The guest commentary below was written by Joseph Y. Calhoun, III of Alhambra Investments on 10/24/21. This piece does not necessarily reflect the opinions of Hedgeye.

The S&P 500 and Dow Jones Industrial stock averages made new all-time highs last week as bonds sold off, the 10-year Treasury note yield briefly breaking above 1.7% before a pretty good-sized rally Friday brought the yield back to 1.65%.

And thus we’re right back where we were at the end of March when the 10-year yield hit its high for the year. Or are we? Well, yes, the 10-year is back where it was but that doesn’t mean everything else is and, as you’ve probably guessed, they aren’t.

In the early part of this year, the 10-year yield was rising as anticipation built for a surge in post-vaccination economic growth. The 10-year yield rose about 85 basis points from the beginning of the year to the peak in late March.

10-year TIPS yields, meanwhile, were also rising, a little more than 50 basis points. There was agreement between the two that growth expectations were improving, inflation expectations rising a bit more than real growth expectations.

The 10-year Treasury ended March right about where it was last Thursday, 1.7%. But there is considerably less agreement between the two markets now with the 10-year TIPS yield still 35 basis points lower (more negative) than the March peak.

So, no, things are not back where they were.

The recent rise in nominal bond yields is much more about inflation fears than growth hopes. Markets provide us with a wealth of information that allows us, to some degree, to get inside the heads of investors.

The changes in the bond markets recently show that investors have a very specific and nuanced view of the economy. They are certainly concerned about inflation and doing what people do when they are scared – trying to protect themselves.

TIPS have been very popular of late for exactly that reason, as the inflation narrative gets louder and louder. But what is interesting is that, in a way, investors are taking the Fed at its word, that the inflation is transitory.

The 5-year breakeven inflation rate hit 2.91% last week while the 10-year rose to 2.64%. But the 5-year, 5-year forward rate (5-year inflation expectations starting 5 years hence), has fallen over the last week to 2.37%.

Investors think inflation will average nearly 3% over the next 5 years but less than 2.4% over the following 5. So investors do see inflation as transitory even if their definition of the term seems quite a bit different than the Fed’s.

Another big difference between now and March is the steepness of the yield curve. The 2-year note yield has been on a steep rise of late, up 140% since the beginning of September, with most of that coming in October.

The 2-year rate roughly doubled in the early part of the year too, but the absolute change was small because rates started so low. The recent change in the 2-year has been more rapid than the 10 and is being driven by expectations for Fed policy changes.

The 10/2 curve was 1.58% at the end of March but just 1.18% today. The short-term trend is still toward steeper but the climb has stalled a bit:

I interpret these changes in the obvious way. Nominal growth expectations are rising with most of the recent change focused on inflation but with some pickup in real growth expectations too.

In addition, investors do not seem willing to believe yet that inflation is a long-term problem. Given the high profile of the inflation narrative and the lack of concrete evidence of a growth pickup, these changes seem perfectly rational and reasonable.

I think it is important to note too that these changes in inflation expectations are small but also rapid. The 10-year breakeven rate is up about 65 basis points this year but over half of that has happened in the last month.

The same is true for the 5-year breakeven rate. As for the change in real growth expectations, I’d just say that it isn’t very impressive regardless of the rate of change. Unfortunately, that makes sense too since, as I discussed last week, we haven’t done anything to change the trajectory of either workforce or productivity growth.

My long-term expectation for growth hasn’t changed much since the first few months of COVID. We came into it with growth averaging roughly 2.2% over the previous decade.

After adding a lot of debt to that economy during the pandemic, my assumption is that, when things finally settle out from the virus and the response to it, economic growth will be lower. How much? I don’t know of any way to quantify that.

But that long-term expectation is just that, long term. It doesn’t say anything about growth over the near term, the next 6 to 12 months. We’ll get a report on Q3 GDP next week and all indications are that it will be a pretty big fall off from the first half of the year.

But anyone who’s been paying the slightest bit of attention knows that so it really won’t matter. Investors will be focused on the current quarter and the one after that.

Will there be a reacceleration in growth as the delta variant fades?

Will businesses be able to get goods for Christmas or will America get a lump of coal in its stocking? Or are we out of coal too?

I don’t know but I do think we need to be careful about getting too negative about, at least, the immediate future.

Inflation expectations can change rapidly while growth expectations take more time so TIPS and nominal yields are often on different songs, even if in the same hymnal.

I don’t generally put much emphasis on the PMIs or regional Fed surveys. They are basically sentiment surveys and rely on people’s anecdotal observations which, as we know, can be skewed for a whole host of reasons.

But they can be interesting at turning points, inflection points, where sentiment does have a bearing on actions and ultimately the economy. While I don’t think we’re near a negative inflection point, the Philly Fed survey and the Markit PMIs do seem to point to a more positive near-term outlook.

The Philly Fed survey itself was down considerably from September but it is still higher than 3 months ago and the details hint at a near-term pickup. The new orders index rose to 30.8 from 15.9, employment to 30.7 from 26.3.

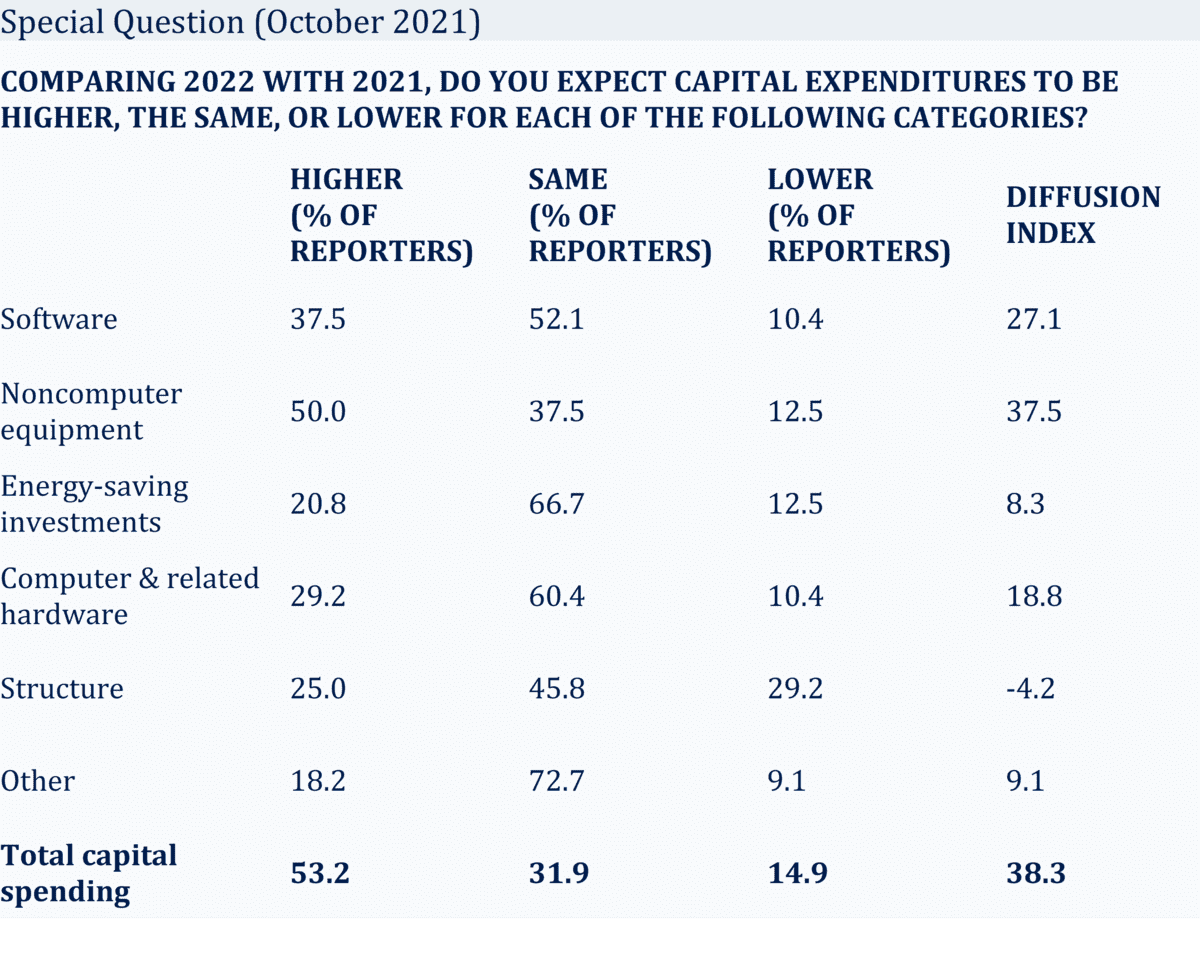

They also asked a special question about capital spending plans that showed expectations for increased spending in 5 of 6 categories for next year:

Of course, those expectations could change dramatically if Q4 turns out to be a bust but it is, for now, a positive indication for future growth.

The Markit PMIs also offered some near-term optimism as the overall measure rose to 57.3 from 55 in September. That’s the best in 3 months with a sharp rise in service sector activity and a 3rd consecutive month of slowing in manufacturing activity (which is still at a high level).

New orders in services rose at the fastest pace in 3 months. Job creation was the highest since June although companies still report having a hard time finding workers.

All of this is perfectly consistent with the expectations for a growth resurgence post delta. Will those expectations be met?

I don’t know obviously but if these expectations start to be met, we should see a response in the bond market with better balance between TIPS and nominal bonds.

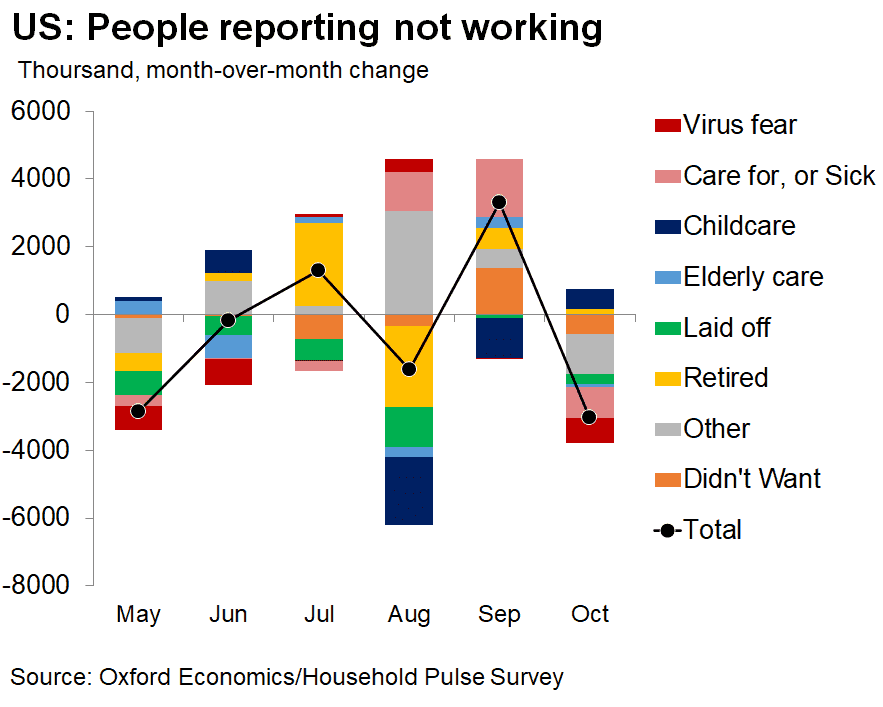

There was also some potentially good news in the Census Bureau’s weekly household pulse survey which showed a big drop in people reporting not working.

Again, I don’t think we should put a lot of emphasis on these surveys. I’m always more interested in what people are doing rather than what they say they’re doing and especially what they say they intend to do. But these seem to be more significant changes than we’d normally see month to month.

We’re going through a bit of an inflation scare right now and we can see the changes in markets. They are fairly small changes though and they can, probably will, change again in the coming weeks.

Growth and inflation expectations are always changing as new information enters the market. Millions of investors speculate about how the future will look and their bets on that future move markets as new consensus expectations emerge.

And the market changes that come from these new expectations also affect the economy in an ongoing feedback loop that changes expectations and markets again in a never-ending search for equilibrium.

The ebb and flow of the markets and the economy are intertwined, one influencing the other to produce the best prediction of the future we’ll ever get. Just don’t get too attached to that future because it can – and often does – change quickly.

|

Click HERE if you want to continue reading the full note. |

EDITOR'S NOTE

Joe Calhoun is the President of Alhambra Investments, an SEC-registered Investment Advisory firm doing business since 2006. Joe developed Alhambra's unique all-weather, multiple asset class portfolios. This piece does not necessarily reflect the opinions of Hedgeye.