Strong revenue growth continues thru Dec 12th

Through the first 12 days of December, Macau table revenues were HK$6.629 billion. After taking into account the number of weekend and weekdays and a full month of slots, our previous HK$17.5 billion estimate for December gaming revenues remains intact. If our projection holds, December would represent another very strong month in Macau, up approximately 60% from last year.

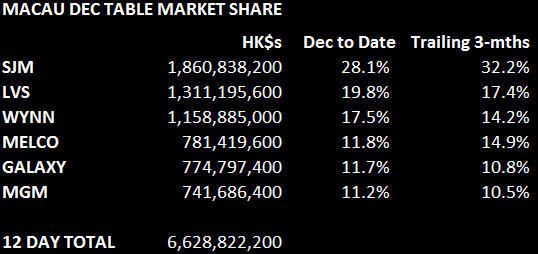

Market shares month-to-date are shown below although they are probably of little value this early in the month. Hold related volatility is obviously a bigger factor over shorter time periods. However, we remain impressed with Wynn’s market share rebound over the last few months. The addition of two new VIP rooms should continue that trend. MGM also remains above the recent trend and we expect that to continue, even beyond the Q1 IPO.