Revolving Consumer Credit Still Sinking, but Nonrevolving Credit Shows Growth

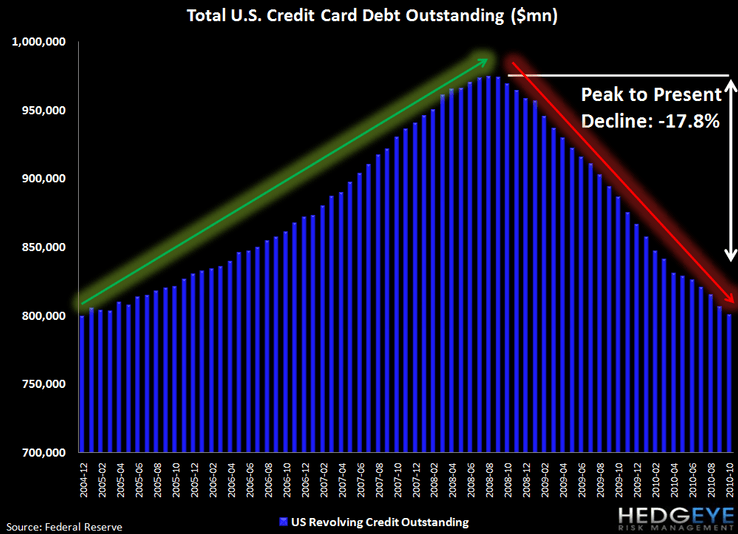

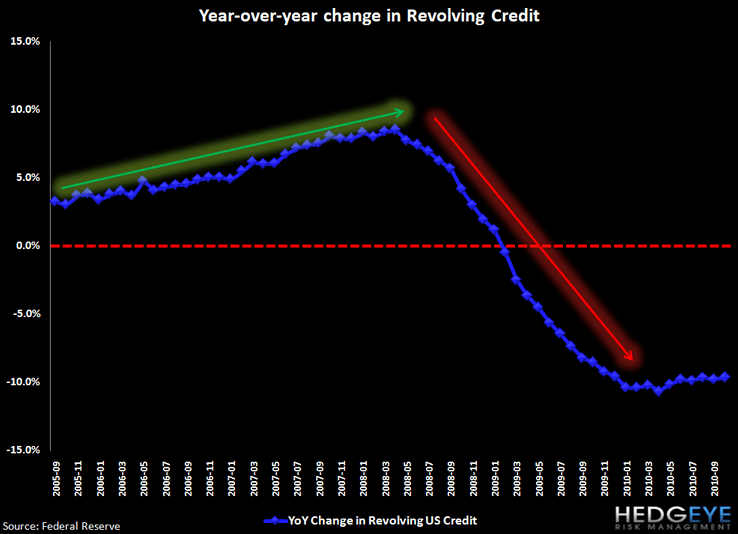

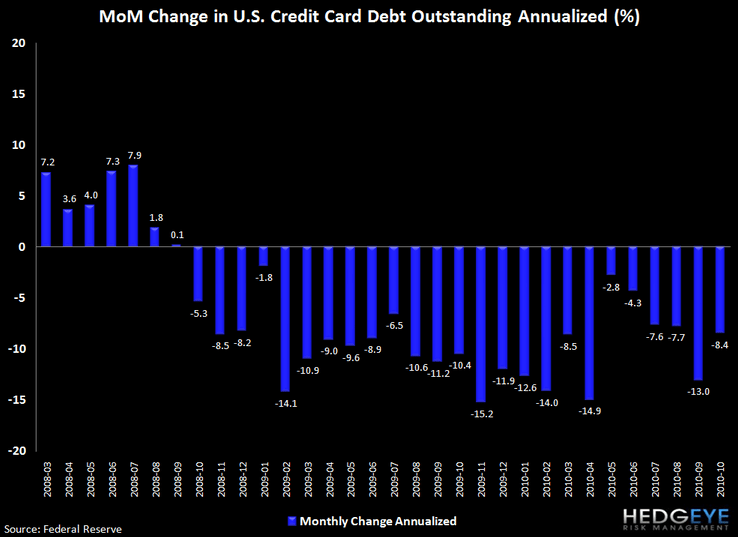

Just-released October G.19 data showed another decline in revolving credit, along with significant downward revisions to earlier data points. G.19 measures non-mortgage consumer credit: credit card, auto and student loan debt. While the month-over-month decline in revolving credit was not as severe as the September print (-13.0%, revised down from -12.1%), it remains far from healthy. Revolving credit (i.e. card debt), the piece we are most focused on, fell -8.4% (MoM annualized) to $800B. Currently, the peak to trough decline in revolving consumer credit stands at -17.8%, or $173B.

The ongoing deleveraging by the consumer is alive and well. Contrary to media reports that the principal driver of deleveraging is actually charge-offs, charge-offs represent less than half of the deleveraging that we've seen in consumer credit to date. This marks the 25th consecutive month in which aggregate credit card debt has declined. Prior to this contraction, the longest drawdown in consumer revolving credit lasted just five months.

Nonrevolving credit (auto and student loans) rose 6.8% in October vs +7.6% in September (revised from +7.9%). With the strength from nonrevolving credit leading the way, overall nonmortgage credit increased for the second month in a row, rising 1.7% (MoM annualized).

Overall bank loans have declined 12% since the peak in late 2008, as seen below in the H.8 series.

The Financials with the greatest exposure to credit card receivables are shown below, including JPMorgan (JPM), Bank of America (BAC), Citigroup (C), American Express (AXP), Capital One (COF), and Discover (DFS).

Overall, total non-mortgage credit increased 1.7%, or $3.4B, as shown in the following charts.

Joshua Steiner, CFA

Allison Kaptur