Management strikes out in attempting to pitch a 14x multiple deal at an 8-10x valuation.

A bird in the hand is worth two in the bush, or so the medieval phrase goes. Unfortunately, Caesars’ management wants you to buy $3.32 billion worth of EBITDA in the bush versus the $1.77 billion of actual EBITDA in the hand. With significant negative free cash flow and 11.5x leveraged, where do I sign up? We call ball four on this deal so the prudent thing would be to take a walk.

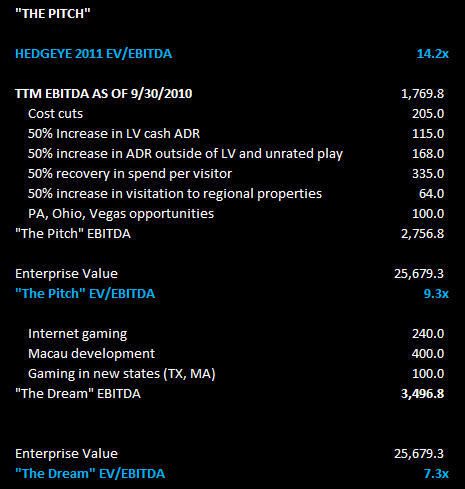

At the midpoint of the $15-17 offering range, the valuation looks to be around 14x 2011 EV/EBITDA. We use the face value of the debt rather than book value which is over a $3 billion difference and a 1.8x EBITDA turn.

This must be a Macau stock, right? We think there should be close to zero value ascribed to Macau. What about other development opportunities and hidden assets? Even if they could find the money, Japan would be a long shot for them, and Texas, PA, and Ohio would cannibalize existing CZR properties. Finally, while we do think World Series of Poker has brand equity, internet gaming in the US just took a major step backward with the Republicans taking over the House.

While we do agree that current EBITDA levels are close to trough, there is a lot of Kool-Aid to drink for one to believe in $1 billion in incremental recovery EBITDA. Here is the Kool-Aid recovery scenario: