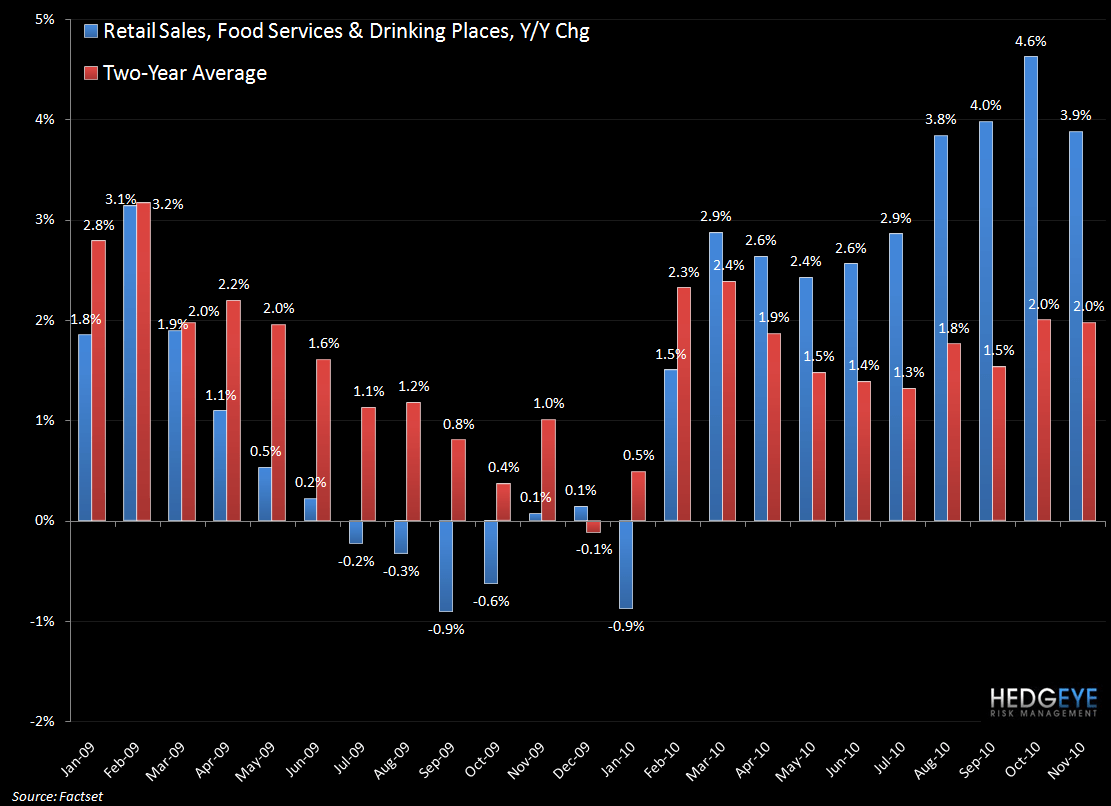

Conclusion: Retail sales came in strong today. However, it is important to note that, on an absolute basis, the number is below where it was three years ago. Sales growth for the Food Services & Drinking Places sector is more anemic than it is for total Retail Sales.

On the back of the strong retail sales numbers, I want to continue with my theme from Monday's Early Look titled, “The Pursuit of True Wisdom.”

As it related to the consumer spending it’s an appropriate time to reflect upon (1) What has transpired? (2) Where are we headed? and (3) What is left undone?

First some details. Retail sales jumped 0.8% in November in total, on top of an upwardly revised 1.7% gain in October. Clearly, the consumers have clearly picked up the pace of their spending (on the heels of increased optimism as the market heads higher); sales less autos growth was even steeper in November at 1.2%, up from 0.4% last month. Is the potential for pent-up demand real?

Sales in November were strong (up for the 4th consecutive month) in nearly all categories outside of housing-related segments. Top-line sales growth have risen at least 0.8% in each of the last four months and averaged 1%.

Growth in November was led by gas stations (+4%), department stores, apparel stores (+2.7%), sporting goods and hobby stores (+2.3%), and nonstore retailers (+2.1%). On the declining side Motor Vehicle& Parts (-0.8%), furniture stores (-0.5%), electronics and appliance stores (-0.6%), and building supply (-0.01%). Restaurants were another noteworthy laggard, up only 0.1%.

What has transpired?

- Income is improving

- The consumer has deleveraged but will continue to do so at a slower pace

- Debt payments have declined dramatically

- Stock market gains are also lifting the spending of higher-income households

- Pent-up demand is being released

Where are we headed?

- Year-over-year growth is likely to slow because comparisons get much more difficult.

- House prices are falling again, contributing to consumers' continuing need to rebuild their balance sheets

- Rental income is up, likely as a function of the soft housing market

- Consumers are doing little borrowing

- In this environment, spending will continue but it is unlikely recent growth is sustainable

What is left undone?

- Additional support will come next year in the form of reduced taxes and increased unemployment insurance benefits if the tax compromise passes

- Unemployment is high, and job gains have not been consistent enough or sufficient to put any downward pressure on the unemployment rate

The strong November growth, combined with upward revisions to the prior two months, shows sales growing at a 13% annualized pace over the last four months. However, some perspective is in order. Even following this period of outsize growth, sales remain slightly below the November 2007 peak. In essence, sales are at the same level they were three years ago.

The first chart below shows Retail Sales for the Food Service and Drinking Places sector. While the sector performed with relative resilience during the recession, it will be interesting to see whether this level can be maintained when comps become materially more difficult in February.

The second chart illustrates total Retail Sales. While November 2009 was the first month of year-over-year sales growth following the recession, growth was only 1.8%; it grew to 5.5% in December and topped 8.5% and 8.7% in March and April, respectively.

Howard Penney

Managing Director