Conclusion: No change to our view that the pillars supporting the US economy are weakening.

Here are some key factors to consider in the outlook for U.S. GDP growth:

- The boost to growth from the fiscal stimulus is fading.

- State and local governments will be a significant drag as they cut spending and employment.

- The boost from the inventory cycle will also weaken.

- While exports continue to rise, imports are also increasing and the trade deficit is widening.

- Global growth is slowing and the sovereign debt crisis will exacerbate this weakness.

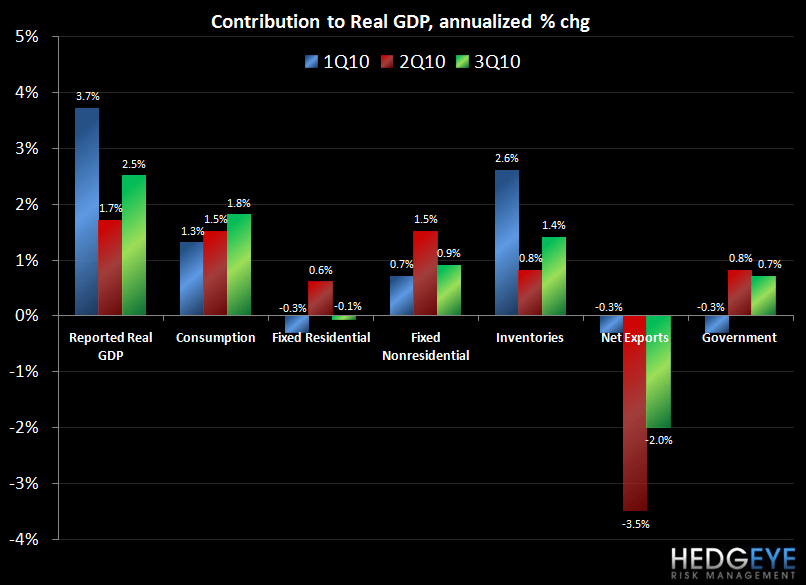

Today, the Bureau of Economic Analysis announced that the U.S. economy grew at a rate of 2.5% in the third quarter, 0.5% more than previously calculated. The upward revision in U.S. GDP for the third quarter was due to upward revisions to consumer spending, exports, and state and local government spending. Our view is that the trends in consumer spending and state and local spending are not sustainable. One supporting anecdote pertaining to consumer spending is the Redbook news today that retail sales were 0.0% for November month-to-date versus October. That compares to +0.1% month-to-date reported in the week prior.

In 2011, GDP growth will be increasingly dependent on the internal demand drivers: consumer spending and the corporate sector driving investment. While corporate profits have returned to their pre-recession levels, confidence needs to improve. The hoarding of cash by Corporate America underlines their reluctance to hire and invest in long-term fixed assets. The political volatility in Washington, and the lack of predictability that goes with it, has been cited by several major CEO’s as a cause for concern.

The most significant downside risk is the continued weakness in the labor market, which is needed to sustain continued improvement in consumer fundamentals. Under an optimistic scenario, 1-2% GDP growth will prove to be inadequate in an effort to reduce the unemployment rate. Add to this slowing global growth and the European sovereign debt crisis and it seems that we are far from seeing a significant acceleration in GDP. Downside risk for the economy is still alive and well.

Howard Penney

Managing Director