, the first thing you’ll hear coming out of US-centric stock market bulls right now has nothing to do with:

- Spiking Sovereign Debt Yields in Spain, Italy, Portugal, Argentina, America, etc…

- US Treasury and Global Commodity markets flashing clean cut inflation signals.

- The BRIC’s (Brazil, Russia, India, and China) falling, well, like bricks.

No, no, no. It’s all about a short-term year-end bonus “pop” in US growth associated with cutting taxes so that the world worries more and more about America’s long-term sovereign debt risk. Short term political resolve perpetuating long term systemic risk. Nice trade.

Markets “pop” then “drop”… most emerging stock and bond markets are already dropping…

Like the broken European promises of reducing their deficit/GDP ratios when European bond yields started breaking out in December of last year (when Hedgeye introduced our “Sovereign Debt Dichotomy” Macro Theme), now professional US politicians are promising you this time is different. This time it’s all about “growth”…

This time, The Enemy of Growth is a government inflation policy itself.

My immediate term support and resistance levels for the SP500 are now 1232 and 1246, respectively. I continue to be a seller of bonds, reducing my asset allocation to bonds from 6% to 3% as of yesterday’s close. Inflation is bad for bonds.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer