YUM continues to pursue an aggressive growth strategy. Here is a recap of their analyst day that occurred this week in New York.

Chief Executive Officer, David Novak, and his team gave a detailed presentation today in midtown NYC and their overall strategy remains unchanged. As they presented it, their four-pronged strategy is:

1) Build leading brands in China in every single category

Hedgeye take: An incredibly strong business and much of the future sentiment around the stock will be anchored on the performance of the China division.

2) Drive aggressive, international expansion and build strong brands everywhere

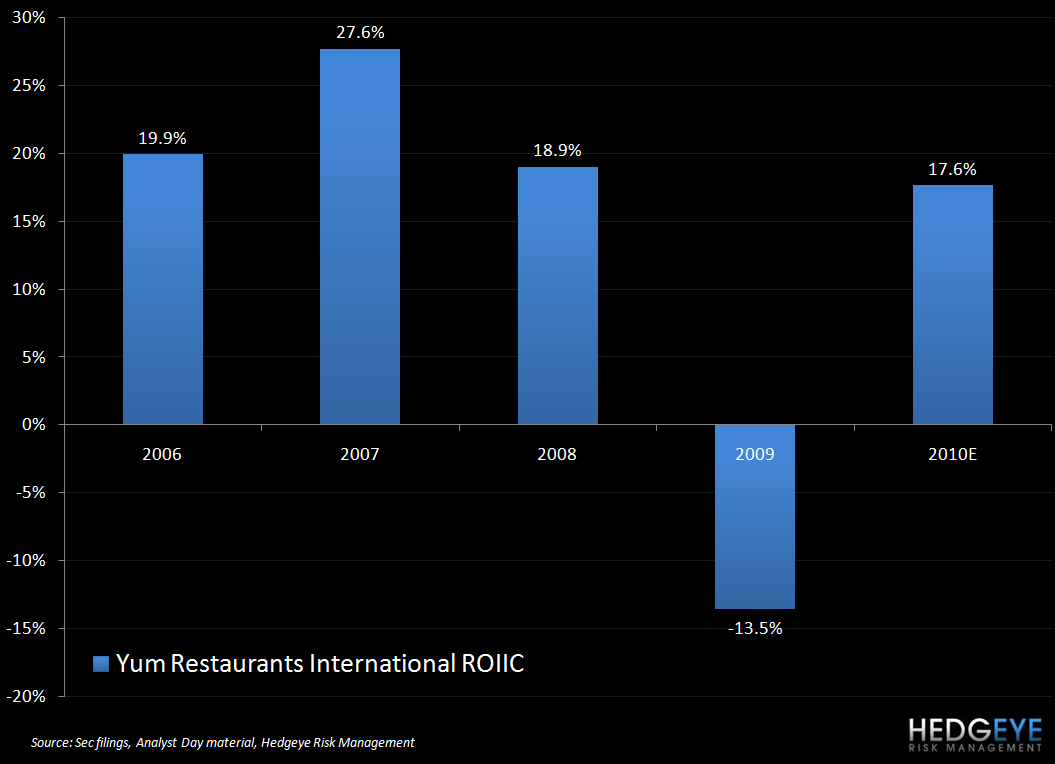

Hedgeye take: Herein is lies a risk for the company’s “aggressive growth” strategy. Incremental international “growth” related capital is moving toward the lower return western part of Europe

3) Dramatically improve U.S. brand positions, consistency, and returns

Hedgeye take: Apart from the Taco Bell and the franchise revenue stream, the US business is not competitive and is in a continued, long-term, secular decline

4) Drive industry leading long-term shareholder and franchisee value

Hedgeye take: This significant growth profile will limit the amount of cash returned to shareholders relative to the past 5 years.

I have some thoughts to share on the respective segments, as they were discussed today, and then I will conclude with some thoughts on the company’s guidance and overall strategy heading into 2011.

China

China’s performance remains impressive and management is as bullish as ever on prospects for that market. YUM plans to further improve asset utilization in the near future with breakfast being rolled out in all stores, delivery being implemented and also 24-hour service on a limited basis (just over 1,000 stores). KFC is opening in cities where no competitors exist and are currently in 650 cities in China. Management was repeatedly citing a Euromonitor source outlining the projected 650m Chinese that will make up the Consuming Class in 2020 versus the 2010 total of 450m.

Overall, the division is focused on its aim to continue growing aggressively in China. The company is appropriately focused on cities and transport hubs. It was interesting to see that the company breaks cities into six tiers. While I was unable to find a specific definition for these tiers, it follows that Shanghai and other large, developed cities are Tier 1 cities and smaller cities such as Xinghua in the Jiangsu Province are Tier 5 cities. In 2010, 15% of total builds were Tier 1, 33% were Tier 2, and 52% were Tier 3-6. It is interesting to note that operating margins have stayed relatively flat versus nine years ago despite growth being more focused on lower tier (higher margin) cities in recent years. This obviously implies that margins have declined for YUM in Tier 1 markets. There is a 500-800bps difference between T1 cities and the balance of the country. This was explained to us as being mainly attributable to higher rent expense in T1 cities. Given that operating margins are so much higher in other cities the contraction is not overly problematic, but the trends are important to watch.

China accounts for 37% of the company’s operating profit and I think it is now unwise to be negative on YUM unless one is also negative on China. YUM’s management team is “all in” as it relates to China and this is evident in their guidance for 2011. The “ongoing” growth target remains 15% on an annual basis and embedded in that number are assumptions of double-digit percent unit growth, at least 4% of comparable restaurant sales growth, and moderate G&A leverage. The 4% same-store sales imply a significant step up in two-year trends and I believe it may be slightly aggressive but top line trends remain robust.

Their earnings guidance also takes into account expected inflation levels of 5% on the Food & Paper line coming from 6-to-7% inflation in chicken (45% of mix) and 2% inflation for packaging. Management’s projection of 12% inflation in labor due to ongoing government requirements is a double-edged sword for Yum since consumers have more money but labor costs go up for their China division. Obviously one edge of that sword is sharper than the other and this will negatively impact earnings. Management seemed confident that sales leverage and the scale that exists in China would enable them to overcome these headwinds in 2011.

United States

The United States is a relatively difficult market for YUM and the company is investing less and less (as a percentage of total) in the division as a result, preferring to increase their focus on China and emerging markets. In 1998, 78% of YUM’s operating profit came from U.S. operations. At present that figure is 35% and the company projects that it will shrink further, to 25%, by 2015.

For now, though, the U.S. remains an important market and the company is struggling to stimulate the KFC business and readily admits that no silver bullet is forthcoming. Taco Bell drives 60% of U.S. operating income. For 2010, 376 (over 2x the 2009 number) remodels will be carried out and management are stepping up the pace of new unit growth for the concept. The “Bold Goal” is to build 8,000 Taco Bells in the U.S. The slide management presented to illustrate this point showed the number of Burger King restaurants in the U.S. as a comparison, which is roughly 7,300. This is not an especially useful comparison given the intrinsically different natures of the two concepts and the fact that Burger King, many could argue, could stand needs to close many of its stores.

In terms of guidance for 2011, the company is forecasting 6% operating profit for Taco Bell U.S. in 2011 and 3% for “Rest of U.S.”, which, if you take Taco Bell as 60% of operating income, implies overall profit growth of 4.8% for the entire U.S. Division. Taco Bell’s guidance assumes “modest” unit growth, 3% comparable restaurant sales growth, and “modest” G&A leverage for the year. Specific guidance for KFC and Pizza Hut within the U.S. Division were conspicuous by their absence. The lack of disclosure doesn’t bode well for their respective performances in 2011.

Overall, I expect the U.S. business to continue to be a drag for YUM. Despite best efforts, KFC is struggling and I do not believe any of the initiatives mentioned at the Analyst Day, such as increasing sandwich mix, will yield improved margins. Again, comparisons of markets (in this case U.S. versus U.K.) may be interesting but do not necessarily offer a winning solution from a strategy standpoint. The refranchising strategy that the company is pursuing with KFC should insulate the company’s bottom line from the weaknesses in that business somewhat, but alongside the bold (and brave) pronouncements that defined the other segments of the presentation, the management’s tone during commentary on the U.S. market was decidedly cautious. Goal number 3, of the 4 pronged strategy outlined at the outset of the presentation, to “dramatically improve U.S. brand positions, consistency, and returns”, will definitely be the most difficult of all 2011 goals for Yum Brands.

YRI

This was an interesting part of the presentation. YUM is aggressively pursuing growth opportunities in select emerging markets, such as Indonesia, Malaysia, Thailand, and others. The thesis is similar to YUM’s China stance; the consuming class population is set to grow at an even faster rate in “YRI Emerging” markets than in China; set to grow to 2 billion by 2020 from 1.1 billion today versus 450 million to 650 million over the same period in China.

Management was particularly enthusiastic about the prospects for growth via the Asia Franchise Business Unit. There are 4,500 units in operation within these countries where six franchisees own 75% of the units. GDP growth in many of these emerging markets in Asia, such as Malaysia, Thailand, Indonesia, and Vietnam is expected to greatly exceed that of the U.S./Euro area over the next 30 years and, as with the China thesis, it is not hard to understand the appeal. This was truly a presentation of bold statements, from start to finish, and the YRI section held its own in that regard, showing the 7.5 YUM stores per million people in the Asia FBU division versus the 60 YUM stores per million people in the U.S. Undoubtedly the Asia FBU number will grow, but I don’t understand the significance of the (probably over-saturated) U.S. number in this context.

Africa

One of YUM’s goals for 2011 is to “drive aggressive, international expansion and build strong brands everywhere”. Apparently, they meant it. Africa, putting the “A” in “BRICA”, is on the “ground floor of growth”, according to YUM. This is a plan that is in its embryonic stages so it would be wrong of me to be hypercritical at this stage but the thesis certainly did not seem water-tight to me. The GM of the Africa effort made some statements that alarmed me within an otherwise interesting and well-delivered presentation.

One of these was that “Africa has good governance”. I’m not an expert on Africa’s political economy but, merely by following the news, I know that the level of political stability in many African nations is far from good. This is true for several of the nations cited by management as targets for unit expansion with stories abounding of political unrest regularly. A simple news search online can illustrate my point.

I don’t think that this will significantly impact YUM’s earnings power but there are certainly better uses of capital, in my opinion. While the long term debt schedule included in YUM’s folder of slides that was provided for the presentation shows that the company has access to cheap capital, it may not last forever. David Novak underlined the company’s commitment to “watch returns manically” but the company could rue investing capital in some of the African markets mentioned should their projections be overly bullish.

Projections are only as useful as the assumptions implicit in them and I would submit that the estimate of Africa’s GDP hitting $2.6T in 2020 is not very useful given the length of time and the politically and economically volatile nature of African political economies. Again, the extent to which the company will lever itself to the African markets is as yet unknown and can be assumed, for now, to be small. Perhaps this new direction is allied with Chinese investment in Africa, given how important China is as a market for YUM, but I hope that they proceed with more caution than was communicated in the presentation yesterday.

Conclusion

At the end of the day, the strategy of “building brands everywhere” and “growing in China till the cows come home” works until it doesn’t. I’m not suggesting that management won’t stay focused on returns but it will be important to monitor what they do more closely than what they say. Bold statements have set great expectations and it will be important for the company to retain its discipline – something it purports to do – and not become married to a mantra of growing “everywhere”. A change in the macro environment, pertaining to individual companies or to the company’s cost of capital, could be a future risk.

Overall, the company remains an impressive organization but the more it stretches itself, developing new brands and new markets, the more investment it will take to maintain current performance. The 500+ person team employed in almost every province in China is just one example of the infrastructure YUM has built for itself in certain international markets. All in all, no revelations were revealed during yesterday’s meeting. Management was extremely positive and as bold as ever in their projections and outlook for the business. Given the company’s significant growth profile, how the company invests its incremental cash is a vital determinant of the stock price. By that score, as shown in the charts below, 2010 has been a very strong year for YUM.

Howard Penney

Managing Director