This guest commentary was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst. This piece does not necessarily reflect the opinion of Hedgeye.

The peace of the Thanksgiving holiday was shattered when governments around the world imposed new restrictions on travel from South Africa, where a novel mutation of the COVID virus emerged.

Once optimistic views of a return to normalcy were discarded in mere moments. Securities related to the travel and hospitality industry took the requisite hit.

Source: GOOG

We all were perhaps a bit overly sanguine about the end of COVID as a global threat to personal and societal health, but the delusion was nice while it lasted. Israel has completely closed its border to travel and the US has banned travel from South Africa.

Many nations in the EU were already dealing with local flareups of COVID and will now likely head toward mandatory lockdowns this winter.

Germany is set to decide on tougher Covid-19 restrictions and could even opt for a full lockdown amid record daily infections and mounting pressure on hospitals.

Perhaps most notable is what is not changing, namely the nearly complete lockdown in China. Authorities in Beijing have made clear that they will not reopen in a similar manner to the U.S. and Europe, regardless of the economic consequences.

A study released before the holiday states that China would face a “colossal outbreak” on a scale beyond anything any other country has yet seen, if it were to reopen in a similar manner to the U.S.

“Our findings have raised a clear warning that, for the time being, we are not ready to embrace ‘open-up’ strategies,” the researchers wrote in the study, which naturally was part funded by the Bill & Melinda Gates Foundation.

They added that the approach of “certain western countries” rested “solely on the hypothesis of herd immunity induced by vaccination,” Bloomberg News reports.

Of course, the idea that vaccination imparts “herd immunity” is probably not a practical goal.

Herd immunity comes via evolution, adaptation over many thousands of years. The flu virus that killed countless millions during the Dark Ages no longer is a threat. Vulnerable populations have been rendered extinct, but the survivors have herd immunity. Yet the great marketing imperative of Western commerce has given such ideas as “herd immunity” via vaccination substance.

In communist China, on the other hand, the imperative is security and political control, thus the idea of a Western-style reopening is unthinkable. A significant increase in COVID cases could threaten communist party rule.

The fact that few Chinese are actually vaccinated and most with the less desirable Sinovac jab has forced China to employ a flexible lockdown strategy to enforce the “zero COVID” rule.

Given the political imperative of control, it could be many years before China reopens. Ponder the significance for the global economy of an extended China lockdown.

The Chinese response to COVID is instructive for a number of reasons. First and foremost, if you cannot afford to lose control of the number of illnesses, then a lockdown is essential to control COVID.

If your priority is a rapid restoration of commerce and related social interaction, on the other hand, then you reopen once you’ve reached ~ 50% vaccination and hope for the best. The comparison between the chaos of Germany and the cold determinism of China is notable.

The decision by western nations to re-open earlier this year evidenced herd behavior. In the US and other western nations, the view of the herd is the operative rule.

Official health pronouncements are often ignored or even attacked as somehow infringing on personal rights, this in a society where celebrity is credibility. Celebrity is ephemeral and a function of the crowd, however, while considered, sometimes terrible judgments that lead to glory and renown tend to be more enduring.

The Chinese response to COVID is notable because the communist party is deliberately imposing its will in place of the popular herd tendency, which naturally is for opening.

In China, the government is prepared to lock down whole cities and regions indefinitely at the first sign of contagion and enforce this cordon. Even if the policy of rolling lockdowns cuts points off GDP, the rule of zero COVID is maintained.

Time will tell which policy is more effective for society as a whole.

Meanwhile, in the world of crypto, the herd mentality seen throughout the global financial markets is in full force and then some. If you think it is dangerous to express divergent opinions on dealing with COVID inside Xi Jinping’s nation prison, then consider the situation in crypto land. Brent Donnelly of Spectra Markets writes:

“The BTC and crypto hype machine is 10X more powerful than the 1999/2000 internet hype machine. Nobody is ever going to tell you when to sell. It is borderline verboten for anyone in crypto to even utter a bearish word. Keep that in the back of your mind. Every story you ever hear is going to be bullish.”

Donnelly notes that whereas a lot of market movers such as Paul Tudor Jones were pounding the table regarding crypto and equities in 2020, the favorable conditions for such speculations are now reversing.

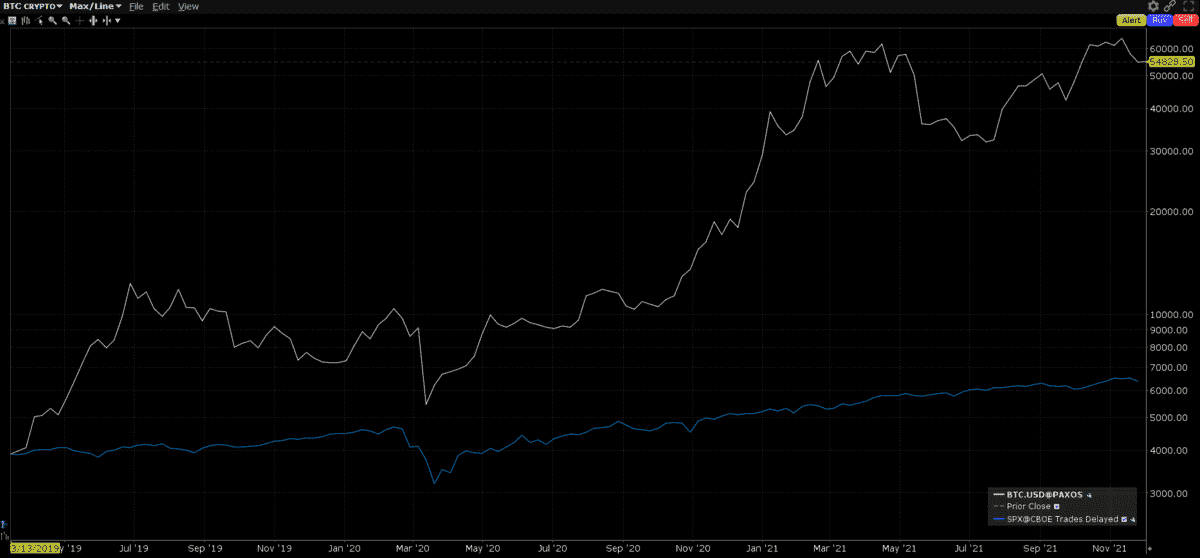

“And all those new TradFi types that have just bet their careers on crypto will not be able to ignore the turn in the Fed cycle as easily as non-macro crypto maxis,” Donnelly concludes. The chart below shows BTC vs the S&P 500.

Source: IBKR

Just as herd behavior has taken stocks and crypto tokens to new heights since the Q1 2020 correction, the thundering herd is prepared to ride these same markets back down in a Fed tightening phase.

Sure, global demand for dollars will increase as the next COVID wave runs through Western market economies, making it difficult or impossible for the FOMC to actually raise the cost of credit. But the narrative of a slowing economy and another COVID pandemic shock will be a tough reality for the perma-bull crowd to ignore, both in stocks and crypto.

It may not be possible to discuss the fundamentals of bitcoin and other crypto assets with any precision, but it is possible to observe the deteriorating fundamentals of US banks and other financials. The culprit is a flattening yield curve. The Fed will taper MBS purchases as planned, hopefully faster. The prepays will be reinvested in Treasury coupons, not T-bills, further flattening the Treasury curve. The chart below shows the Treasury yield curve vs dollar swaps as of Friday's close.

Source: Bloomberg

Most of the pain felt by credit market participants in October was due to curve flattening. In September, by comparison, the shift in the curve was most significant.

Curve flattening will be the challenge going forward, but 10s-30s could actually fall in yield depending on market conditions and the direction of the herd due to the latest COVID scare. It is notable, as this edition of The IRA goes to press, that oil and other commodities are already rebounding from last week’s selloff.

Look for the Fed to keep the overall size of the system open market account (SOMA) portfolio ~ $7 trillion, meaning that they will buy only to offset net prepayments.

Until the purchases of MBS end, now targeted for June, Fed MBS purchases may grow relative to supply as new issuance slows dramatically. Total GNMA outstanding in particular is basically flat for the year and will start to decline with lower refinance volumes.

The Fed will not talk about raising target interest rates for some months, in part because they hope that ending MBS purchases will cool the housing market. The Board staff also continues to believe that inflation in other sectors is transitory. The hope prior to Thanksgiving was that a combination of ending QE and improvement in supply chains will eventually push inflation stats lower. The renewed focus on COVID will alter that calculus as winter deepens.

The problem, of course, is that once you change psychology with respect to inflation and/or pandemics, it is hard to change it back and especially when COVID fears are contributing to scarcity. Vendors will resist giving back price increases after years of absorbing hidden inflation, especially when COVID provides a convenient excuse.

A renewed lockdown in the US could present the Fed and markets with a lethal combination of rising inflation and an economic recession. And meanwhile, China remains in lockdown.

ABOUT CHRISTOPHER WHALEN

Christopher Whalen is the author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington. Currently, he serves as the editor of The Institutional Risk Analyst.