TODAY’S S&P 500 SET-UP - December 8, 2010

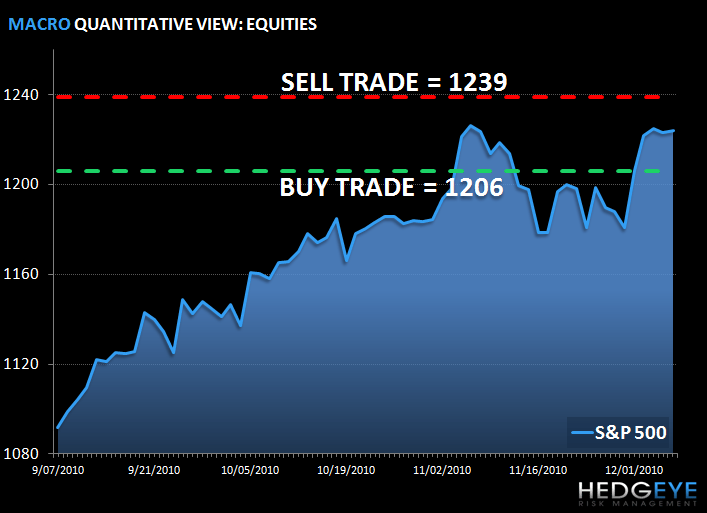

As we look at today’s set up for the S&P 500, the range is 33 points or -1.45% downside to 1206 and 1.25% upside to 1239. Equity futures are trading mixed to fair value following Tuesday's up-and-down session which left major stock indices little changed on the day. Of note yesterday, 10 and 30 year T-bond yields hit 5-and-half month highs in reaction to the extension to tax cuts. Moody's warned that the tax cut extension, if made permanent and no offsetting measures were put in place, could put downward pressure on the US Aaa credit rating.

- AeroVironment (AVAV) 2Q EPS 1c vs est. loss-shr 6c

- Mitcham Industries (MIND) 3Q EPS 7c vs est. 6c

- Men’s Wearhouse (MW) sees 4Q adj. loss-shr wider than est.

- Netflix (NFLX) CFO Barry McCarthy to leave

- Orexigen Therapeutics (OREX) OREX’s diet pill wins FDA panel backing

- Starwood Property Trust (STWD) plans 20m-shr secondary

- Texas Instruments (TXN) narrows 4Q EPS, sales forecast

- Costco (COST) posted 4Q EPS that beat est.

PERFORMANCE

- One day: Dow (0.03%), S&P 0.05%, Nasdaq +0.14%, Russell (-0.03%)

- Year-to-date: Dow +8.93%, S&P +9.74%, Nasdaq +14.51%, Russell +22.23%

- Sector Performance: Energy (-0.38%), Tech +0.12%, Materials +0.13%, Consumer Discretionary 0.05%, Telecom (0.03%), Industrials 0.27%, Financials 0.16%, Consumer Staples 0.56%, Utilities (0.67%), and Healthcare 0.06%

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 16 (+580)

- VOLUME: NYSE 1622.36 (+101.88%)

- VIX: 17.99 -0.17% YTD PERFORMANCE: -17.02%

- SPX PUT/CALL RATIO: 1.29 from 1.32 -2.37%

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 16.93 -0.102 (-0.569%)

- 3-MONTH T-BILL YIELD: 0.14% -0.01%

- YIELD CURVE: 2.61 from 2.53

COMMODITY/GROWTH EXPECTATION:

- CRB: 315.62 -0.53%

- Oil: 88.69 -0.77%

- COPPER: 404.95 +1.04%

- GOLD: 1,408.650 -0.44%

CURRENCIES:

- EURO: 1.3302 +0.04%

- DOLLAR: 79.857 +0.36%

OVERSEAS MARKETS:

EUROPEAN MARKETS:

- European markets have fluctuated either side of unchanged in a relatively tight range after hitting their highest levels in over two years yesterday.

- Participants assessed Ireland's austerity budget and the lack of quantitative action by EU finance ministers as worries over the regions sovereign debt crisis refuse to go away.

- Commodity prices saw profit taking after sharp recent gains.

- Advancing sectors lead decliners 11-7 with insurance the leading gainer, whilst personal & household products led fallers.

- The Irish equity market is little changed, whilst peripheral markets including Spain +0.6% and Italy +0.8%, led the regions gains.

- Bank of France Nov industry sentiment indicator 107 vs prior 104, Bank of France raises Q4 GDP forecast to +0.6% vs prior estimate +0.5%

ASIAN MARKTES:

- Asian markets were mixed today.

- Japan advanced on a softer yen.

- Taiwan finished flat.

- South Korea declined slightly as falls in shipbuilders outweighed gains in tech stocks.

- Australia declined, but Aston Resources gained 5% on selling a stake in a mine to Itochu.

- China fell on worries about higher interest rates. Railway stocks were strong on reports that the government plans to invest $600B in high-speed rail networks.

- Chinese banks fell 2% on a belief that China will raise interest rates this weekend, and deposit rates may go up faster than lending rates do.

- Japan October current account surplus ¥1.436T, +2.9% y/y. October machinery orders (1.4%) m/m vs (0.1%) consensus.

Howard Penney

Managing Director