MACAU NOVEMBER DETAILS

The growth train kept on chugging in November despite tough hold and growth comparisons. Total revenues grew 42% to $2.17 billion. Table revenues grew 43% YoY, on top of a 63% growth rate in Nov 2009. Mass market table revenue grew 29% while VIP revenues climbed 48%. VIP revenues accounted for 77% of the total table revenues. Direct play appears to have increased to 8.7% of VIP compared to 7.3% a year ago. Adjusted for direct play, market VIP hold appears to be about 3.04%, just slightly lower than last year's 3.09%. December has an easier hold comparison, as our estimate of December 09 hold was only 2.74%.

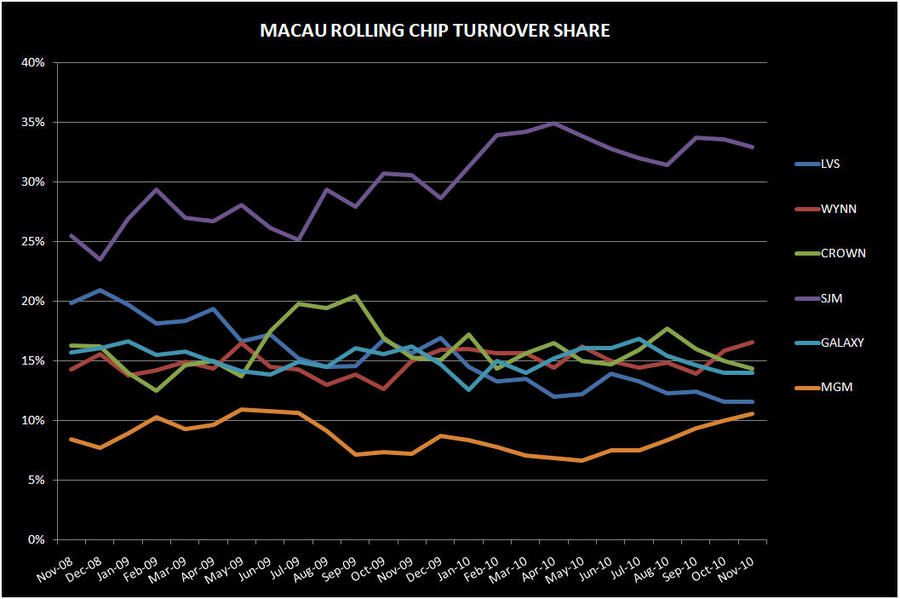

Wynn was the big share gainer in the month of November while LVS was a big donor. Lady luck was the primary driver of this divergence of fortune. SJM also lost 1% of its market share while the other 3 concessionaires picked up some share with MPEL gaining 80bps and MGM climbing by another 50bps. In terms of Mass share, LVS and WYNN lost share sequentially while MPEL, SJM, Galaxy, and MGM gained.

YoY Table Revenue Observations

LVS table revenues only grew 2% - 20% growth in Mass revenues offset by a 6.7% decrease in VIP revenues. VIP suffered from the combination of low hold and difficult hold comparisons.

- Sands decreased 7%, the second month of sequential declines and with growth of only 6% over the last 5 months despite the market growing 59%. Part of the underperformance is due to difficult hold comparisons.

- VIP revenues declined 17% despite a 10% increase in Junket RC volume

- 16% increase in Mass revenues

- Low hold was the culprit behind VIP revenue declines. Assuming 14% direct VIP play (same as 2Q & 3Q2010), we estimate that hold for November was 2.5% which compares to 3.3% hold last November, assuming 9% direct play (in-line with 4Q09).

- Venetian was up 11%

- VIP revenues only increased 5.5% on a 28% increase in Junket RC due to a difficult hold comparison

- Mass revenues increased 21%

- Assuming 23% direct VIP play volume, we estimate that hold for November was 2.7% compared to 3.5% last November if we assume that direct play was 17% (in-line with 4Q09 levels).

- Four Seasons decreased 17%

- Mass revenues grew 34%

- VIP revenues decreased 28% on a 41% decrease in Junket VIP RC volume on very low hold despite easy comparisons

- Assuming $525MM of direct VIP play or 50% in November, implied hold is 1.7% compared to 2.3% in November 2009 assuming direct play was 28% (consistent with 4Q09)

Wynn Macau/Encore table revenues were up 101%, driven by an 113% increase in VIP revenues and a 52% increase in Mass revenues

- Junket RC volume increased 64%. Assuming 13% direct VIP play, November hold was 3.3% compared to an easy comparison of 2.5% hold experienced in November 2009 (assuming 12% direct play)

MPEL table revenues grew 57% with the growth driven by a 64% increase in VIP and Mass growth of 57%

- Altira was up 63%, due to a 62% increase in VIP revenues and a 92% increase in Mass revenues

- VIP revenue growth was partly driven by high hold as RC grew only 32%

- We estimate that hold in November was 3.5% vs. 2.8% in November 2009

- CoD table revenue increased 106.5% YoY, driven by 51% growth in Mass and 66% growth in VIP revenues

- Junket VIP RC increased 46%

- Hold benefited CoD's market share. Assuming 15% direct VIP play, hold was 3.3% compared to last November's hold of 2.9% assuming 18% direct play

SJM table revenues grew 38%

- Mass was up 22% and VIP was up 47%

- Junket RC volumes increased 59%

- SJM's hold was 3%, compared to 3.25% in November 2009. December will have an easier hold comparison since last December's hold rate was 2.8%.

Galaxy table revenue only increased 20%, driven by a 22% increase in VIP win and a 10% increase in Mass

- Starworld's table revenue increased 22%, driven by 23% growth in VIP revenues and 18% growth in Mass

- The Group RC volumes were up 28% while Starworld RC volumes increased 35%. Despite hold being normal, the comparisons from November 2009 were difficult. November hold for the Group and Starworld was 2.8%, respectively, compared to last November's hold of 3.0% and 3.1% last year.

MGM reported the strongest growth in the month of November, with table rev growth of 81%

- Mass revenue growth was 55%, while VIP revenues grew 88%

- VIP RC grew 117%

- Hold was high, at an estimated 3.2% but it was even higher last November at 3.6%

Table Market Share

LVS table share dropped 370bps sequentially to 14.8%, an all-time low for LVS since we've been tracking the data (March 2007)

- LVS's share of VIP revenues dropped 4.3% to 11.9%, its lowest share since we've been getting data (March 2007).

- RC share was flat sequentially at 11.6%.

- Mass share fell 1.7% to 24.5%

- Sands market share decreased by 50bps due to a 70bps loss in VIP share

- Venetian lost 2% to 8.7% sequentially, driven mostly by losses in both VIP and Mass share which were impacted by difficult hold comparisons

- FS share dropped 130bps to 1.2% due to a 160bps loss in VIP share

WYNN's table share increased 340bps to 17%

- Mass market decreased 50bps to 10.9%

- VIP revenue share increased 4.6% to 18.8% sequentially

- Wynn's VIP share jumped to 2nd place behind SJM

MPEL's market share increased 70bps sequentially to 14.7% in November, driven by a 30bps increase in Mass and an 80bps increase in VIP share

- CoD's share decreased 20bps

- Altira's share increased 80%, driven by a 1% increase in VIP share

SJM's share decreased by 1.2% to 32.1%

- SJM's share gain was driven by a 70bs gain in Mass share to 40.3% which was offset by 1.8% decrease in VIP share

Galaxy's inched up 20bps to to 10.3%

- The Group's share gain was driven by a 90bps gain in Mass market share

- Starworld's market share increased 40bps sequentially to 8.5%

- Junket RC share was flat sequentially at 14%

MGM's share continued its climb to 11.2%, the property's highest share since July 2009

- MGM's share gain can be attributed to a 70bps increase in VIP and a 40bps increase in Mass

- RC share increased 60bps to 10.6%

November Slot Revenue Observations

Slot revenue grew 21% YoY in November reaching a total of $92MM and accounting for 4% of total revenues

- MPEL experienced the largest growth of 69% to $20MM

- MGM's slot revenue increased 43% to $12MM

- Galaxy's slot revenue increased 43% to $3MM

- LVS, having the largest base, barely grew - only 1.3% (YoY) to $26MM

- Wynn's slot revenue increased 13% to $19MM

- SJM's slot revenue grew 7% to $12MM