Hedgeye Position: Long Germany (EWG); Short Euro (FXE), Short Italy (EWI)

Yesterday we shorted Italy and the EUR-USD off a two-day bounce in equities and declines in peripheral yields. We called out the move as a dead-cat bounce and continue to stress that despite immediate term market swings, over the intermediate to longer term we expect the risk premium across Europe to remain elevated as the risk associated with the sovereign debt contagion spreads to the likes of Portugal, Spain and Italy.

That said, we’re seeing another day-over-day decline in risk via 10yr bond yields from the PIGS (except Italy) that is worth a call-out (see chart below). Further the EUR-USD has gained ground, currently at $1.3365, which we shorted into.

This lift comes into and out of ECB President Jean-ClaudeTrichet’s announcement yesterday morning to hold the ECB’s benchmark lending rate steady at 1%, and no step-up to its €67 Billion bond purchasing program, which the market was largely speculating on given the Fed’s $600 Billion QE2 injection (Quantitative Guessing) and the Bank of England’s larger bond purchasing program of £200 Billion.

The ECB will keep offering banks unlimited loans through the first quarter over periods of seven days, one month, and three months. That marks a shift from last month, when Trichet said that the ECB could start limiting access to its funds, a position long voiced by Bundesbank President Axel Weber.

Positive Data, on the margin

-The Bundesbank revised upward its GDP forecast for Germany in its bi-annual economic outlook today:

3.6% in 2010 (vs June estimate of 1.9%)

2.0% in 2011 (vs 1.4%)

1.5% in 2012

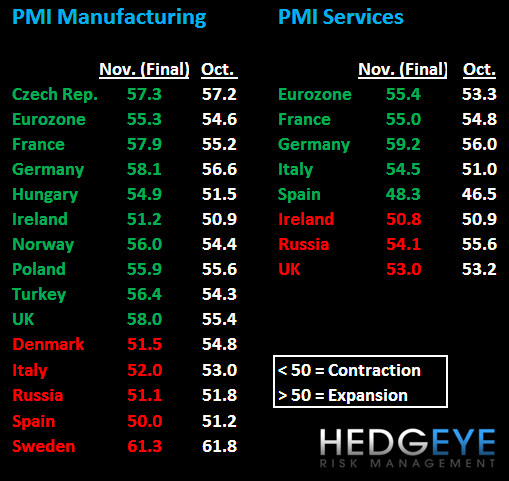

-Final readings of November Manufacturing and Services PMIs, released on Wednesday and today, respectively, showed month-over-month gains for the majority of the reporting countries:

Positive Divergences: UK Manufacturing rose to 58.0 in November versus 55.4 in October and Germany Services jumped to 59.2 vs. 56.0.

Negative Divergence: Spain Services rose M/M to 48.4 but remain under the 50 line, denoting contraction. Italy Manufacturing fell to 52.0 vs 53.0.

Keep your risk management pants on and have a great weekend!

Matthew Hedrick

Analyst