This guest commentary was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst. This piece does not necessarily reflect the opinion of Hedgeye.

In this issue of The Institutional Risk Analyst, we ponder the state of the US financial markets in the final weeks of the third quarter of 2021. The economy is slowing, a U.S. debt default again looms, but life continues, albeit stranger each day.

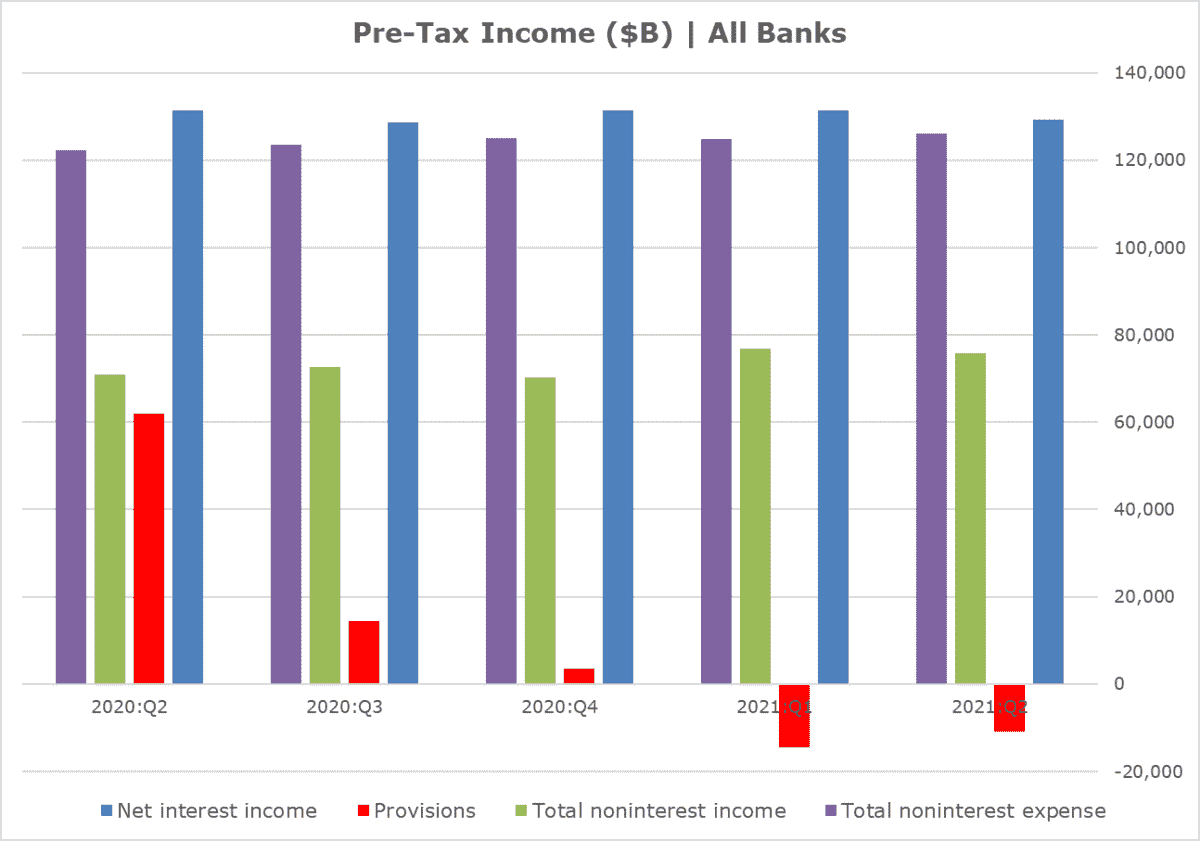

We predicted almost a year ago that bank net-interest margin was headed towards zero. The FDIC now notes in its Quarterly Banking Profile:

“The average net interest margin contracted 31 basis points from a year ago to 2.50 percent—the lowest level on record. The contraction is due to the year-over-year reduction in earning asset yields (down 53 basis points to 2.68 percent) outpacing the decline in average funding costs (down 22 basis points to 0.18 percent). Both ratios declined from first quarter 2021 to record lows.”

Source: FDIC

Now you might think that the state of the US banking system ought to be a key concern of members of the Federal Reserve Board, but you’d be wrong.

Instead, members of the Board, joined by former Fed Chair and now Treasury Secretary Janet Yellen, are planning ways to work-around the American political process and thereby avoid an event of default by the United States. Writing Friday night in the Financial Times, John Dizard notes:

“We had a hint of the risks and what actions the Fed can take from a transcript of a teleconference of the central bank’s policy-setting Federal Open Market Committee on October 16 2013. It was released in January 2019 and is the most recent published account of the emergency “actions” the central bank plans to keep markets open in the event of a shutdown, according to a person familiar with the matter. Yellen and current Fed chair Jay Powell were on the call as board members.”

And this all just happened to surface at the end of last week – at the same time that “extraordinary” measures by the Fed to avoid a Treasury default were gaining attention? Hmmm.

As it turns out, the FOMC actually discussed in 2013 ways to skirt federal law and roll maturing US Treasury debt by one day at a time. This was intended to give the Treasury under President Barrack Obama time to obtain an extension of the debt ceiling from Congress.

Both political parties seem determined to push the credit standing of the United States to the breaking point in pursuit of partisan advantage, thus the Fed is looking for a solution.

Congress allowed the limited authority for the Fed to purchase debt directly from the Treasury lapse in 1981. For history buffs, please see the excellent 2014 treatment by New York Fed economist Kenneth D. Garbade, “Direct Purchases of U.S. Treasury Securities.” The abstract reads:

|

“Until 1935, Federal Reserve Banks from time to time purchased short-term securities directly from the United States Treasury to facilitate Treasury cash management operations. The authority to undertake such purchases provided a robust safety net that ensured Treasury could meet its obligations even in the event of an unforeseen depletion of its cash balances. Congress prohibited direct purchases in 1935, but subsequently provided a limited wartime exemption in 1942. The exemption was renewed from time to time following the conclusion of the war but ultimately was allowed to expire in 1981.” |

Garbade’s timely history lesson published a year after the subject FOMC meeting was a not-so-gentle rebuke to the staff of the Fed Board in Washington.

The Fed’s lawyers apparently advised members of the FOMC a year earlier that they could lawfully accommodate the Treasury’s cash needs. In fact, as Garbade documents, the advice which led to the FOMC discussion in October 2013 was completely wrong.

Not only is it unlawful for the Fed to purchase debt directly from the Treasury, but more important, as Dizard alludes in the FT, the value of Treasury debt as collateral is nil once it gets within one day of maturity.

Rolling the maturing Treasury debt for a day does not help the shortage of risk-free collateral, especially if you are cognizant of the collateral rules of the various exchanges and clearing houses. But it now seems that neither Chair Yellen nor then-governor Jerome Powell were properly informed.

Several of the actions reported in the FOMC minutes seem to be illegal on their face. Action 8 discussed by the FOMC, for example, would remove Treasury securities with delayed or potentially delayed payments by buying them outright for the Fed’s account. Action 9 would exchange customer’s or dealer’s bonds that are on the verge of default with bonds in the Fed’s portfolio that have later interest or principal payments.

Now most casual observers think that the Fed’s dual or actually triple mandate from Congress via the Humphrey Hawkins legislation includes guiding monetary policy so as to achieve full employment, price stability and, lest we forget, stable interest rates.

In fact, the true mandate that motivates the Fed’s actions is illustrated by the 2013 FOMC meeting. That is, to keep the market for US Treasury debt open and functioning, and thereby avoid a U.S. default.

The debt ceiling and tax raising circus now playing out on Capitol Hill adds certain difficulties to the Fed's fine tuning task. Since a large portion of the Fed’s holdings of Treasury securities are in the form of short-term bills, the approaching political confrontation in Congress over the debt ceiling presents technical problems for the money markets.

First, since the FOMC is currently running over $1 trillion in reverse repurchase agreements (RRPs) with money market (MM) funds, a lack of collateral eligible for repo will throw the FOMC’s efforts to manage the vast flow of liquidity released by Congress earlier in the year into disarray.

Notice, in this regard, that the Treasury General Account (TGA) has now fallen from $1.7 trillion to ~ $200 billion, yet the volume of RRPs remains elevated.

Readers of The IRA may recall that the public narrative behind the RRP facility was to soak up the liquidity flowing from the TGA into bank accounts from the COVID recovery legislation.

As the cash flowed out of the TGA, the collateral used to “sterilize” the TGA was released, but you would not know if looking at the short-term markets. Of interest, domestic bank deposits rose about $800 billion since Q4 2020, but much of this flow is due to the Fed's bond purchases under quantitative easing (QE).

Second, a future lack of collateral is already suggested by the guidance from the Treasury regarding the size of the TGA. This trend that will impact the fixed income and equity markets both since demand for risk-free collateral is the key factor behind U.S. interest rates. The entire US economy depends upon a foundation of leverage on risk-free collateral held by banks and investors. If you have less Treasury, government and agency collateral, then you have less leverage for the system and less economic growth.

If the Fed tries to “adjust” by selling collateral to satisfy private demand for Treasury paper and government-insured MBS, then tapering will have well and truly begun – involuntarily.

This is one reason why the Fed securities desk should sell into market strength and be ready to buy when weakness appears. The mechanical and public management of QE is a major impediment to the Fed's ability to manage this dynamic mess of a situation.

Few people inside or outside of the Federal Reserve fully understand the fragility of the current monetary construct. In past years, the Fed was the proverbial dog shaking the market tail.

Today, however, the vast fiscal flows from Treasury unleashed by the Congress have greatly added to the complexity of the Fed’s liquidity management task. The FOMC talks of tapering, but actually making it happen without a market tantrum is another matter.

The prospect of trillions more in new taxes and debt-funded federal spending from Congress, on top of the $1.7 trillion already spent this year, adds even further to the risk of market instability. Remember that back in July when Federal Reserve Board raised the interest rate paid on reserves and RRPs, Chairman Jay Powell called the move a “tweak.”

The July interest rate hike was ignored by the Big Media, but was an inconvenient turn in the happy economic narrative. Powell's "tweak" was a pretty clear attempt to bolster the yield floor under US assets and thereby defend MM funds and banks.

The growing fiscal chaos in Washington makes such efforts problematic, however. Since the Democrats lack a true majority in the Senate, there is no visibility on future fiscal policy out even a few months.

Should the debt ceiling fight result in a disruption in new debt issuance, Treasury yields could fall significantly. This may seem a strange response to an approaching event of default, but the markets still don't believe a default can occur.

If Congress decides to play chicken, the FOMC may find it is no longer able to defend the lower bound as investors rush to buy supposed "risk free" assets.

In the event, look for MM funds, commercial banks and other users of leverage to complain loudly and seek additional subsidies and support from Washington. US banks and funds cannot function in a zero or negative interest rate world, either financially or in terms of internal systems and controls.

As we noted at the top of this comment, the cost of funds for the entire $20 trillion asset US banking industry was less than $10 billion in Q2 2021, a rounding error.

The only trouble is that the return on earning assets for US banks and MM funds is now falling faster than funding costs due to the mounting demand for risk-free collateral, even more than the artificially suppressed cost of funds. Indeed, the Fed needs to raise interest rates soon to avert a serious calamity.

ABOUT CHRISTOPHER WHALEN

Christopher Whalen is the author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington. Currently, he serves as the editor of The Institutional Risk Analyst.