This note was originally published at 8am this morning, December 08, 2010. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“The individual’s power to operate something with a deficit is very limited.”

-Ludwig von Mises

I think people who run their own companies (or lives) without government bailout support get this very simple point. It’s Darwinian.

Most modern day federal governments, however, don’t have to have any experience in the simple matter of balancing a budget. As the late Austrian economist, Ludwig von Mises, astutely pointed out, “for the government, conditions are different. The government can run a deficit, because it has the power to tax people.” (Economic Policy, von Mises’ 3rd Lecture, “Interventionism”, page 28)

Well what happens if a government that’s running a deficit doesn’t have the political spine to tax people? Simple answer. The risk associated with that government’s sovereign debt goes up. That’s the price of fiscal irresponsibility. Try this at home with your credit card debt and you’ll get the point.

Yesterday was a fascinating day in the US stock market. In risk management speak we call what happened an “outside reversal.” Essentially, outside reversals occur when some buy-and-hope event (extending the Bush tax cuts) sends US stock market futures soaring to fresh YTD highs… but then they fade intraday on heavy volume… and close below the prior YTD closing high. An outside reversal is a bearish immediate-term signal.

The 2010 YTD high for the SP500 is 1225. Intraday, the market registered readings as high as 1234 (on the open at 945AM EST when emotional decisions run rampant), but sold off hard into the close to settle down at 1223.

All the while, US Treasury yields were screaming higher. They were telling you, Mr. Shortermism of Political Career Risk Management, that CUTTING taxes when you have a massive deficit problem = sovereign debt risk.

So, if you are a government… and you have a debt financed deficit spending problem… and you can’t tax anyone… what do you do? This is not a trick question. There’s only one answer the Fiat Fools have for this – INFLATE.

In fact, it was the forefather of Big Government Intervention, John Maynard Keynes himself, who wrote in his 1936 manifesto, the General Theory of Employment, Interest and Money, that “if one devalues the currency and the workers are not clever enough to realize it, they will not offer resistance against a drop in real wage rates, as long as nominal wage rates remain the same.”

Sorry to Messrs Bush, Obama, and The Ber-nank. This Canadian American’s workers are Clever Enough.

If the ideological submission by the Keynesians is that:

- Markets are rational, and

- American workers are stupid…

I’ll comfortably sit on the common man’s side of that trade.

If the conclusion is that we can load American 301ks with bond fund allocations and no one will notice when they get ploughed, we’ll take the other side of that theoretical trade too. Inflation is bad for bonds.

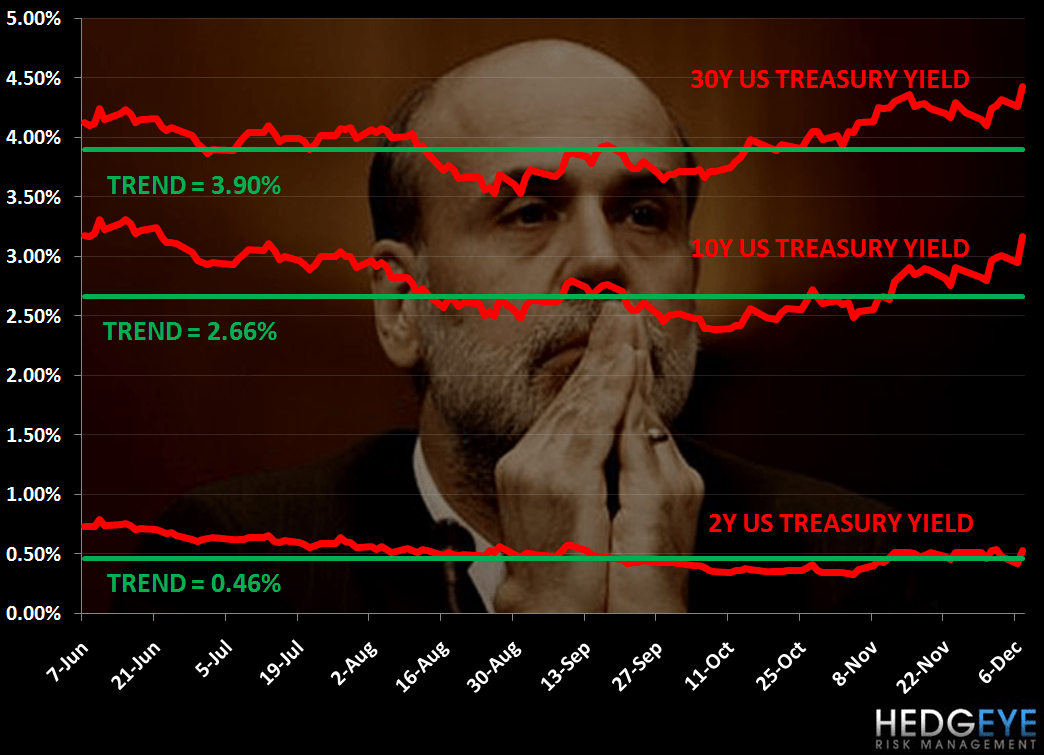

Both US and Global Bond Yields are all of a sudden making a credible threat to break out into what we call a Bullish Formation (bullish on all 3 of our core investment durations: TRADE, TREND, and TAIL). The corollary to this is that sovereign bonds (including US Treasuries) are moving into a Bearish Formation. This is not what The Ber-nank ordered.

The following lines are the bullish intermediate-term TREND lines of support across the US Treasury Yield Curve:

- 2-year yields = 0.46%

- 10-year yield = 2.66%

- 30-year yields = 3.90%

In other words, bond yields are trading significantly above their intermediate-term TREND lines of support and bond funds are breaking down, hard, as a result. Maybe that’s why this morning’s ABC Consumer Confidence reading remains astonishingly low at -45 (that’s a minus 45, less than 10 points off its all-time lows) on the weekly print, despite the US stock market having a monster move of +2.9% to the upside in that week.

Maybe Americans don’t own as many stocks as they did when they had 401ks…

Maybe someone stuffed their 301ks with bond fund allocations at a bond market top…

Maybe Americans are Clever Enough to know what’s happening to their money when A) the government can’t tax and B) has chosen to inflate…

My immediate term support and resistance levels for the SP500 are now 1206 and 1239, respectively. I’ve dropped the Hedgeye Asset Allocation to Bonds to 6% in the last month and I remain short the SP500 via the SPY in the Hedgeye Portfolio.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer