“Oh, Andy loved geology. I imagine it appealed to his meticulous nature. An ice age here, million years of mountain building there. Geology is the study of pressure and time. That's all it takes really, pressure, and time.”

-Red, The Shawshank Redemption

On a daily basis, we grind through a constant channel of noise. E-mails, instant messages, text messages, Bloomberg messages, and phone calls all can interrupt our train of thought. Generating valuable investment ideas for our clients in real-time requires pressure (effort) and time (focus) so at Hedgeye we value the time we take away from the various stimuli that surround us for so much of the day so that we can share ideas across sectors, discuss ideas with clients, or simply think in solitude. As Keith referenced in his Early Look titled, “AMERICAN SOLITUDE” last week, solitude and leadership often go hand-in-hand.

That said, I think I can speak for everyone at the firm when I state that the unique nature of our business model offers valuable dialogue channels with our clients. The nature of that dialogue can vary broadly, agree or disagree, angry or calm, data based or pure qualitative opinion. The fact is, all of it is critical to our process and all of it is appreciated.

Besides the wide array of views we receive from our exclusive network, the disparate perspectives of our readers are also a key differentiator for our firm. We hear from people managing billions and we hear from people managing a few thousand from their bedroom.

While I am sensitive to the trust our clients have in us, I think it is important to highlight one of the more powerful thoughts that have come across our screens lately:

“What is the relatively small retirement investor to do? He is long stocks--that is what has been taught to him over 80 years. He is long on American patriotism and innovation. He is disgusted with American politics. He is naive on currencies, trade, global economics and the bigger picture. He has income investments that he needs to pay the bills. He lives in fear of the next bubble bursting.”

The reason why I think this thought is powerful is that it highlights a lot of the ideological dogmas that shackle people’s investment perspectives. That is not a criticism, and I am not claiming to be immune to the influence of emotion or groupthink. The best one can do is to be aware of it. The above thought highlights several handcuffs that need to be removed in order to hold as dispassionate and lucid a view of the markets as possible.

1) American Patriotism, while admirable, should not be confused with American Delusion. I love my country (Ireland) as much as the next man. Thinking critically, especially about government and the path of the country, is a necessary feature of a democracy.

2) American innovation is not what it used to be. Some in the media may pine for the days when auto stocks used to “double and double” as soon as “they get going”, but this theme doesn’t sit well with our data-based conviction that Jobless Stagflation (inflation accelerating, growth decelerating) is here to stay.

3) Currencies, trade, global economics and the bigger picture are all part of the same patient that we examine each day. Interconnected markets are here to stay. We strive to fully respect that fact in the positions we hold in the Hedgeye Virtual Portfolio; we are short the Euro and long the Dollar, while being short the S&P 500.

The last sentence of our client’s message is powerful. Living in fear of the next bubble bursting is certainly a powerful engine driving market sentiment. Whether it’s the “relatively small retirement investor” that “needs to pay the bills” or the banker that wants to get paid at year end, fear is a very persuasive mechanism. In the end, we are as grateful to hear the perspectives of our individual investors as we are to hear the views of our most successful PM’s.

In Ben Bernanke’s op-ed in the Washington Post, published yesterday morning, he writes that the dual mandate of helping promote increased employment and sustain price stability compelled the FOMC to announce its intention to buy an additional $600 billion of longer-term Treasury securities by mid-2011.

The introduction to his piece refers to the actions taken by the Federal Reserve and other governments to “stabilize” the crisis in 2008 with a clear aim of claiming legitimacy for further quantitative easing in 2010. In that same vein, I would refer to the uselessness of past forecasts by government employees like Bernanke and Christina Romer, former chairwoman of President Obama’s Council of Economic Advisers (remember the prediction of 8% being the “peak” of unemployment?). When Keith coined the term Quantitative Guessing, he was not being flippant; these people do not – and cannot be expected to – offer anything more than guesswork in their economic forecasts.

What does not involve guesswork is the monitoring of real-time market prices. The impact of QE2 on the markets is clear to see in the data. As the dollar has declined, oil, gold, corn, cotton and many other commodities have seen parabolic moves to the upside. The jobless claims numbers yesterday underscore the dire circumstances that America’s unemployed find themselves in. The actions of the Federal Reserve are not even close to meeting the expectations that the government set. With respect to the “dual mandate” of the Federal Reserve, it is failing on both counts. The consumer is experiencing inflation and job growth has been rather disappointing.

An intuition exists among the American public that I am convinced is lost on many inside the beltway in Washington. The 401(k) is a significant depository of wealth for the American people so the fear of the “relatively small retirement investor” is understandable. That investor can see and hear the realities of the economic situation. The realities of the economy are all around for us to see - 43 million people on foods stamps and growing; a foreclosure crisis that shows no signs of abating and will likely get worse before it gets better. Investing under a cloud of fear of the bubble bursting is exactly the kind of position we do not want our clients to be in. In the end, all it will really take for the “Bernanke Bubble” to burst is pressure and time.

In The Shawshank Redemption, the result of Andy Dufresne’s meticulous application of pressure and time resulted in him burrowing out of a prison over a twenty year period using only a small rock hammer. As those of you who have seen the movie will remember, the prison warden was shocked to say the least. Pressure, sustained by time, can work both ways. In 2010 America, the pressure is being provided by a broken political system, government-sponsored inflation, and a merciless devaluing of the dollar. All else that is required is time.

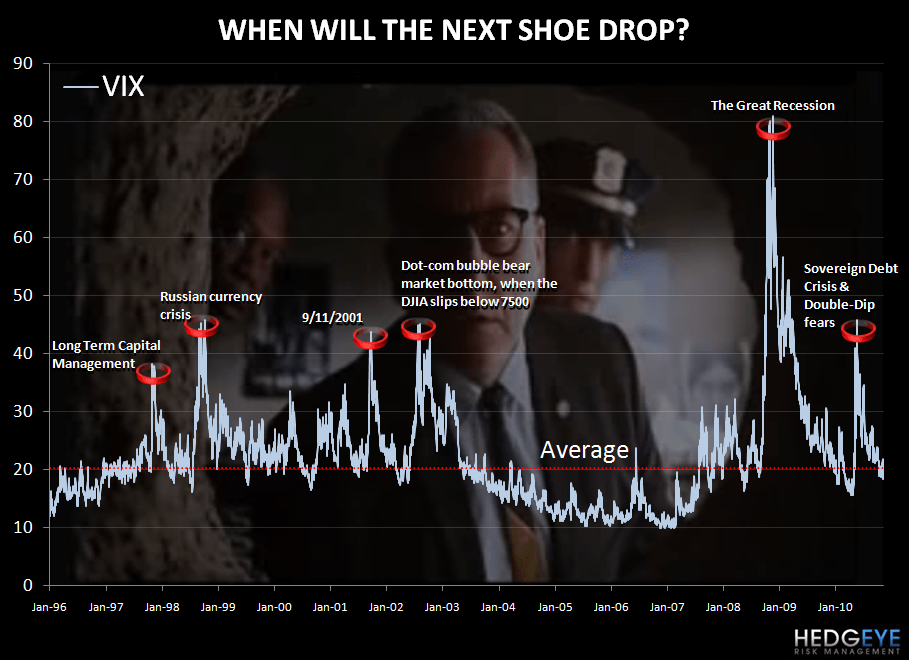

One thing is for sure, we will not be complacent. The last thing we want to do is look like the warden of Shawshank when he realized what had become of Andy Dufresne. As you can see in the chart below, the VIX Index has traded below its 15 year average. Being bearish at this point is not consensus and we are down 2.18% on our short position in the S&P 500. Yesterday’s move was significant but our conviction has not wavered that the largely policy-induced pressure building inside the market is reaching a critical point.

Time is ticking and pressure is growing.

Have a great weekend,

Rory Green