|

Editor's Note: Below is Hedgeye Communications analyst Andrew Freedman's post-earnings analysis on his short Netflix (NFLX) research. Freedman highlighted his short NFLX bias on 7/14/21 during his "2H21 Communications Themes Call." Following a disappointing earnings call on July 20, NFLX fell roughly -5%. Below is updated analysis following the earnings call, as well as key takeaways on why Freedman is short the stock (and potential catalysts for him going long in the future). For more info on Communications Pro research click HERE. |

FROM FREEDMAN

On the subscriber front, Netflix added 1.54M subs in 2Q21 (slightly ahead of management’s guidance of 1M, and just above consensus of 1.2M – note the consensus estimate was revised downward from 1.6M in days leading up to the print).

Most notable was UCAN, where Netflix lost 433k subscribers, largely offsetting the Q1 gain of 448k. Say what you will about competition, but we believe it is having an impact on the margin.

From the survey chart above, you can see that “price” has become increasingly a reason why people cancel Netflix in the U.S.

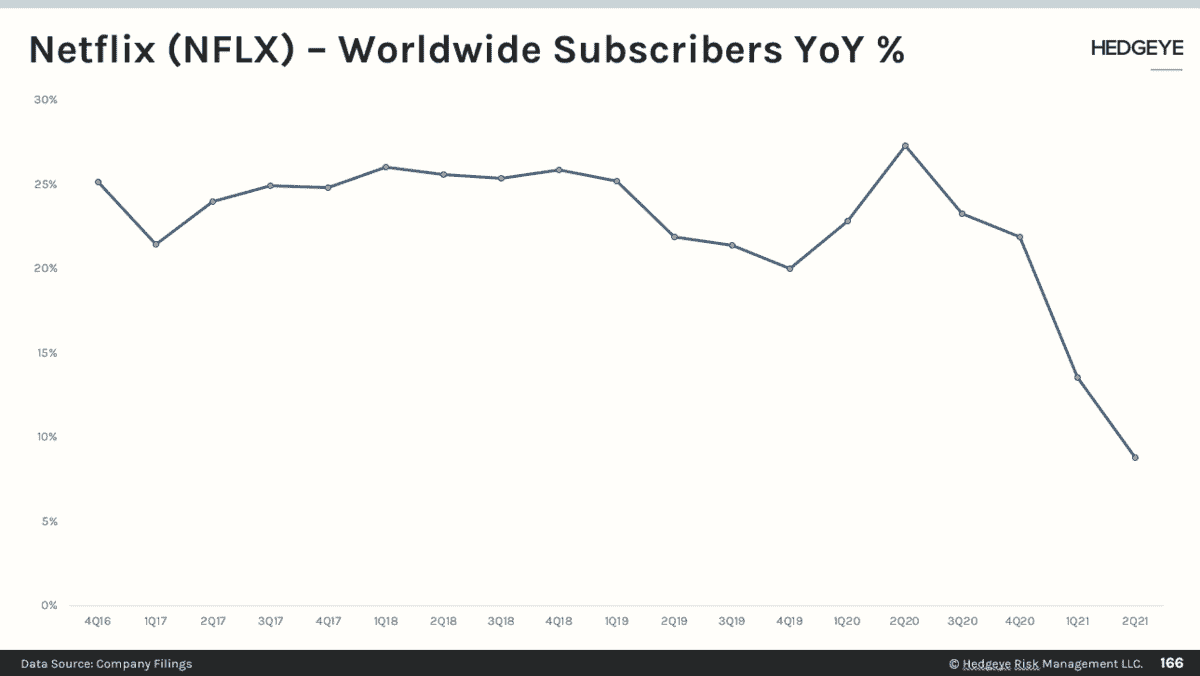

In total, APAC represented 66% of sub adds this quarter, which we believe are coming in at a lower ARPU (or should I say… ARM?) contribution due to mobile-only. Overall, subscriber growth slowed to 9% YoY (2016 – 2020 the average has been ~22.5%).

In terms of our model and what we previewed during our Q3 Communications Themes call last week, we were expecting 1.4M sub adds this quarter and 4.2M on the guide – so downside risk on the guide relative to ~6M consensus Q3 estimate given where the data was trending QTD.

They guided to 3.5M net additions AND a further rev growth decel to 16% in 3Q21 from 19% this quarter (another U.S. price increase coming?). Meanwhile, FCF went back to negative this quarter! (we have long argued you can have FCF or sub growth but not both).

We continue to believe that Netflix’s growth algorithm is challenged.

… and on the net add guidance of 3.5M for Q3, I thought it was weak relative to the 2.2M 3Q20 last year and with content slate ramping back up with “Money Heist” being released late September.

Overall, it doesn’t inspire a ton of confidence that we are getting back to 2019 level of sub growth of 25M a year by 2022 (I’d like to see estimates come down closer to 20M). If the guide ends up being conservative, I am confident we will see it in the data.

From our seat, the quarter played out largely as expected. We have been less bearish on the stock because of the prospect for a rate of change improvement in sub adds given the better content slate, but not ready to make the pivot to the long side since we thought estimates needed to come down.

And while estimates certainly will come down after last night, it is still to be determined whether we get a large enough 2H improvement to keep the TAM/Growth narrative in tact (we still think adoption rates are much higher than bull case implies) and preserve out-year estimates.

If tentpole series like “Money Heist” and “The Witcher” (historically major drivers of new sign ups) don’t move the needle (we will see it in the data), then that will be a big problem and we are setting up for a great short opportunity later in the year (capitulation event).

However, for now, it appears the sell side is going to continue to defend the name (yay video games! #shinyobjects).

So… the stock likely remains in purgatory/range-bound. Spencer has the buyback machine on at $500/share. If we somehow get to $450/share or lower then Netflix gets more interesting on the long side. But as of this morning, we are keeping it on the short bench and will continue to track the data closely for a meaningful inflection.

I don’t see how the stock works on the long side until estimates find a bottom and we see evidence that sub trends are improving.

We're opening up Andrew's Recap of his Q2 2021 Themes complimentary. Click here for access.

Click here to learn more about Communications Pro and get access to Andrew's full hour-long presentation and over 75+ slides.