Conclusion: Consistent with the Malcolm Knapp data we posted on earlier today, retail sales posted better that expected results. However, it will be interesting to see if consumer confidence in November will support this trend.

Some thought from today’s retail data:

- Retail sales posted a fourth consecutive month of top-line growth, although core sales, excluding auto dealers and gasoline stations, have decelerated for the past two months.

- The headline number was driven by strong auto sales; the 5% growth rate contributed more than two-thirds of the growth in top-line retail sales during the.

- Building supply stores, sporting goods and hobby sales posted growth of 1.9% and 1.0%, respectively. Declines were seen in furniture stores, electronics and appliance stores, and department stores.

There are several important factors that are supporting spending in October:

- The S&P is down only one month in the past four, which has helped spending

- The headline job growth is a plus, but still remains sluggish

- Income has continued to rise slowly, despite less government support

On November 1st, I wrote a post titled, “Q4 THEME UPDATE – CONSUMPTION CANNONBALL” that outlined underlying trends pertaining to our thesis. As I pointed out, transfer income is fading and taxes are on the rise. This is clearly a negative for the consumer. Below are the five bullet points from my 11/1 post:

- Both personal income and spending weakened in September. Personal income fell 0.1%: the first decline since last September.

- The decline in income was driven by a $25.5 billion reduction in emergency unemployment insurance benefits. Emergency benefits had boosted transfer income by $20.5 billion in August.

- Interest income (due to the Federal Reserve emergency interest rates fell 0.9% for the third straight month.

- Tax payments are up, driving disposable income down 0.2%.

- Real spending was up 0.1% driven by consumers diving into the savings rates which fell to 5.3% - matching its lowest level in over a year.

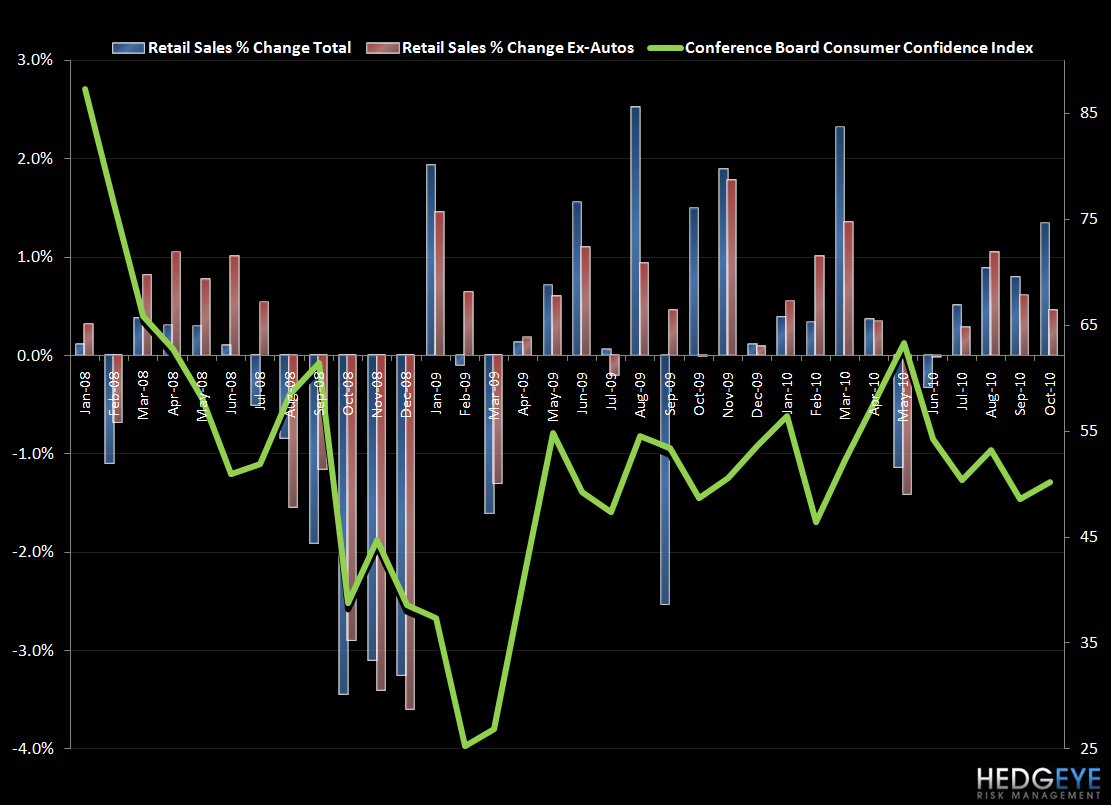

A sixth bullet point I would add to the list is illustrated in the chart below. Despite the recent gains in Retail Sales growth, the consumer is not (as yet) getting behind it in terms of confidence. The next release of this index, on November 30th, will be interesting to see. The chart below suggests that this rally is unlikely to sustain itself long without a similar pickup in consumer confidence, especially with government subsidies waning and taxes increasing. While recent jobless claims data was positive, with the rolling four-week average declining to 446k, the economy is still shedding too many jobs for any material improvement in the unemployment rate to be seen.

Howard Penney

Managing Director