This guest commentary was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst. This piece does not necessarily reflect the opinion of Hedgeye.

“Anyone taken as an individual is tolerably sensible and reasonable – as a member of a crowd he at once becomes a blockhead.”

- Friedrich von Schiller, as quoted by Bernard Baruch

“A Short History of Financial Euphoria”

John Kenneth Galbraith (1993)

Back in May of this year, we published a comment that described the three key components that the Federal Reserve Board was seeking to put in place prior to a change in monetary policy and specifically an end to quantitative easing or “QE” (“Fed Prepares to Go Direct with Liquidity”).

To review, those components are:

-

Liquidity: First, the FOMC is going to make permanent the RRPs, essentially accepting the proposal by the Federal Reserve Bank of St Louis to create a standing repo facility for banks and nonbanks alike. This means that funds, REITs and especially smaller dealers are going to be able to go direct to the Fed of New York and finance collateral, breaking the monopoly control of the big primary dealer banks.

-

Money Market Funds: Second, and this change is already in process, “swing pricing” for money market funds and corporate bond funds will allow the Fed and the Financial Stability Oversight Council (FSOC) to manage market liquidity. For investors, this means that the Fed and FSOC will be able to suspend immediate cash redemptions on money market and corporate bond funds in time of liquidity stress. The message here is simple: “We’ll get back to you.”

-

Centralized Clearing: Third and most significantly for the large banks, the Fed and FSOC are going to push for central clearing of all Treasury securities, killing the predominantly bilateral market for US debt and also eviscerating the monopoly of the primary dealers on financing collateral. As our friend Ralph Delguidice reminded us at the time, centralized clearing of Treasury collateral closes the door to those big, 100:1 leverage offshore trades in risk-free collateral that the big banks love.

The trouble, of course, is that only a few of these three necessary conditions for monetary tightening are actually in place. The Fed has stood up a facility for reverse repurchase agreements (RRPs) that is open to a variety of financial institutions.

Indeed, the rate hike on reserves this past July by the Fed’s Board of Governors was a direct sop for banks and money market funds that were close to collapsing under the weight of zero rates and QE.

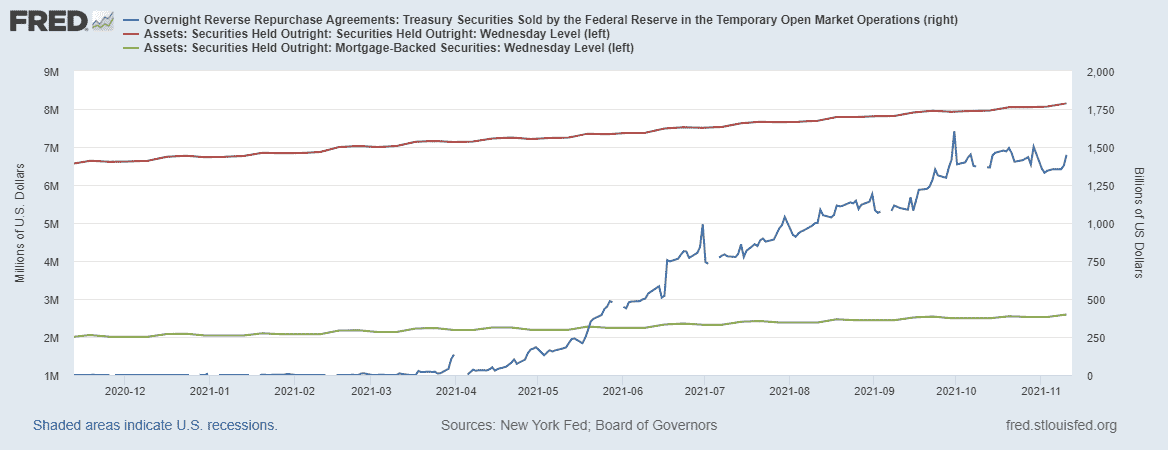

The chart below shows the total assets of the Federal Reserve System as well as holdings of mortgage-backed securities (MBS) as part of the total on the left axis. On the right access, we see the $1.5 trillion in RRPs.

Fed officials have stated publicly that the use of RRPs to sop up cash injected by QE is a “transitory” phenomenon, but we suspect that the need to subsidize MM funds and banks is going to only grow as the Treasury yield curve flattens.

When the FOMC is forced to end purchases of MBS and instead routes prepayments into longer-term Treasury collateral, the mother of all curve flatteners is just around the corner.

As the shift in Fed purchases via QE starts to accelerate, the total amount of liquidity in the system will decline – thus the need for a standing forward repurchase facility for securities. We have argued on Twitter that the FOMC should be targeting duration rather than interest rates.

Think of duration as the average time it takes to get half of your money back from an investment.

The impact of forcing interest rates down is to lengthen the duration of fixed-income assets. If the coupon on a bond is low or even negative, then the duration of the security -- i.e, when you receive a return on investment -- extends.

But what happens when the fact of low interest rates incentivizes issuers to repay securities earlier, even with a prepayment penalty, and refinance these liabilities with new debt or even equity? Then duration suddenly shortens and investors are forced to deploy funds into other assets. This has been the impact of QE on MBS and all callable securities.

As the FOMC throttles back on QE, the central bank is essentially leaving more duration in the markets for investors. Think of duration as the opportunity to earn a return.

As QE recedes into memory, investors will have more opportunity to earn returns away from stocks, necessarily affecting the supply-demand balance in the markets. And duration, of course, is another way of measuring financial repression by global central banks.

There are many factors, plus and minus, that impact this balance, but history suggests that a cessation of QE is bad for stocks. The table below from FRED shows the S&P 500 on the right axis and the total assets of the Federal Reserve System on the left axis.

Again, there are many factors that will impact the balance between stocks and bonds, but the simple fact is that when the FOMC stops creating hundreds of billions of dollars in liquidity each month, and buying securities for the System Open Market Account (SOMA), then the proverbial risk curve will shift back toward its positions pre-QE.

Early stage companies will find it harder to raise new capital and investors may even start to demand higher returns for risk taken. Just imagine that. And in the meantime, we view the end of QE as a net negative for global stocks as well as crypto. Everything is correlated in a crowd.

But as new mortgage lending dives below 5 million loans in 2022 vs 10 million in 2020, mortgage spreads may not widen for months or even years. On the other hand, inferior companies locked out of the equity markets may be forced to raise debt, which could be good for spread widening.

Yet the long-term impact of QE may be to distort the markets for years to come, both up and down, as the geniuses on the FOMC try to fine tune the widening disaster of market manipulation that we politely refer to as monetary policy.

ABOUT CHRISTOPHER WHALEN

Christopher Whalen is the author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington. Currently, he serves as the editor of The Institutional Risk Analyst.