Lower airline capacity and higher airfare could slow recovery

As we mentioned in our note last week, “A SOLID OCTOBER ON THE STRIP,” McCarran visitation increased 2% YoY in October, the first increase since November 2009. We wonder if this growth can be sustained, given what’s happening with air capacity and airfare.

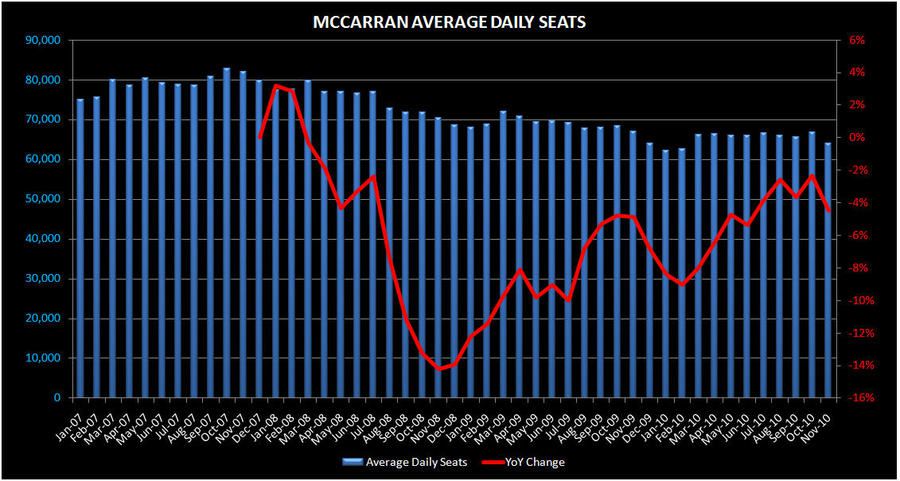

The number of average daily seats at McCarran has fallen every month on a year-over-year comparison since Feb 2008. Based on the released schedules, November is no exception, falling 4.5% YoY and 4.2% MoM, as Southwest Airlines, the busiest carrier at McCarran, had announced it was cutting 12 McCarran round-trip flights starting Nov 7. This capacity shrinkage is not universal as North American air carriers, on a nationwide basis, increased capacity by 3% in November, according to aviation intelligence OAG. Year-to-date, McCarran capacity is down 5.4%. Furthermore, airlines are focusing more on business travel routes which yield higher than leisure markets such as Las Vegas.

What about for 2011? Hard to say. MGM’s CEO Jim Murren is confident McCarran capacity will be higher in 2011. The Air Transport Association and Randall Walker, Director of Clark County Aviation Department, believe capacity will have a small gain next year but nowhere close to 2007 levels. Some of the smaller international carriers are also predicting greater number of seats. But the domestic carriers, which account for 95% of the capacity, are cautious. Southwest will only add one Vegas daily round-trip flight a day when winter seasonal changes are completed in February 2011. Jet Blue’s CEO, David Barger, said he is reluctant to add Vegas flights and Andrew Levy, president of Allegiant Travel Co., the parent of Allegiant Air, said he doesn’t see higher number of planes at McCarran because of the focus on profit margins. In addition, US Airways is unlikely to return to McCarran after its massive withdrawal in late 2009 and the proposed Continental and United merger may further cut capacity.

Meanwhile, lower capacity is contributing to higher airfare. The average lowest LV airfare has remained stubbornly higher in 2010, compared with a year ago - higher lows if you will, which could mean lower highs for Vegas stocks. The Bureau of Transportation Statistics data show that, as of June 30, 2010, Las Vegas airfares had risen quicker than the national average. Using Expedia’s TrendTracker and FareCompare’s Airfare Tracker, we believe higher Vegas airfares continued in Q3 and will continue into year-end.

Unless the airlines reverse their tactic of higher prices/lower capacity, Vegas could see limitied visitation growh and less discretionary spending - potential impediments to any Vegas recovery.