With the majority of family footwear retailers reporting this morning a few things are clear, boots are working - again, traffic’s improving, and comps are rivaling what we saw in the athletic channel last week. With PSS the last to report coming out next week, the read-through is unquestionably positive. Comp trajectories suggest our prior estimate of -8% comp in Q3 is simply too low at PSS. Here are our key callouts both at the channel level as well as by retailer from this morning’s calls:

Family Channel Callouts:

- Consistent with what we saw in the athletic channel, EPS beats across the board with upward revisions to guidance.

- Inventory build ahead of sales growth at all 3 companies in the channel, which better positions each to capture Q4 sales

strength compared to chase mode several were in last year. Also embedded in inventory growth is higher toning related

inventory that accounts for more than 50% of inventory growth at some retailers (i.e. BWS & SCVL).

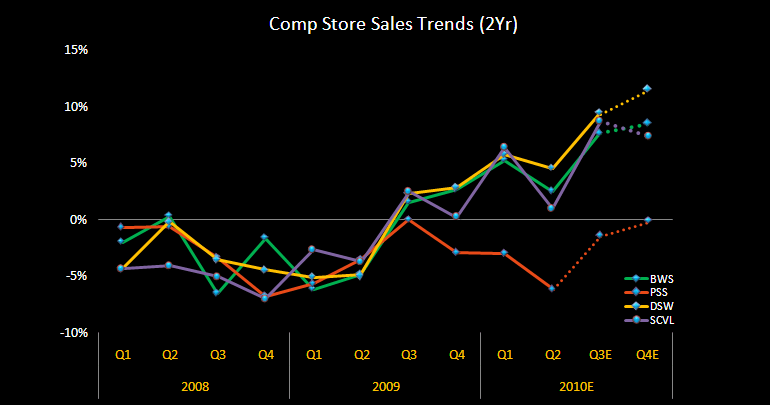

- Comps slowing more modestly on 1yr basis in 2H reflecting a substantial acceleration in the 2yr

- Early reads for Q4 reflect accelerating trends even from Q3 levels

- Traffic improving (up 6% at DSW; +2.5% at SCVL, and up LSD as BWS)

- Boot comps up +10% on a +47% last year at DSW, 40%+ at SCVL confirms trend remains robust

- Better than expected BTS sales across the board appears to have legs into Q4

- Promotional environment has and continues to remain more benign compared to last year

DSW: EPS of $0.79 vs. $0.75E ($0.60 last year)

Sales +10%

Inv +15%

- Better than expected sales through first 3-weeks of Q4

- Outlook:

- Raised EPS to $2.30-$2.40 (was $2.20-$2.30)

- Add’l gross margin compression expected in Q4 against significantly more difficult comps (+850bps)

- SG&A leverage largely due to lower bonus expense compared to last year

- Inventory per sq. ft. up 13% vs. down 11% last year so up modestly on 2yr basis

- 2yr comp (9%+ in Q3) accelerating even higher so far in November

- Traffic up 6% in stores (.com up 22%)

- By category: +10% in women’s; +6% men’s; +9% athletic; +19% in accessories

- Boots posted a +10% comp on a +47% last year

- DSW Rewards a factor in driving sales growth with 87% of sales YTD part of program – 4mm accounts added this year

- Now have nearly 20% of stock on replenishment system helping to increase conversion rates by 4% at the store level

- Nike assortment expanded to include men’s running in Q3 as company broadens into more athletic

- Toning still accounts for ~2% of total sales; unit sales consistent with 1H reflecting lower ASPs

- Bigger focus looking forward is lightweight footwear

- Store growth:

- plan to open 20 new stores next year

- 3 in smaller markets that co. has previously avoided, if successful equates to additional 50+ market opportunity

- Seeing ‘a lot of deals’ coming up for attractive real estate opportunities – positive chg on the margin

BWS: EPS $0.45 vs. $0.30E ($0.42 last year)

Sales +14.5%

Inv +20%

- Better than expected BTS sales driven by athletics, dress, and casual styles

- Less promotional activity than last year (19 fewer BOGO days)

- Stronger initial margins in mid-tier and mass channel

- Most significant growth at wholesale up +34% in a decade

- E-commerce up +14%

- Comp up +10.6% on +4.7% last year at Famous Footwear

- Traffic up LSD and AUR with double-digit increases in conversion

- Increases across all categories and regions

- Women’s up HSD; Men’s up MSD; Kids & Acc’s up LDD

- Toning accounted for +4.5% of comp (most over-indexed of family channel peers)

- Boot and dress shoe demand drove sales at Via Spiga and Vera Wang up over 50%+

- Sales/ sq. ft. up to $184 vs. $164 last year edging closer to goal of $200+

- Toning accounts for ~3/4 of inventory growth in Q3 with core inventory up only +5.6% excl. toning

- 30% of customers purchasing toning product new to FF; 1/3 of which have bought other product

- Toning category expected to represent 6%-7% of volume in Q4.

- Comps Q4-to-date trending up HSD

- Wholesale backlog up +25% reflecting positive forward demand

- Strong top-line key to offsetting $17mm after tax cost ($0.25 in EPS) related to higher incentive comp and marketing

- Net store closings continue with 14 locations vs. opening 4 in the quarter

- Outlook:

- FY10 EPS to $1.00-$1.05 vs. $0.90E

- Initial outlook for FY11 - Famous Footwear same-store sales growth in the low to mid single-digit range;

GCO: EPS $0.77 vs. $0.59E ($0.49 last year)

Sales +19%

Inv +25%

- Comp up 9% on -2% last year

- Up +11% through first 3-weeks of November

- By seg: Lids +13%; Journeys +9%; Johnston & Murphy +7%; Underground Station +3%

- Johnston & Murphy one of strongest qtrs in years driven by casual business and higher full-price selling

- Slow start to boot sales in October – accelerating in November

- Mix shift towards casual away from dress continues

SCVL: EPS $0.70 vs. $0.66E ($0.59 last year)

Sales +6.7%

Inv +12%

- Sales trends by category and region all positive during the quarter

- Comp up +7.2% on +10.2% last year

- Both traffic (+2.5%) and conversion rates increased

- Would have still been up MSD excl. toning

- Women’s non-athletic up MSD driven by strong sandals selling at higher rates, men’s up MSD as well

- Adult athletic up HSD driven by running up 20%+

- Boots up double-digit in first 2-months of Q3, trended down in October, back up 40%+ in first 2-weeks of Nov.

- Toning $$s down in Q3 though pairs remained flat sequentially

- More than half of inventory build due to toning (up only MSD ex toning), aged levels at all-time lows

- Still expect to ramp store openings in FY11 to 20 stores from 10 this year – mostly in existing markets

- Outlook:

- Q4 EPS of $0.30-$0.32 vs. $0.25E

- Comps +4%-6%

- Expect strength in boots to increase throughout the holiday season (Nov & Dec strongest months)

- Also expecting continued strength in athletic and toning categories

Casey Flavin

Director