Here I am addressing an article written by the respected Jacqueline Doherty of Barron’s this past weekend.

Dear Jackie,

I can appreciate the value in a non-consensus view as much as the next guy, but having read your article in Barron’s titled, “Off to the Mall” this weekend, I have a few points I’d like to make in defense of the consensus view that consumer deleveraging is due to continue for a while. In fact, it will continue for longer than consensus expects. The data presents a gloomy picture but I also believe that recessions such as this take a toll on the mindset of consumers in a way that less severe downturns do not.

The crux of your argument, as I understand it, is that following “two painful years of retrenchment”, there is pent-up demand and data relating to household financial obligations are – currently – better on the margin and this points to “an end to the deleveraging process” and a boost to retail sales and the broader economy in 2011. Respectfully, I disagree. On the contrary, deleveraging has a ways to go.

Firstly, the Consumer Discretionary sector (XLY) is the best-performing sector so far this year and the S&P performance of late seems to suggest that positive news for the consumer is being priced in. Corporate profits are also being well-received by the markets. In spite of the upward trajectory of the stock market and corporate earnings, unemployment is still not improving sufficiently. Corporations, nervous about the economic outlook, are retaining earnings in the form of liquid assets rather than hiring of investing in long-lived assets. The Great Recession had an impact on the psychology of corporations that should not be underestimated.

Likewise, the impact on consumers should also not be underestimated. Job uncertainty and continuing economic weakness is imparting an unprecedented degree of frugality on today’s Americans. The drawdown in credit card balances is one example. Since credit card debt stands for a very small portion of total household debt outstanding, I believe that the 16% decline says more about the shift in mindset of the consumer than any completion of the deleveraging process.

The chart above illustrates an unprecedented change in consumers’ mindset. Furthermore, private sector borrowing as a whole is dragging on the economy. Total private sector borrowing amounted to almost 30% of GDP in 2007 and by2009 it had fallen to less than minus 15% of GDP. That constitutes roughly a 45% of GDP swing in private sector borrowing over a two-year period. This was a traumatic hit, to say the least. I’m not expecting a rebound to the good old levered up days any time soon!

As the Reinhart and Reinhart study you fairly allude to in your article describes, the tectonic shifts in the financial sector, housing market, and subsequent (and ongoing) consumer deleveraging pose drastically difficult obstacles for the economy to surmount. Unlike slowdowns that are associated with monetary policy being tweaked in order to address inflation concerns, downturns triggered by the financial sector tend to take result in longer and more sluggish recoveries.

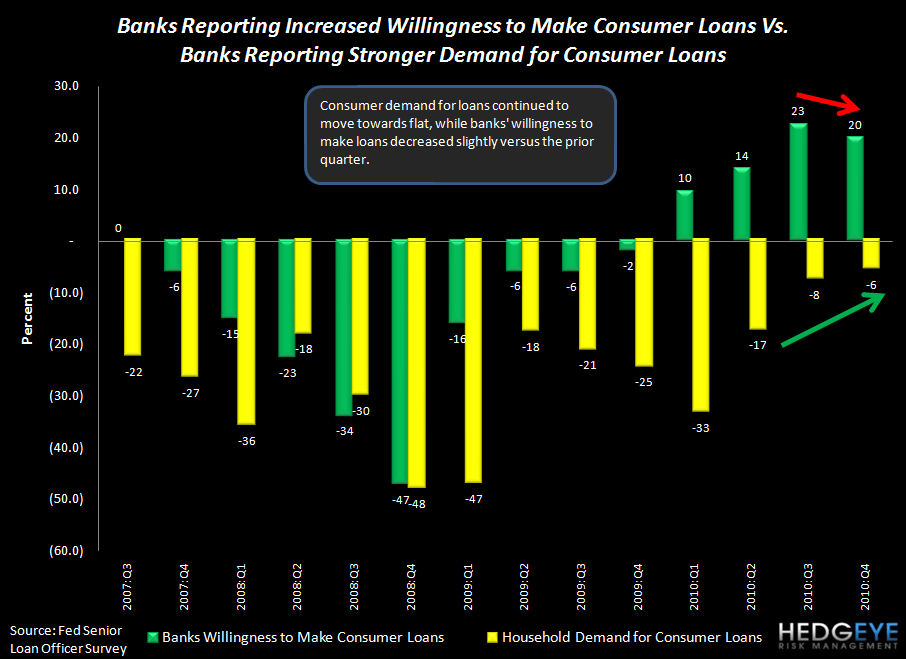

While the rise in equity prices over the last 18 months may help the consumer via higher 401(k) values this holiday season, inflation and the higher interest rates across the globe are causing slower growth on an international basis. The emergency interest rate that the Federal Reserve has held for two years now may be viewed by Diane Swonk, chief economist at Mersirow Financial, as “an unqualified boon to borrowers”, but where are the lenders? As of the most recently reported quarter, banks are tightening lending standards. Most importantly, mortgage rates are heading higher, not lower, and that will certainly not encourage any consumer re-leveraging.

I don’t have access to James Paulsen, chief investment strategist at Wells Capital, work but I would be very interested to see how he gets to 3-4% GDP growth for next year. Here are my main concerns with his bottom line:

- The inventory cycle is going the wrong way in the first part of 2011; moving to net-neutrality towards impact on GDP growth. (I recently posted that inventory accounted for 2.6%, 0.08% and 1.4% for the first three quarters 2010, respectively) As a side note, the sequential improvement in GDP in Q3 was unintentional as some firms were caught out by the slump in demand during the summer and unintentionally built up inventories in Q3 - a trend that will reverse itself in Q4 and the early part of 2011.

- The Recovery Act, despite the controversy, added 2%+ to GDP in 1H10. By design the act was to have all the money “out the door” by the end of September and succeeded in doing so. Going forward, the cost of the Recovery Act will be net neutral and eventually as it ramps down and, eventually – in terms of cash flow – will be net negative to GDP growth.

- The final factor is state and local deficits which are projected to be $100 to $150 billion a year for the next two tears. Going forward, a much smaller share of which will be offset by federal subsidies, therefore a much larger share will need to be closed through tax increases and spending cuts at the state and local level.

Taking points two and three, together that added a net 2% to GDP in 1H10 and will be a negative 2% to growth in 1H11. If you then add the positive inventory cycle in 1H10 of 3.4% and you get the total contribution to GDP growth from the three factors of 5.4% in 1H10. Depending on your view of the inventory cycle, we are looking at a potential year-over-year swing in GDP in 1H11 of around 5.4%, which becomes a headwind in the next 12 to 24 months. At best, we are looking at flat to 1-2% GDP for the next 12-24 months.

What does all this mean for the consumer and the unemployment rate? Under a good scenario, it’s going forward it’s going to be a hard slog of 1-2% GDP growth, which will prove to be inadequate in an effort to reduce the unemployment rate. Your article cited an improving outlook for jobs. Is the outlook really improving enough? If it is improving, I don’t believe that the data supports more than a miniscule improvement. Certainly, a far greater rate of improvement will be necessary to ease concerns about the job market on a wider basis.

Last week the headline initial claims number rose 20k to 457k (23k net of revisions)! Rolling claims came in at 456k, an increase of 2,000 over the previous week. This wiped out last week’s improvement, and claims still remain in the same band they’ve occupied for the year. We're still a solid 50-75,000 above where we would need to be in order to see the unemployment rate fall.

As you noted, one leading indicator of the consumer's health is the default rate on loans; it peaked in the past year in several key loan categories, and has been declining since. The S&P/Experian Consumer Credit Default Indices, a measure of changes in U.S. consumer-credit defaults, fell 3.6% in October.

We at Hedgeye have a much different point of view. We see consumer deleveraging going on for years to come. Here are a few key components of out thesis:

- From 2004 to 2Q08, total household debt rose 31.6%. From 2Q08 through 2Q10, it declined 5.1%. There is likely more to come!

- Looking at the year-over-year change in total household debt is even more lucid an indicator; total household debt is declining and it is declining at an accelerating rate. The decline in 2Q10, of 3.4%, was the steepest of the recession.

- In terms of mortgage debt, despite the decline in home values from the peak (approximately 33%), mortgage debt has only declined 5%. Loan to value ratios are in the 80’s – expect further deleveraging, not releveraging.

- Until LTV’s come into a more historically-normal range, it is unlikely that consumer spending will return to its former glory. Without housing prices appreciating (highly unlikely), our financials team estimates that it would take 10-15 years for the current LTV ratio level to be worked down through amortization. Housing is the key hurdle for stronger consumer spending in the U.S. and forms a key part of the Hedgeye view on this topic.

- Mortgage debt matters for commercial banks; 27% of the $10.6 trillion in household mortgage debt outstanding is held by commercial banks. That’s $2.86 trillion.

- Credit card debt is a small piece of the picture, 6.4% of total household debt. Year over year change in revolving credit has recently ticked up but, at this rate, would take 10 years to stop shrinking.

- The reduction of credit card debt since 2008 (chart earlier in the post) is unprecedented; clear shift in consumer mindset.

The consumer is certainly not dead and there are segments of the consumer space that are tied to wants and not needs (or maybe less unnecessary needs) that may continue to perform well. Starbucks may continue to sell an addictive product well, car sales may perform well also, but considering that housing is the ultimate ball around the ankle of the consumer, there is a long way to go until Americans can once again lever up and splash some cash.

Sincerely,

Howard Penney