Looking at the table, below, it is clear to see that the restaurants’ rip in equity prices is slowing into year end. Some notable items:

- QSR volume was light yesterday with all stocks besides PEET and KKD generally flat or down

- An article on Nation’s Restaurant Review titled “NPD forecasts modest recovery” highlights unemployment among the young adult age cohort as being a particular concern for QSR

- Additionally, short interest in the QSR space is particularly low, 6.6% on average. If we exclude the coffee concepts, it stands at 4.3%. Over the course of 2010, these stocks have risen an average of 44%

- CMG has also slowed and was downgraded last week

- MCD is planning massive expansion in China – boosting investment by 40% in 2011, according to media reports. This is certainly relevant for YUM

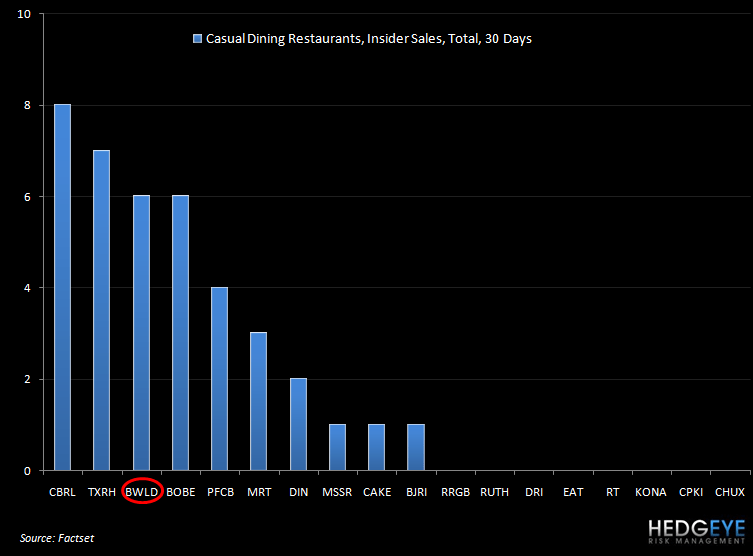

- In casual dining, following a downgrade, BWLD declined on volume slightly up versus trailing 30-day average volume. It is also interesting to see insider selling having picked up in BWLD over the past 60 days (with roughly equal proportion of selling over the period)

- CAKE underperformed the space on high volume following a downgrade

Howard Penney

Managing Director