TODAY’S S&P 500 SET-UP - December 8, 2010

As we look at today’s set up for the S&P 500, the range is 36 points or -1.57% downside to 1206 and 1.36% upside to 1245. Equity futures continue to hold above fair value but weekly jobless numbers out before the open may determine whether recent strength can be maintained amid deteriorating volumes. Rising bond yields are offering support to financials while the asset class as a whole continues to benefit from a hoped boost to consumption emanating from the extension to tax cuts

- Diamond Foods (DMND) boosted 2011 sales, EPS forecasts

- Linn Energy LLC (LINE) plans 10m-unit offering

- Martek Biosciences (MATK) 1Q EPS forecast below est.

- SAIC (SAI) FY2012 EPS, rev. forecasts below est.

- Stryker (SYK) raises qtr div. 20% to 18c from 15c

- Verint Systems (VRNT) boosted lower end of yr rev. forecast

PERFORMANCE

- One day: Dow +0.12%, S&P +0.37%, Nasdaq +0.41%, Russell 2000 (0.05%)

- Month-to-date: Dow +3.33%, S&P +4.04%, Nasdaq +4.44%, Russell +5.09%;

- Quarter-to-date: Dow +5.42%, S&P +7.63%, Nasdaq +10.16%, Russell +13.00%;

- Year-to-date: Dow +9.06%, S&P +10.15%, Nasdaq +14.98%, Russell +22.17%

- Sector Performance: Financials +1.8%, Tech +0.9%, Consumer Spls +0.3%, Healthcare +0.1%, Telecom 0.00%, Consumer Disc (0.1%), Industrials (0.3%), Energy (0.3%), Utilities (0.5%), Materials (0.9%)

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -685 (-701)

- VOLUME: NYSE 1092.73 (-32.65%)

- VIX: 17.74 --1.39% YTD PERFORMANCE: -18.17%

- SPX PUT/CALL RATIO: 2.05 from 1.29 +59.33%

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 16.73 0.000 (0.001%)

- 3-MONTH T-BILL YIELD: 0.15% +0.01%

- YIELD CURVE: 2.63 from 2.61

COMMODITY/GROWTH EXPECTATION:

- CRB: 316.87 +0.40%

- Oil: 88.28 -0.46%

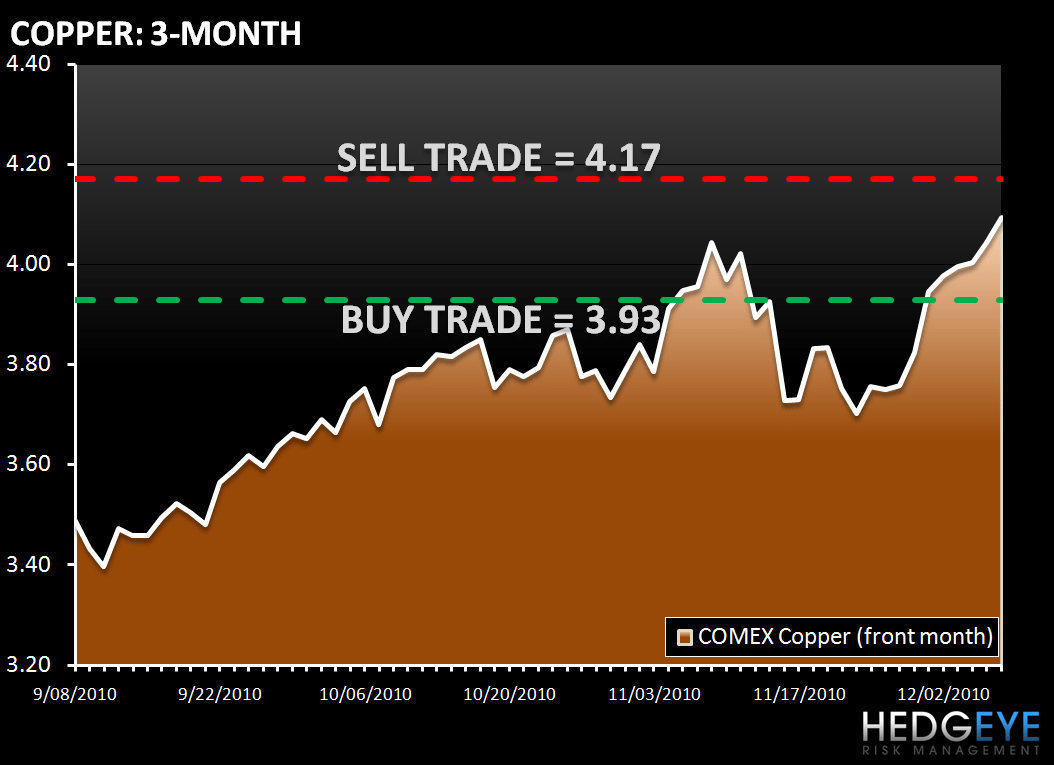

- COPPER: 410.05 +1.26%

- GOLD: 1,381.94 -1.90%

CURRENCIES:

- EURO: 1.3227 -0.56%

- DOLLAR: 79.997 +0.18%

OVERSEAS MARKETS:

EUROPEAN MARKETS:

- European markets opened higher before paring or reversing gains as comments by the ECB over rising unemployment weighed. Corporate results met with a mixed response whilst UK economic news disappointed.

- BOE leave its 0.5% benchmark interest rate and QE measures unchanged.

- France Q3 non-farm payroll +0.2% q/q and prior +0.3%

- Germany Nov Final CPI +1.5% y/y vs prelim +1.5%

- UK Nov Halifax house price index (0.1%) m/m vs con (0.5%), posted first annual fall in a year

- UK Oct trade deficit unexpectedly widened to (£8.53B)

- The pound and the euro are trading at $1.5768 and $1.3211 respectively euro pressured by ECB monthly report saying rising unemployment was concerning, requires effective policy response in order to avoid a persistent increase in structural unemployment and market talk of fund liquidating a long position in illiquid trading conditions.

ASIAN MARKTES:

- Nikkei +0.5%; Hang Seng 0.3%; Shanghai Composite (1.32%)

- Most Asian markets followed Wall Street up today.

- South Korea posted a solid gain; the Bank of Korea’s decision to maintain interest rates did not affect the market.

- Australia rose on a strong jobs report. Banking and resource stocks gained, but retailers declined in sympathy with The Reject Shop, which plunged 21% after lowering FY guidance.

- In Taiwan, Quanta Computer rose 4% on a report it got a contract to assemble the iPad 2.

- On expectations they will benefit from higher long-term interest rates, financials led Japan to a small gain.

- In Hong Kong, China Unicom gained 3% when it cut rates for its entry-level 3G plan.

- Japan Q3 GDP growth revised to +4.5% y/y from preliminary +3.9% y/y.

- Australia November unemployment 5.2%, matching expectations. November jobs added 54,600 vs consensus 19K.

Howard Penney

Managing Director