Hedgeye Portfolio: short Euro via FXE, short Italy (EWI)

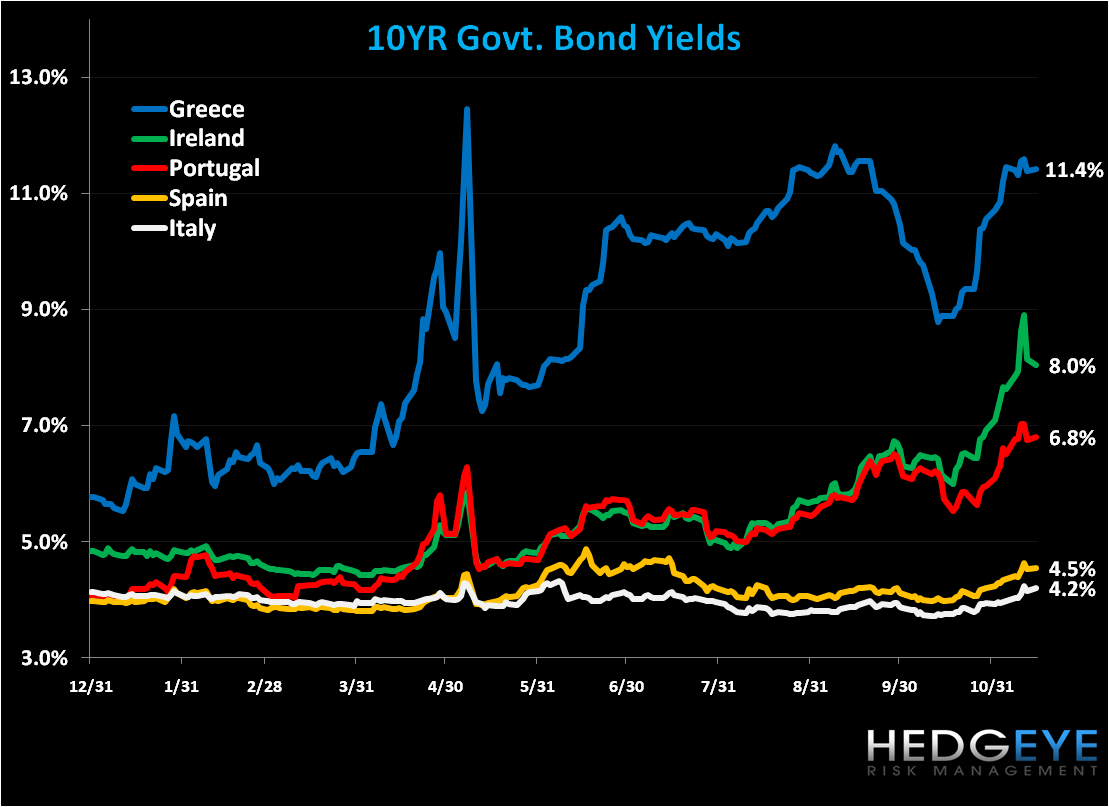

Below we highlight a familiar chart of 10YR government bond yields from the PIIGS (Portugal, Ireland, Italy, Greece, Spain). Of note is the turn in Irish yields, a reflection of short covering and investor anticipation that Ireland will fall the way of Greece and receive a bailout. Beginning tomorrow, European official will meet in Brussels to discuss Ireland’s sovereign funding situation. With an explosive deficit/GDP of 32% in 2010 (a significant share of which represent bank liabilities), the market is demanding a “fix” to the country’s outstanding fiscal imbalances. While Ireland is pushing back on a bailout, claiming that a ~€20 Billion cash pile can cover its debt obligations into mid-2011, the market over the last three weeks is signaling that’s not enough, and that Ireland too must dip into the region’s Financial Stability Fund. Germany is particularly supportive of such a decision. This week we shall also hear from Allied Irish on its revised funding situation, which could further weigh on a bailout decision.

We’ll have our eyes affixed on European meetings this week and next. Remember that European officials have seen this film before vis-à-vis Greece. Six months ago that fire, along with the severe depreciation in the Euro versus major currencies, was quickly quelled with a €110 Billion bailout. This time around we’re seeing the Euro weaken, down -4.3% versus the USD since 11/4 (we’re short the Euro via the etf FXE in the Hedgeye Portfolio)...the river card on Bailout Band-Aid Part Deux may not be far afield.

Matthew Hedrick

Analyst