Hedgeye Portfolio: Short Euro via FXE; Long Germany (EWG)

German Bulls

The ZEW survey of German investor confidence came in well above expectations today, however despite the positive print capital markets across Europe are slumped over the fate of Ireland. As an important inflection, ZEW’s 6 month forward-looking economic sentiment gauge rose for the first time in the last seven months to 13.8 in November versus a forecast of -6 and an October reading of -7.2; the current situation gauge rolled higher to 81.5 versus 72.6 in October. See yesterday’s note titled “Ireland’s River Card” for our take on Ireland and the heightening risk trade in Europe.

We continue to like Germany (EWG) from a fundamental standpoint. Germany’s fiscal conservatism continues to be a bullish catalyst and a clear positive divergence over the bloated PIIGS (Sovereign Debt Dichotomy). Export orders, especially from Asia, continue to flash bullish, and a weakening EUR versus the USD should further propel export demand on the margin.

UK’s Inflation Juice

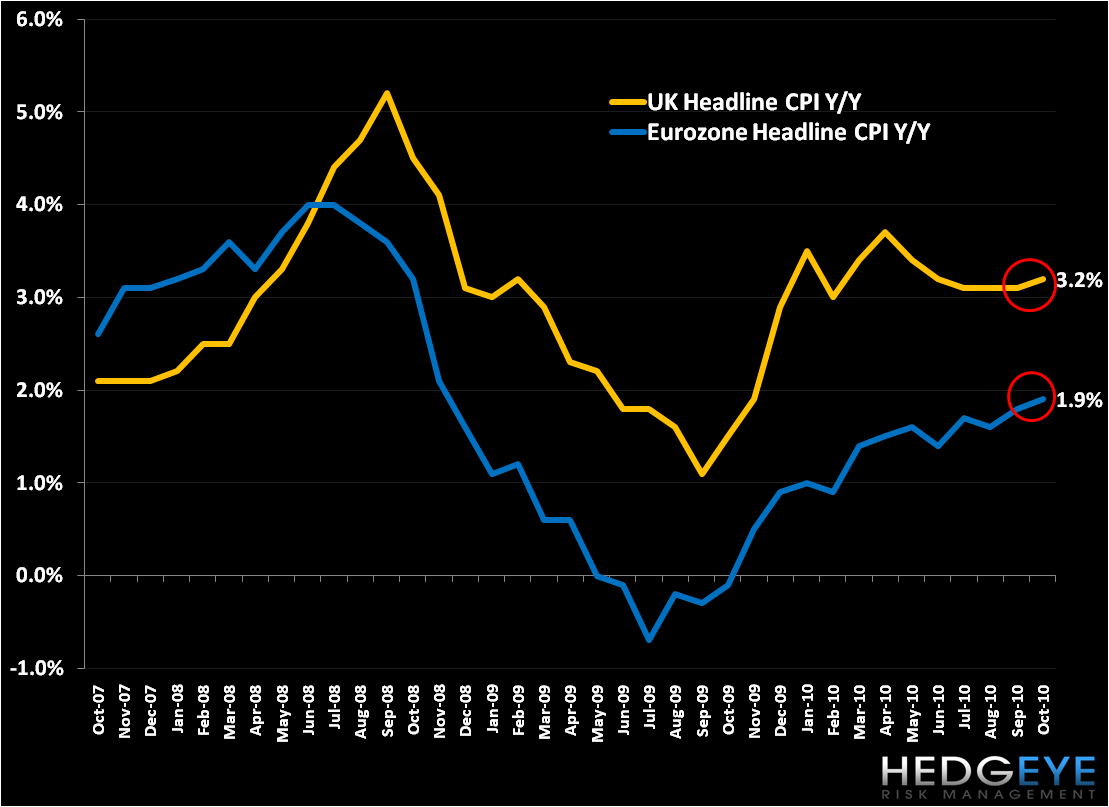

As we’ve highlighted in our UK posts this year, the island nation continues to suffer from inflation above its target rate of 2%. Inflation measured by the CPI rose 10bps to 3.2% in October year-over-year versus October. The chart below shows the divergence between average Eurozone CPI. As CPI continues to trend higher in the UK, and comments from the BoE suggest a rise could be seen well into 2011, the Bank will be challenged (should it be necessary) to issue further quantitative easing for fear of boosting inflation. And should economic growth slow in the UK over the coming quarters, which we’re suggesting due to the country’s austerity programs, the country could be in a real political quarrel on go-forward economic policy.

Das Auto

Finally, as a measure of economic health, European new car registrations (across 25 states) declined 16% in October Y/Y for the 7th straight month. Our take is that as austerity measures squeeze the consumer over the next years, we wouldn’t expect to see domestic car purchases improve materially over the intermediate to longer term. It’s worth noting the difficult compares in the chart below, in particular due to the success of the cash-for-clunkers rebate program in 2009. Bullish prospects remain for European auto manufacturers as order flow continues from the client, China, and greater Asia.

Matthew Hedrick

Analyst