The Macau Metro Monitor, November 22nd, 2010

VISITOR ARRIVALS FOR OCTOBER 2010 DSEC

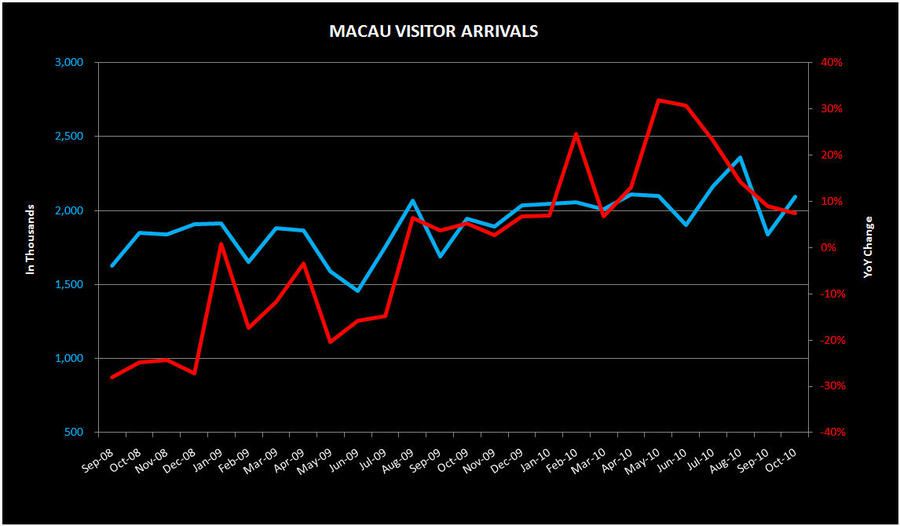

Total visitor arrivals rose by 7.5% YoY to 2,092,343. Visitors from Mainland China increased by 6.7% YoY to 1,124,061 (53.7% of total), with 479,516 traveling to Macau under the Individual Visit Scheme (up 3.9% YoY). Visitors from Hong Kong (629,233), Malaysia (27,454) and Republic of Korea (21,931) grew by 14.0%, 5.9% and 59.8% respectively, while visitor arrivals from Japan (29,637) held stable compared with that of October 2009; however, those from Taiwan (98,674) decreased by 6.8% YoY.

OCT INFLATION HITS 3.5% Strait Times, RTT News

Oct CPI of 3.5% was lower than the market's forecast of 3.7%. Month-on-month, CPI rose 0.5%.

S$96M 'LOST' IN SINGAPORE Asia One

MCA national organizing secretary Tee Siew Kiong believes Malaysians gamble away about RM230 million (S$96 million) a month. His calculation is based on 3,200 people crossing over in buses or cars to gamble in the two S'pore IRs, spending an average of S$1,000 (RM2,400) every day. The casinos have been giving free meal vouchers and free return trip for those who bought a minimum token of RM240 to gamble. Also, transport operators get a RM900 bonus if they bring in a busload of passengers to the casinos.