Conclusion: While the company conference call may shed some light on how management is going to turn things around, right now what JACK is doing is not working.

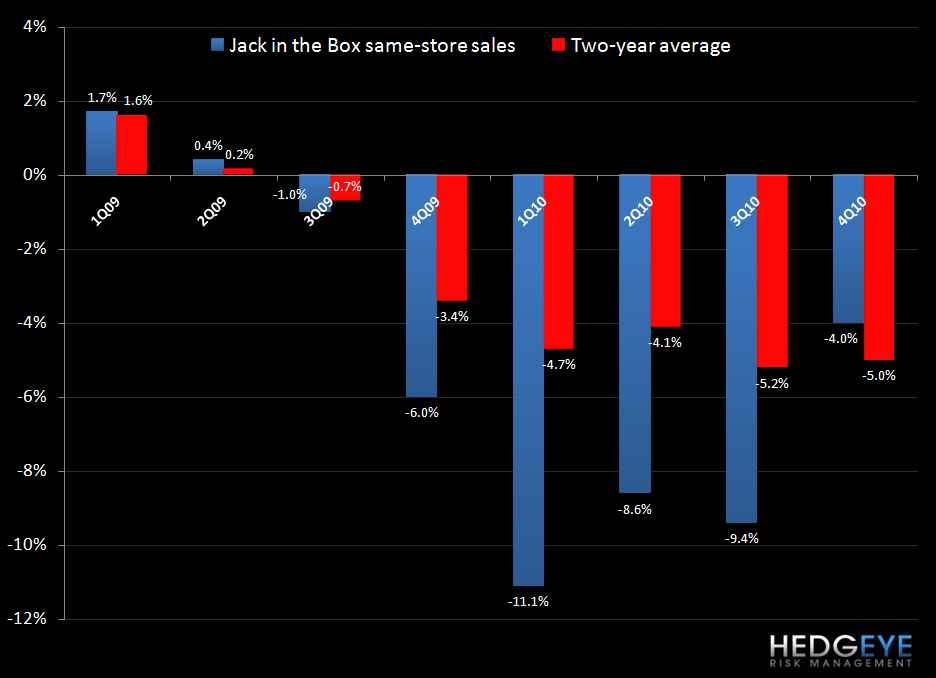

For 4QFY10 Jack in the Box company same-store sales declined 4.0%, with the same excuse of the concept continuing to be impacted by high unemployment in key markets for the key customer demographics.

One a two years basis same-store sales improved only 20bps as the company strategy of quality improvements to signature products are not gaining traction. The strategy for 2011 will include a substantial completion of the restaurant re-imaging program, which will continue to penalize EPS in 2011. The company is currently guiding to same-store sales of -1% to +1% at Jack in the Box company stores for 1QFY11, which implies things get worse on a 2yr basis from 4QFY10.

Yet management hopes that these initiatives will increase the customer appeal of the Jack in the Box brand and provide a catalyst for sales growth when unemployment and consumer spending begin to improve. Additionally, getting the system to look good is getting incrementally more expensive too. Diluted earnings per share guidance of $1.41 to $1.68 (consensus at $2.01) includes approximately $0.10 to $0.12 of incremental re-image incentive payments to franchisees in fiscal 2011 as compared to fiscal 2010.

It’s expensive to hope and pray things get better?

Consolidated restaurant operating margin was 12.5% in 4Q10 versus 15.8% last year - sales deleverage negatively

impacted margins by approximately 110 basis points in the quarter.

- Food and packaging costs were 90 bps higher - overall commodity costs were approximately 3% higher, driven by higher beef, cheese and pork costs which were partially offset by lower costs for poultry, shortening and bakery products.

- Payroll and employee benefits costs were 29.9% vs. 29.6% the same quarter one year prior.

- Occupancy and other costs increased 210 bps primarily to sales deleverage, higher depreciation resulting from the company’s ongoing restaurant re-image program, increased repairs and maintenance, and additional costs relating to guest service initiatives.

I completely understand why the company wants to refranchise the store base down to 20% company owned, but getting from A to B continues to be a struggle. The 4Q10 gains on the sale of company-operated restaurants included the sale of an entire market with lower-than-average sales and cash flows. To get the sales done, the company provided $23.1 million in financing during the quarter for two of the six refranchising transactions, including the entire market sale. Importantly, $18.7 million has been repaid thus far in the first quarter of 2011.

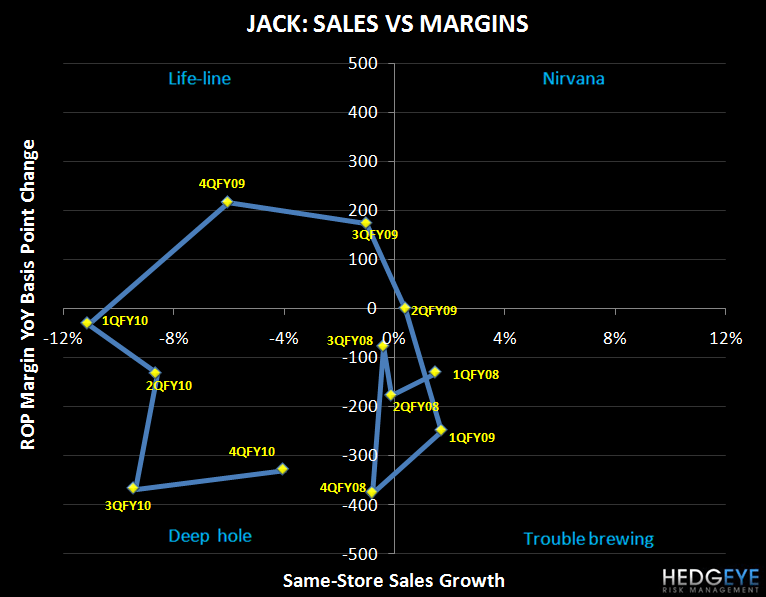

The penalty the company is paying right now to fix the business and get the business model is a big drag on EPS and the confidence level that things will improve is low. To make my point I have included the matrix chart for JACK and for MCD. When there is any expectation that JACK can get to Nirvana, with positive same-store sales and expanding operating margin, the stock will move accordingly.

Howard Penney

Managing Director