This note was originally published at 8am this morning, December 10, 2010. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“One of the privileges of a rich man is that he can afford to be foolish much longer than a poor man.”

-Ludwig von Mises

This morning’s top global macro headline is ‘China raising rates on reserve requirements in order to fight inflation.’ This shouldn’t be new “news” to anyone who follows Chinese monetary policy closely. China is willing to give-up short-term stock market performance (the Shanghai Composite Index is down -13.3% for the YTD) for long-term price stability. Fancy that.

What is inflation? It’s when prices are breaking out to higher-highs over the intermediate-term TREND. In Ludwig von Mises 4th Lecture (“Inflation”, page 52 of Economic Policy) he reminds us that “the most important thing to remember is that inflation is not an act of God; inflation is not a catastrophe of the elements or a disease that comes like the plague. Inflation is a policy.”

The Ben Ber-nank’s inflation policy has been crystal clear. Since his decision to engage in Quantitative Guessing part deux at the Groupthink Inc. meetings in Jackson Hole in August, here are the 3-month percentage moves of real-time market prices:

- Crude Oil = +18.2%

- Natural Gas = +20.8%

- Heating Oil = +18.2%

- Gold = +10.1%

- Silver = +41.2%

- Palladium = +38.3%

- Copper = +17.3%

- Cocoa = +12.3%

- Cotton = +52.4%

- Lumber = +19.8%

- Orange Juice = +16.5%

- Sugar = +35.5%

- Corn = +24.2%

- Oats = +27.9%

- Rice = +20.5%

- Soybeans = +23.6%

- Wheat = +10.3%

Now to be fair to the Fear-mongering Deflationistas who want me to believe that I should accept a ZERO percent rate of return in my savings account in perpetuity, the price of pork bellies was down -1% over the same time period. Maybe, in the short run, I should have stuffed my kids with rice-less, wrap-less, pork burritos for the last 3 months and have told them to like it… no guac.

Altogether, in the long run, the Keynesians like to say don’t sweat this short run stuff, because “you’re dead.” While that’s seemingly a convenient and clever answer to starving the world’s poor for a nice year-end US stock market “pop”, as von Mises said, “the fact is that, in the not very long run, inflation does not cure unemployment” either.

As the US stock market continues to hit higher-highs on light volume and negative breadth and skew, both global and local bond yields continue to ring the alarm bells of inflation concerns. That’s why the world’s largest bond fund, Bill Gross’ PIMCO Total Return Fund ($250 BILLION in assets under management), has lost 3% of its nominal value in the last 30 days. Inflation is a policy. Inflation is bad for bonds.

Every aspect of what’s going on in global macro markets right now makes sense to us other than US stocks going higher. No, that doesn’t mean that every stock market should be going lower. We have a 9% long position in the German stock market and that makes sense to us as countries like Germany and Australia have pseudo-sober monetary and fiscal policy that’s not equating to US style Jobless Stagflation.

As a reminder, our intermediate-term global macro outlook for the next 3-6 months is as follows:

- Global Growth Slowing

- Global Inflation Accelerating

- Interconnected Risk Compounding

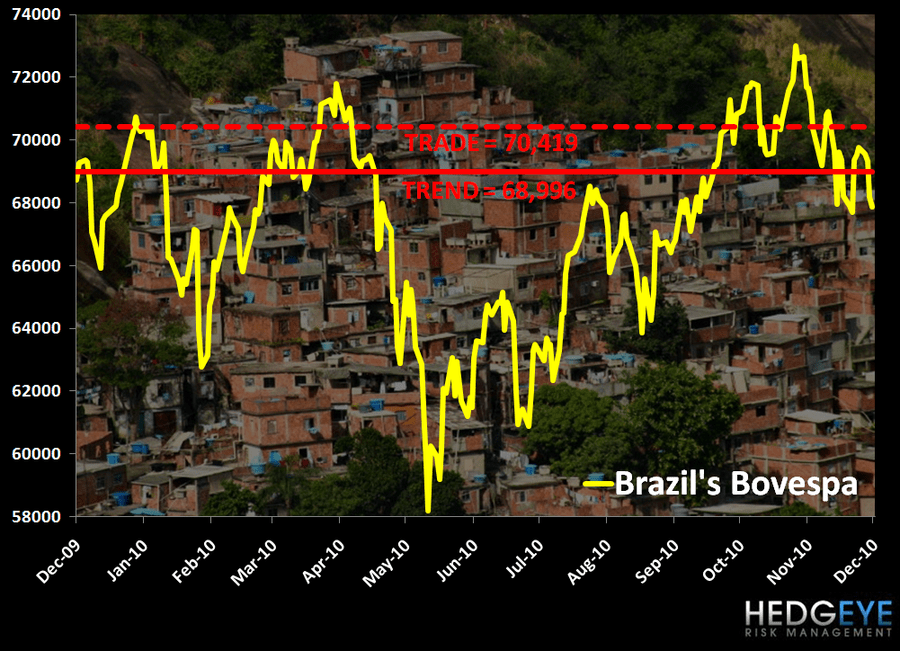

As hyped up as a US stock market bull wants to get on buying the things that China, India, and Brazil want, is as disinterested as local stock market investors in all 3 of those markets have suddenly become. Two of the three are broken on both our TRADE and TREND durations (India and Brazil) and one of the three (China) is gearing up to release very hawkish inflation data this weekend.

In the Hedgeye Chart of The Day (attached) we have outlined this point with a picture of Brazil’s Bovespa. The situation developing in Brazil’s economy is a major global macro risk:

- Growth Slowing – Q3 GDP released yesterday showed Brazilian growth slow materially (on a sequential basis) to +6.7% year-over-year versus the +9.2% reported growth of Q2 2010.

- Inflation Accelerating – this morning, Brazil’s CPI (Consumer Price Index) jumped to +5.6% for the month of November versus +5.2% reported for October.

- Interconnected Risk Compounding – as emerging market debt in Brazil comes off one of its worst monthly performances since the late 90’s , Brazil’s stock market has all of a sudden dropped -7% since the beginning of November.

Remember, market prices don’t lie; politicians do. And think about what Ludwig von Mises said in his 4th Lecture, “Inflation” (in Argentina 1959) when he asked us to “remember that, in the long run, we may all be dead and certainly will be dead. But we should arrange our earthly affairs for the short run in which we have to live.”

My immediate term TRADE support and resistance levels for the SP500 are now 1214 and 1249, respectively.

Best of luck out there today and enjoy your weekend,

KM

Keith R. McCullough

Chief Executive Officer