“You never see the old austerity. That was the essence of civility; young people hereabouts, unbridled, now just want.”

-Moliere

That’s an old quote from a famous French playwright who has long been dead. “Moliere” was Jean-Baptiste Poquelin’s stage name. His urban legend was born when he collapsed and died in the middle of a play in 1673. He was 51 years old.

I’ll take some editorial liberty this morning and evolve Moliere’s quote for the Age of American Millenials and Baby Boomers: ‘You’ve never seen austerity. That was the essence of our grandparents; Millenials and their parents, unbridled, now just want.’

This is obviously a generalization but, in principle, I can’t imagine that an analyst from outer-space wouldn’t see the hypocrisy in Americans door busting each other on Black Friday for i-Pads at the same time as their Congress fights to keep interest rates on my savings account at zero percent as a result of an alleged depression.

Want, want, want. What can I get out of this market? Pretended Patriotism be damned, what’s in this for me?

The good and the bad news on this front is that we have leaders in this country who can enforce change. Some of that change is going to be slow. Some of it is going to hurt. Some of it is needed or what you’re seeing in European stock and bond markets is going to be playing at an American “Lifestyle” Center near you in 2011.

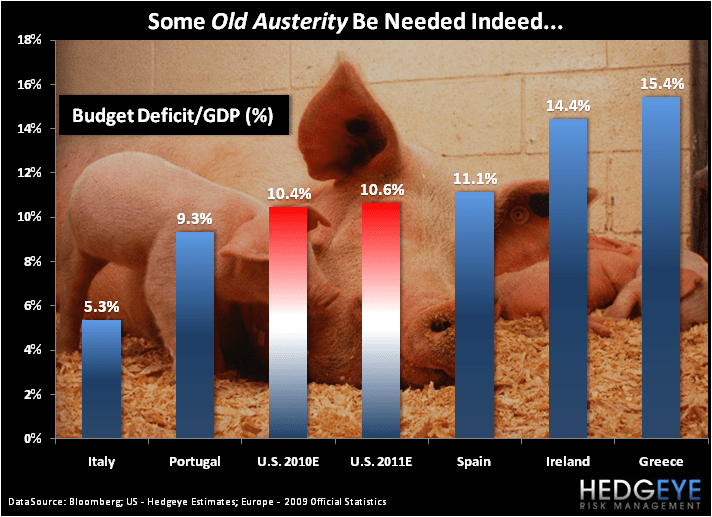

In proposing a 2-year pay freeze for US Federal employees, President Obama did the right thing yesterday in implementing the first stage of what we have been calling for since July of 2010 (when we were short the US Dollar on reckless government spending). Our Q3 of 2010 Hedgeye Macro Theme was titled “American Austerity” and we think that fiscal conservatism is the only path to US Dollar driven prosperity.

The debauching and devaluation experiments of the Big Government Interventionists have been tested and tried. From Japan to Europe and back home again, they have not worked. We need to fix these deficit and debt to GDP ratios, or the global bond market is going to fix us.

This morning you are seeing Greece’s stock market test its lows from June 2010 when the European Fiats made a conflicted and compromised promise to the world that Piling more short-term Debt-Upon-Debt was the elixir of life. Apparently 8 centuries of Reinhart & Rogoff data has once again trumped political storytelling. This time isn’t different.

Why me? Why now? Shouldn’t this be someone else’s problem?

I get that line of thinking, but I also get what wearing a team jersey means - and, as legend USA Hockey Coach Herb Brooks said:

“You're looking for players whose name on the front of the sweater is more important than the one on the back.”

Back to the construct of our intermediate-term global macro forecast…

- Growth Slowing

- Inflation Accelerating

- Interconnected Risk Compounding

We don’t have a choice but to do this now. European and Emerging Bond markets are telling you this and so are American Bond yields:

- European Sovereign Debt Yields continue to make a series of higher-highs as concerns push rightly towards Spain and Italy.

- Emerging Market Debt just had its worst month in 2 years (NOV down -2.9% on the EMBI Index with Brazilian and Russian weakness).

- US Municipal Debt funds just flashed their 2nd consecutive week of outflows, taking the 2-week total to north of $5 BILLION.

Yes, we recognize that a BILLION or a TRILLION dollars isn’t what it was to our grandparents, but these are still big numbers to consider on the margin. Remember, everything in global macro that matters happens on the margin.

US Treasury yields are bullish on both our immediate and intermediate-term durations (TRADE and TREND) again this morning as well (yes, that’s a very bad leading indicator for bond funds in your 401k). Despite The Ber-nank’s JapanEuro style political promises, Mr. Global Macro Market is saying hey, dude, remember The Lehman Brother?

If you or your parents are baby boomers, you know what a double digit mortgage rate means to your family’s discretionary income. God knows you don’t need a Johnny Come Lately Wall Street “economist” to warn you about that. Maybe it’s time to dig into those Old Austerity boxes of our forefathers this Christmas to remind ourselves that as good as it gets may be gone if we don’t stop ourselves from just want.

My immediate term support and resistance levels for the SP500 are now 1173 and 1197, respectively. I’ve maintained my ZERO percent asset allocation to US Equities. I’m still long the US Dollar (UUP) and short the SP500 (SPY) in the Hedgeye Portfolio.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer