As part of the Bush tax cut compromise, it looks like Obama’s 2011 proposal for full deduction for equipment purchases will pass.

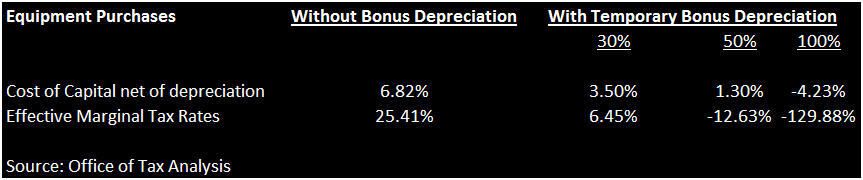

As we wrote about in “DARE WE SAY THERE MIGHT BE A NEAR TERM REPLACEMENT CATALYST” (09/16/10), Obama’s temporary 100% expensing proposal would allow companies to immediately deduct the full cost of equipment purchased between Sept 8, 2010 and Dec 31, 2011. For equipment purchases, the complete write-off will lower overall effective tax rates and the cost of capital as shown below.

We believe the passage of this proposal comes at an opportune time as casino operators remain cautious about investing during the current recovery. Accelerated depreciation could help spark the long-awaited recovery in replacement demand.

Appendix: Treasury Report highlights