|

Below is a complimentary research note by our Gaming, Lodging & Leisure analyst Todd Jordan. We are pleased to announce our new Sector Pro Product Gaming, Lodging & Leisure Pro. Click HERE to learn more. |

HEDGEYE EDGE

We’d characterize PENN’s Q3 as disappointing primarily because margins compressed sooner than we thought they would. But the offset was a powerful start to Q4 and market share gains in the OSB/iG segment. So when the stock indicated down slightly, we weren’t surprised.

Then it quickly dropped double digits which seemed like an insane overreaction until we heard about the Portnoy piece in Business Insider nicely timed for PENN’s earnings day. Now it makes sense.

PENN needs to jump on the PR train. The company has been lauded for its diversity and female Board representation and community activity and support. Dave Portnoy is a loose cannon, and we can’t predict how this will all shake out.

He did make a spirited video defense with some evidence to corroborate his case - but this is certainly a wild card. We are, however, pretty sure that PENN’s stock is undervalued. We see $70-75 in share value from PENN’s brick & mortar segment alone. So, in a worst case scenario where PENN’s OSB/iG and Barstool media is worthless, PENN is still a buy.

Q3 | WHAT WENT RIGHT AND WHAT WENT WRONG

- Right

- B&M: Strong October rebound suggests that the core business is back and hitting its stride. October did hold extra weekend days vs 2019, but the South Segment was still reeling with Ida, too. Assuming usual seasonality for B&M, PENN’s Q4 Property EBITDAR (ex. Online/Other) looks above Street expectations by 4-6%.

- Online: Solid momentum articulated for Penn Interactive with market share gains starting to inflect higher through football Season. Live events are giving way to accelerating signups in certain states (like IL) and better retention. PENN also revealed that the Barstool app is now among the highest rated in the App store – so much for the narrative around its clunky tech and poor app. Online momentum has started to build after a 7-8 month slide.

- Wrong

- B&M: Margins compressed more QoQ than the other regional players, which is a net negative but there was added noise in the quarter. Accounting for add backs like the Ida disruption, margins looked less bad but the quarter was messier than we’d like to see. Net/net margins are moderating earlier than we thought.

- Online: Not surprisingly, given our views, OSB/iG costs are running higher as PENN has made a hard push into new markets. Our numbers for PENN’s other segment are coming down for Q4 and for ’22, though admittedly, we have been more optimistic than others on how fast PENN could scale and get to profitability.

OUTLOOK | LET’S FOCUS ON THE B&M STORY

The Dave Portnoy fallout today will be a cloud over the online business – despite its likely acceleration – for at least the time being, so let’s focus on how investors could get paid from here.

We’ve been adamant about the sustainability of topline trends in the regional markets and we think that the GGR releases for the states starting early next week will be a catalyst for the group. Sure, we know what PENN already did in October, but the outlook for Q4 is generally positive and presents a real catalyst.

Beyond Q4, however, we see improving trends well into ’22, with Q1’22 same-store GGR likely to accelerate again from Q4, which makes for a nice setup over the coming 4-6 months.

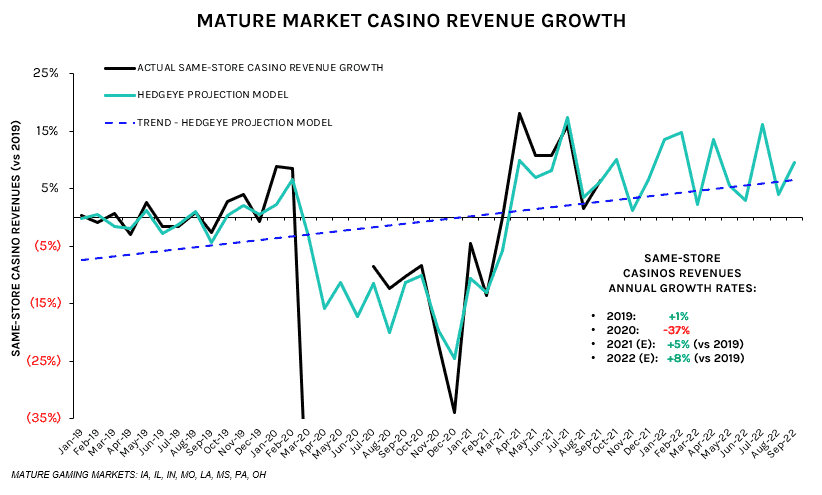

The chart below reflects our reworked Regional GGR seasonality projection model which for now, is still in beta testing mode, but the implied projections are promising, even if we discount some of the implied growth.

Given the volatility (Covid, casino shutdowns, etc.) and often inconsistent trends, we had discontinued our projection model, but with data getting a little more consistent (ex. weather) as Covid recedes, we’re gaining confidence in the model’s forward looking power.

We’re running the analysis exclusive of Sports Betting given that it is not universally offered across all the states observed in the analysis. Either way, given the much lower incremental margin on retail Sports Betting revenues, the real EBITDA upside would naturally come from slots and tables.

Additionally, if there is an extra pick up (or setback) in slots or table trends, our model would capture it and those trends would be carried forward in our estimates. We look forward to publishing this on a more frequent basis.

VALUE | B&M BIZ WORTH MORE THAN EV, WITH OR WITHOUT PORTNOY

The Portnoy situation is a difficult one to handicap – he did bounce back quickly from the sex tape fiasco and his spirited video defense (see here) offered some corroborating text information but the article was certainly not a good look.

It might be a while before PENN gets any credit for SB/iG or the Barstool media business.

Of course, even under a bad case scenario there is value but even allocating $0 in valuation credit to those future business lines, we see PENN worth at least $70 per share on a standalone, pre-Barstool pre-theScore. Our valuation assumptions can be found below.

The cash flow generation inherent in PENN’s regional portfolio should be robust for years to come as we have outlined multiple times in the last 4-5mths, and as of today, it’s on sale, big time.