"Behind us lay the whole of America and everything Dean and I had previously known about life, and life on the road. We had finally found the magic land at the end of the road and we never dreamed the extent of the magic."

-Jack Kerouac, On the Road

Jean-Louis Kerouac, or Jack as he was more popularly known, was the leader of the beat generation and is one of the most well known American novelists of the last half decade. I recently took a break from my weekend readings of the Economist, Barron’s, Grant Interest Rate Observer, and other similar publications that make my girlfriend go to sleep, to reread Kerouac’s classic, On the Road.

I think it is fair to say that most type “A” investor types operate in stark contrast to the beat generation, and in particular to the writing style of Mr. Kerouac. In 1950, Kerouac outlined The Essentials of Spontaneous Prose, which was an overview of his style of writing - a style which emphasized the unplanned spewing forth of ideas, emotions, experiences and so forth.

Our CEO Keith McCullough wrote his own book, which came out earlier this year, titled, Diary of a Hedge Fund Manager. Far from being the spontaneous prose of a beat, the book is a well thought-out overview of the last decade of Keith’s journey in the world of Hedge Funds. As one reviewer wrote:

“In telling his story, McCullough may end up inspiring a whole new generation of Wall Street achievers and innovators. He may also succeed in tipping a few sacred cows and instilling new paradigms for investing before all is said and done.”

Admittedly, I may be a little biased as I appear in the book via my nickname Jonesy a few times, but I would recommend you consider it as a stocking stuffer in the upcoming holiday season for that emerging fund manager in your family. ( http://www.amazon.com/Diary-Hedge-Fund-Manager-Bottom/dp/0470529725 )

Coincident to reading Kerouac’s book, I was literally on the road this week. I flew out to Colorado Springs to participate in a bi-annual forum with a subscriber of ours, Huntley Thatcher Ellsworth Advisors (http://www.hteadvisers.com/). Aside from being very innovative in the ETF field, twice a year the folks at HTE get up in front of their clients, put on the accountability pants, and talk about what they got right, what they got wrong, and what’s next. At the forum, I gave a presentation titled, “Should U.S. Debt Be Rated Junk Status?” and then participated in Q&A. An interesting question that came up a number of times from the audience was: should we own gold?

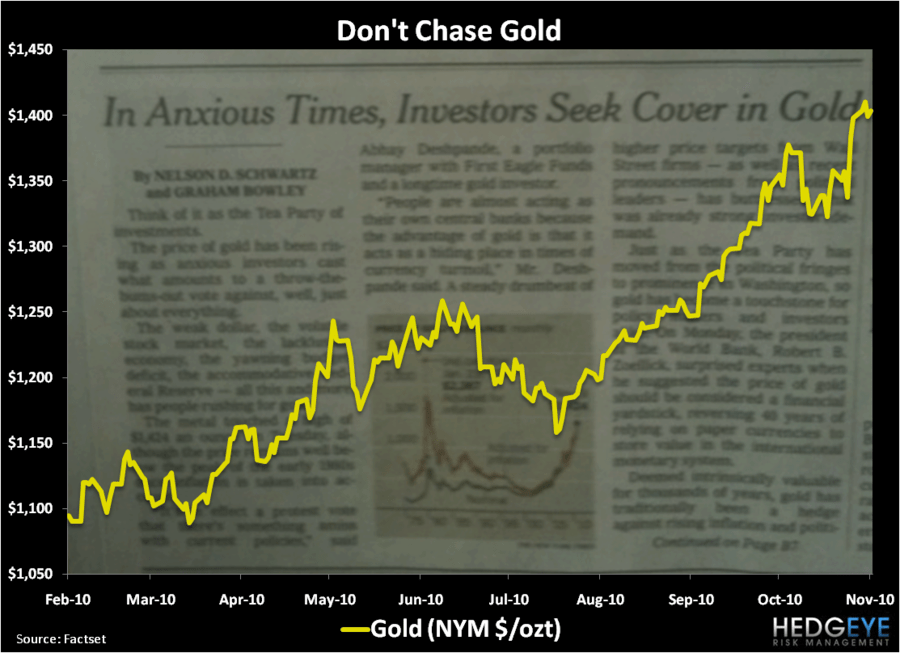

As we think about gold, it is pretty simple. If the dollar continues to get debased, gold will go higher. So longer term, it is likely an asset you want to own if you believe the dollar is going lower. That fact is, if there weren’t monetary value in gold stock, the U.S. Federal Reserve wouldn’t be sitting on over 8,000 tonnes of gold and not selling it. In the short term, we aren’t long gold and have highlighted a key reason in the chart of the day below, which shows the dramatic increase in the price of gold over the past few months juxtaposed against a recent front page New York Times article, “In Anxious Times, Investors Seek Cover in Gold.” If newspaper and magazine covers aren’t the best contrarian indicators, they are close.

Another topic we discussed was the implications of Quantitative Easing, the monetary policy more popularly known at Hedgeye as Quantitative Guessing. Our view is that QE will lead to inflation, without the commensurate pickup in economic activity. While we can debate whether we are seeing inflation in the U.S., globally we are seeing it. In fact, yesterday Chinese CPI accelerated dramatically. As Darius Dale wrote to our subscribers yesterday:

“Chinese October inflation numbers came in white hot this morning. CPI accelerated to a 25-month high of 4.4% Y/Y and PPI also quickened substantially to 5% Y/Y.”

Chinese inflation will lead to one thing, Chinese tightening. If you don’t think that has global growth implications, then you haven’t turned on your Bloomberg terminal yet this morning. In the anticipation of tightening, Chinese equities are down more than 5% and the commodity complex is getting taken behind the barn and shot. Copper is down 2%. Silver is down 2%. Cotton is down 3.6%. Sugar is down 3.4%. It seems we may not have to guess as to the implications of Quantitative Guessing much longer.

My last road trip to Colorado Springs was about 15-years ago when Keith and I were members of the Yale Hockey team. (Keith was a little quicker and I had a little more hair back then.) We were playing Air Force in a two game series. As I recall, Keith was suspended for the weekend and we were swept by Air Force. (Keith would likely suggest there was something to that correlation.) Ironically, the Yale hockey team is back in Colorado Springs this weekend taking on Air Force and Colorado College. Much has changed in the last 15-years, including the fact that Yale is now ranked 3rd in the country. Let’s hope the Bulldogs find the “magic land at the end of the road” this weekend.

Keep your head up and stick on the ice,

Daryl G. Jones

Managing Director