It’s gotten colder out and frappes and smoothies are slowing down considerably. The hot lattes are not making up the difference. McRib was a social media darling but it did not move the needle that much.

McDonald’s is scheduled to report its November sales numbers before the market open on Wednesday, December 8th. November had one less Sunday, and one additional Tuesday, than November 2009. Based on this, it seems possible that there may be a negative sales shift.

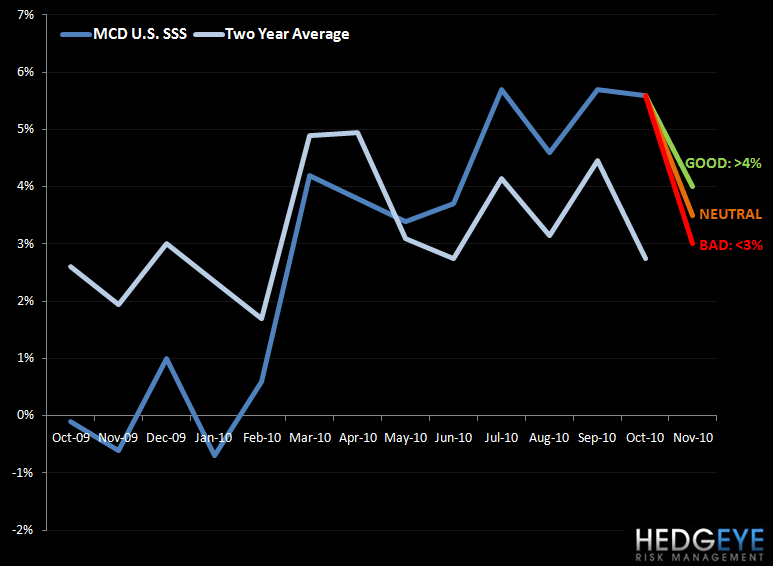

Consensus estimates are calling for comparable store sales numbers in line in the U.S., slowing down in Europe, and slightly positive sequentially in APMEA. On a relative basis, MCD continues to out-gun the competition. However, I am seeing a slight slowdown in sales trends for MCD and I believe that consensus may be overly optimistic for November.

To recall, October comparable restaurant sales numbers from McDonalds indicated a slowdown in the U.S. region based on two-year average trends. For comparison purposes, I have adjusted for calendar and trading day impacts. Europe and APMEA both slowed in October following strong results in September on a two-year average basis. In November, Europe and APMEA need to print strong headline comparable restaurant sales numbers to maintain two-year average trends.

U.S. – facing an easy -0.6% compare (including a calendar shift which impacted results by -0.9% to -1.7%, varying by area of the world): As of today, consensus is forecasting a print of 5.1% for McDonalds U.S. region comparable store sales in November.

GOOD: A print of more than 4% would be perceived as a good result as it would imply that the company improved two-year average trends by 50 basis points or more. While this would not bring trends back to the lofty levels seen in the summer months, it is perhaps unrealistic to expect a repeat of those numbers in the absence of hot weather-induced beverage and smoothie sales.

NEUTRAL: Roughly 3% to 4% implies two-year average trends that are approximately flat versus trends seen in October. Of course, this would indicate that two-year average comparable restaurant sales were significantly below summer levels. The summer sales of frappes and smoothies are well and truly behind the company as winter sets in.

BAD: Below 3% would indicate a further decline in two-year average trends in MCD’s U.S. business from October’s

significant decline. It would also imply the lowest comparable restaurant sales number since February.

Europe – facing an easy +2.5% compare (including a calendar shift which impacted results by -0.9% to -1.7%, varying by area of the world): As of today, the consensus estimate is for Europe to post +4.9% comparable restaurant sales growth.

GOOD: A print of roughly 7.5% or higher would imply two-year average trends slightly below or above the two year average trends seen in October. October was a strong month in Europe for MCD but a significantly higher print will be required to maintain two-year average trends. A 7.5% number would be the strongest result since May 2009.

NEUTRAL: A result of 5.5% to 7.5% would imply that sequential trends had decelerated by up to approximately 100 basis points. 5.5% is still a relatively high level; in fact, it exceeds all months’ results year to date except for March, May and October. Offsetting that positive aspect is the fact that two-year trends would slow sharply. In addition, a relatively high number is to be expected against a poor 2.5% print for November 2009.

BAD: Less than 5.5% would imply a deceleration of more than 100 basis points in two-year average trends from October. Furthermore, two-year average trends would fall below 5%, which, with the exception of August, has not happened since February 2010.

APMEA – facing an easy -1.0% compare (including a calendar shift which impacted results by -0.9% to -1.7%, varying by area of the world): As of today, the consensus estimate is for APMEA to post +6.4% in same-store sales growth.

GOOD: Roughly 9% or higher would imply a steady-to-slight acceleration from the results seen in October. October saw a significant slowdown in MCD’s APMEA business on a two-year average comparable restaurant sales basis. A lofty headline print is likely given the weak result of a year ago. The two-year trend implied by this print will be important to watch.

NEUTRAL: Between 8% and 9% would imply two-year average trends slightly lower than those seen in October.

BAD: Below 8% would imply a significant slowdown from the two-year average trend in October and a return to the level of two-year average trends seen in June, which was a lackluster month for MCD APMEA.

Howard Penney

Managing Director