Round-up of today’s data: Berlusconi wins Confidence Vote; Bullish German ZEW survey; UK CPI accelerates; Spain’s Pain continues; Portugal bows to the client (China)

Position: Long Germany (EWG); Short Euro (FXE), Short Italy (EWI), Short Spain (EWP)

Viva Berlusconi!?

Italian Prime Minister Silvio Berlusconi won a no-confidence vote today, capturing the upper house easily, but winning by a slim majority of 314 votes to 311 in the lower house. As we noted in our post yesterday titled “Silvio’s Black Eye”, despite the victory, Berlusconi’s slim majority should only prolong Italy’s Crisis in Confidence and increase the risk that Italy struggles to finance and meet its debt obligations next year.

Position: Short Italy via the etf EWI. Current public debt projections mark Italy’s debt at ~120% of GDP. Next year, Italy is rolling up against a substantial €350 Billion in government debt maturities (principal + interest) and we’re of the opinion that the market will increasingly punish its fiscal imbalances alongside continued political uncertainty with Berlusconi at the helm. YTD we’ve seen a steady rise in the country’s risk premium via credit spreads and yields, and a more parabolic move alongside Ireland’s funding assistance over recent weeks.

Bullish German Sentiment

The German ZEW economic sentiment survey showed confirmation of a positive outlook for the next 6 months in Germany, rising to 4.3 in December from 1.8 in November, with improvement over the last two months. The current situation index also gained, registering 82.6 in December versus 81.5 in the previous month.

Position: Long Germany via EWG. We continue to like Germany’s fundamentals that present a strong dichotomy from most of its European peers. Germany’s strong exporting and industrial complex continues to get orders, especially from China. Unemployment has trended lower this year, currently at 7.5%, and the DAX has powered forward at 17.8% YTD.

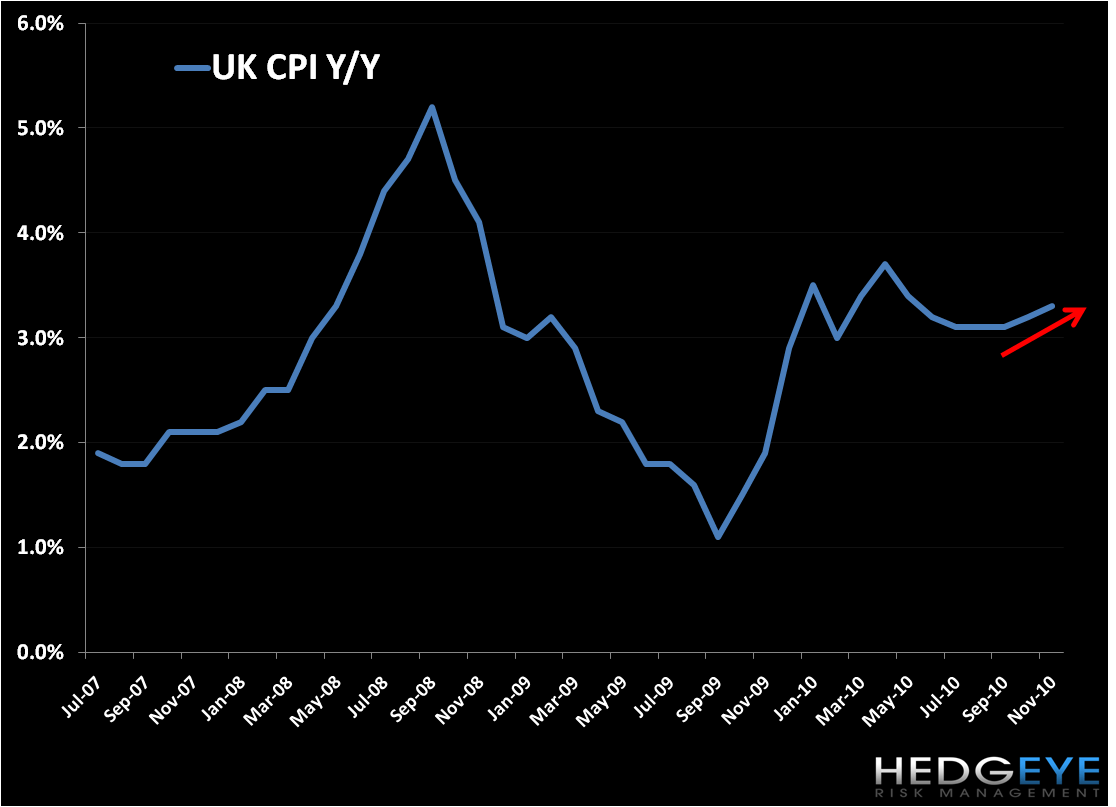

UK’s Inflationary Dilemma

UK headline CPI registered 3.3% in November versus the previous year, an acceleration from October’s rate of 3.2%. With inflationary signals from November PPI (input and output) published in the last days, it came as no great surprise that headline CPI also rose. We think the UK’s inflationary issues are well documented; however the BOE still seems quite divided to make any policy changes. The dilemma remains that an additional bond purchasing program would encourage inflation, while increasing the main interest rate could threaten growth. The Bank’s consensus may well remain to do nothing for the next months.

Spain’s Pain

Today we saw a similar trend in Spain’s bond auctions, namely the increased yield premium to entice investors, a trend also seen across auctions from Europe’s fiscally weaker countries. Spain issued nearly €2 Billion of 12M bonds at 3.449% versus 2.363% on November 16th. €523 Million of 18M bonds were also sold at 3.721% versus 2.664% in November. We’ll have our eyes on Spain’s auction this Thursday with maturities in 2020 and 2025 to be issued.

Portugal at China’s Hand

Portuguese Finance Minister Fernando Teixeira dos Santos completed a two-day visit to Beijing to meet with Chinese Finance Minister Xie Xuren, Chinese central bank Governor Zhou Xiaochuan, and officials of China’s state administration of external reserves to strengthen relations as Portugal hopes to get additional financial support from China.

Teixeira dos Santos said, “We took a big leap forward in terms of strengthening our relations at all levels, commercial and investment, and also in the area of financing,” however did not specify the amount of Portuguese treasury securities that Chinese institutions have already bought or will buy.

Take-away: Going to the Client (China) is an interesting move as Portugal attempts to get the media’s spotlight off its sovereign debt issues. Notwithstanding, we do not believe Portugal can escape the market forces that punish countries with excessive debt leverage and political instability.

Matthew Hedrick

Analyst