This guest commentary was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst. This piece does not necessarily reflect the opinion of Hedgeye.

As the final days of summer 2021 come into view this week, mortgage executives are left to ponder the world post-Labor Day. A combination of political and regulatory threats is arising just as volumes and profitability in the industry weaken.

And the biggest threat, as usual, is political.

First and foremost, progressive politicians are desperately looking for a problem to solve in the world of 1-4 family residential mortgages, this as the backlog of Cares Act forbearance due to COVID quickly disappears thanks to the Fed. We wrote in an earlier post:

|

"The once daunting pile of loans, millions in fact, that opted for CARES Act forbearance in 2020 are curing at a rapid pace, dashing the hopes of progressive activists for a train wreck in terms of low-income households. Likewise the liquidity trap we saw forming last April for Ginnie Mae issuers was literally averted by the Fed’s cheap money." |

For example, is there racial bias baked into GSE underwriting? A recent syndicated article on racial bias from The Markup, published by ABC News, AP, Market Watch and more, drew a great deal of attention from trade groups, policy makers and housing advocates.

The only problem with the article by Emmanuel Martinez and Lauren Kirchner is that it’s completely wrong.

First, the authors did not even include FHA/VA/USDA loans in their “research” into systematic discrimination. “The Markup has found that lenders in 2019 were more likely to deny home loans to people of color than to white people with similar financial characteristics,” the publication proclaims.

But, wait, aren't GSE loans for rich people with plus +720 FICO scores? FHA is where low-income households access mortgage credit. Double duh.

Naturally, former Federal Housing Administration (FHA) Commissioner, past Mortgage Bankers Association head and all-around good guy, Dave Stephens, took issue with the report. “HMDA data shows outcomes across a variety of variables, including race, but does not show FICO information,” he wrote in a comment. “Obviously to anyone in the business that’s a big deal given that FICO is a threshold data point that determines eligibility for a mortgage.” Bingo.

While the GSE market tends to look at loans based upon risk factors such as LTV and FICO scores, the government loan market does not.

This is why the whole premise of the article in The Markup claiming bias in GSE lending is so completely off base. But remember, progressives in and outside of the media are on a mission, to find a problem to solve – even if none actually exists.

"From the beginning, we explained to The Markup that its analysis of HMDA data, and its pre-determined conclusions regarding mortgage lending, fail to take into consideration several key components that form the backbone of lending decisions, including a borrower's credit score and credit history,” the MBA said in a rare rebuke of a publication.

"We also informed the authors upfront that by limiting their analysis to only ‘conventional’ loans, they would be painting an incomplete picture of the lending environment by purposely excluding mortgages guaranteed by government agencies like the FHA that are designed to help borrowers with lower credit scores and small down payments.”

The reason that people of color are frequently denied conventional home loans has to do with the income levels and FICO scores of the applicants, not some deliberate conspiracy by lenders.

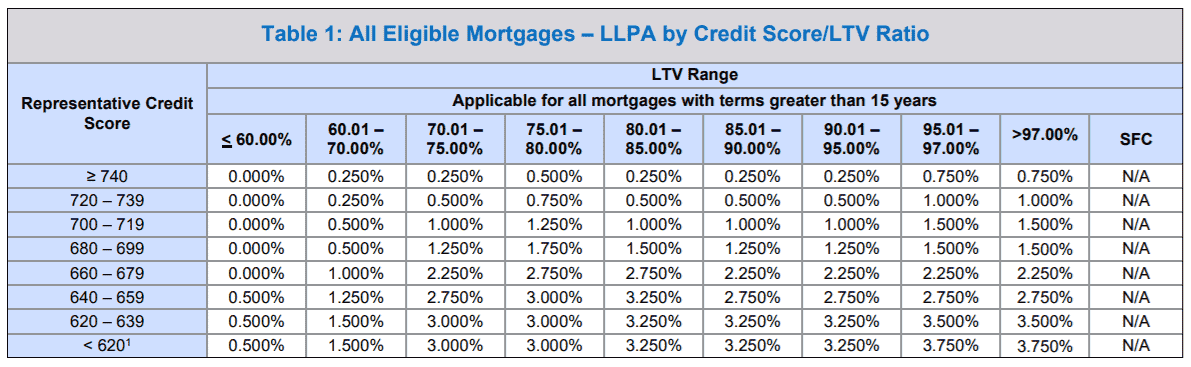

When conventional loans to lower income, lower FICO score borrowers come up for sale into the secondary market, the execution suffers because of these attributes. For example, a borrower with a 620 FICO score and an 80 LTV loan would be hit with a 3% discount from Fannie Mae when the loan is purchased. But since progressives have no idea about mortgage lending, credit or markets, don’t even try to explain this little nuance to them.

Source: Fannie Mae

The embedded discrimination in lending by Fannie Mae and Freddie Mac comes in large measure from the loan level price adjustments (LLPAs) imposed by the Treasury under President Barack Obama after 2008.

These additional fees were initially imposed by the Treasury to prevent GSE loans from prepaying, a hideous move that was meant to preserve the earnings of the GSEs by denying all conventional borrowers the right to refinance. Again, this policy came under Barack Obama.

Successive directors of the Federal Housing Finance Agency have refused to remove these unnecessary fees, which can add points to the cost of a loan for a low-income household depending upon the loan-to-value (LTV) ratio of the loan and the FICO score of the borrower.

But, again, don’t try to talk to a progressive about the secondary market execution for conventional loans to low-income borrowers. They have no idea and, frankly, the progressives don’t care about the details either. They are in search of the next cause.

Today, LLPAs are perhaps the single biggest obstacle to a person of color seeking a loan from the GSEs, but you’ll never hear anybody in Washington and especially within the Biden Administration talk about them.

Remember, the borrower is already paying the GSEs for mortgage insurance on the loan, so the additional fees imposed by LLPAs represent a terrible regressive tax that is weighted against low-income households and people of color. Got it?

LLPAs add to the overall cost of the loan, making it more difficult to sell the asset given the inferior credit profile of the low-income borrower. Remember too that the consumer credit agencies and bond rating agencies all contribute to this problem because, again, of the lower income and FICO scores of the borrower. Adam Rust of the Community Reinvestment Association of North Carolina wrote:

|

“Loan Level Pricing Adjustments” (“LLPA”) change both the cost and the accessibility of mortgage loans for consumers. Although relatively unknown, it is contributing to the ongoing weakness in housing prices. It makes it harder for American families to buy and sell homes. Since it moves many loans to FHA, it does little to relieve the risks associated with mortgage lending that is placed upon American taxpayers. The LLPA creates another hurdle for underserved borrowers." |

Since historically people of color tend to have lower incomes and also higher default rates, the bond market discriminates against these borrowers without even knowing their racial profile.

The bond rating agencies use published methodologies that enshrine 1) FICO scores and 2) LTV ratios in the assessment of the pricing of a pool of loans. While the guarantee provided by the GSEs makes all of these assets seem homogeneous from the perspective of the investor, the pricing of these assets at the point of sale is still affected by the borrower’s credit attributes.

Of note, all of the links to relevant pages of the Fannie Mae Selling Guide to the change in LLPAs from 2011 have disappeared from the web.

In the government market, on the other hand, all loans are priced without a risk adjustment because of the direct federal guarantee.

Historically, the FHA has priced all loans in the same way and has essentially allowed the stronger borrowers to subsidize the weak. But, of course, the folks at The Markup have no idea about any of these little details.

The BIG story on alleged discrimination in GSE lending is whether Sandra Thompson, acting FHFA director, will walk-the-walk on improving access to credit for low-income borrowers and roll-back the LLPAs for the GSEs to pre-2008 levels. Thompson talks a good game when it comes to access and inclusion, but will she act now to remove these hideous LLPAs, which are a levy on the poorest Americans?

Here’s a little hint for progressives: The continued use of the Obama-era LLPAs is a direct assault on people of color who want to purchase a home.

But removing the LLPAs will likely push both GSEs into the red given the footprint reductions already put in place by former Director Mark Calabria. As with everything else in life, there is no free lunch when it comes to lending to high-risk, low-income borrowers.

ABOUT CHRISTOPHER WHALEN

Christopher Whalen is the author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington. Currently, he serves as the editor of The Institutional Risk Analyst.