Hedgeye Portfolio: Short EUR-USD via (FXE); Short Italy (EWI)

Conclusion: as the interconnected risk trade in Europe heightens alongside the US Fed’s Quantitative Guessing (QG) decision to pump more dollars into the system, we’re taking the explicit tact to short the EUR versus the USD. Today’s announcement from the ECB and Bank of England to hold benchmark interest rates at their current levels of 1.00% and 0.50% with no comment to explicitly issue their own QE2 packages, while the region pushes through austerity measures, leaves many questions unanswered, including just how these central banks and global governing bodies may need to act in the very near term given the explosion in risk premiums for Europe’s fiscally imbalanced countries, particularly Greece, Ireland, Portugal, Spain and Italy. As we stated in our Q2 2010 quarterly theme of Sovereign Debt Dichotomy, history shows that kicking the can of debt down the road doesn’t end well. In the case of the Eurozone, countries like Ireland are bearing the brunt of the European Monetary Union’s (EMU) constraints, namely the inability to influence monetary policy to lessen debt obligations and market volatility.

Below we highlight the rising risk trade in Europe and the fundamentals behind our bearish view on Italy:

Trading Europe’s Risk Inflection:

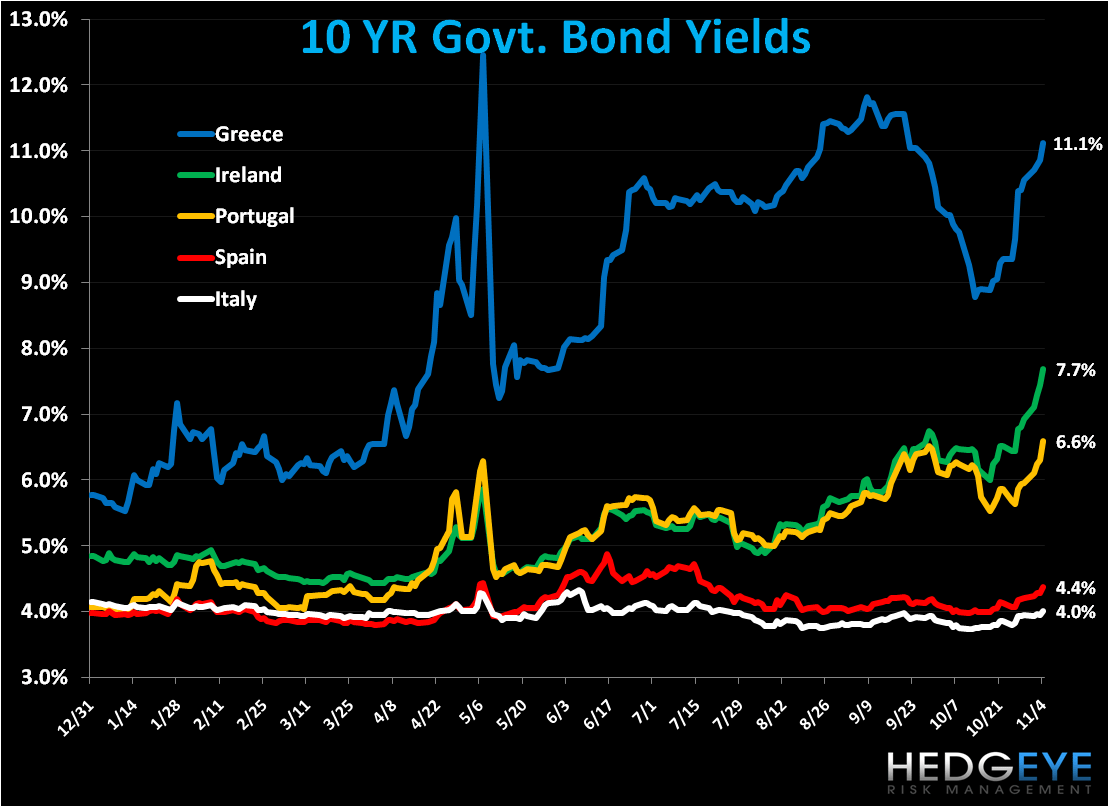

From the recent movement in our Hedgeye Portfolio and our research over the past 10 days, we’ve noted heightening risk for paper across Europe, but particularly for Europe’s fiscally bloated member states. This marked inflection, which we’re measuring via government bond yields and sovereign CDS spreads, has emerged after the month of September and most of October saw risk compress. As the charts below of the 10 YR government bond yields and 5YR CDS spreads demonstrate, risk is blowing out to year-to-date highs (excluding Greece), and therefore we’ve oriented ourselves accordingly!

Below are some of the major macro moves in our Hedgeye Portfolio over the last few days:

11/2/10

9:57am Covered UUP (US Dollar Index Fund) @22.23

11/3/10

3:26pm Sold USO (US Oil Fund) @ $36.67

3:36pm Shorted FXE (EuroTrust Fund) @ $140.55

11/4/10

10:28am Shorted FXE (EuroTrust Fund) @ $142.10

10:16am Shorted EWI (Italy Index Fund) @ $18.34 (*initially shorted on 9/24/10 @ $16.65)

Explicitly we’re playing Europe’s currency risk on the short side versus a bullish view on the USD from a short-term, mean reversion perspective. We think the USD should gain on the back of a Republican victory of the House and next week’s G20 meeting in Seoul (Nov. 11-12) in which global players will put additional pressure on the US to quell further USD debauchment. [As a side note, ECB President Trichet said in a press conference today that he is confident the US is not promoting a weak dollar.]

Our quantitative models suggest the EUR-USD is overbought from an immediate term TRADE duration at $1.42, with TRADE support at $1.39. Our intermediate term TREND line of support is at $1.33.

Returning to the sovereign debt outlook, Ireland is one country that stands out in the charts above. The country is currently the region’s debt poster child, with 2010 debt and deficit levels estimated at 10% and 32% of GDP, respectively. Certainly Ireland has “earned” its reputation after pigging out on low interest rates for nearly a decade, resulting in a severe domestic housing bubble and financial crisis, the latter of which is contributing heavily to its 2010 deficit. While Irish economic ministers have tried to calm investor fears by stating that the country has €20 Billion in cash to fund its debts into April of next year, as the government plans to push through spending cuts and tax hikes worth €6 Billion next year, the market is telling a different story--one of desperation.

We’re of the opinion that Ireland, like Greece, presents risks that could snowball beyond their individual borders. We have not actively taken a position in Greece or Ireland, due to this volatility, however it’s interesting to note that Greece’s bond yields and CDS spreads exploded exponentially over just a few days, which ultimately led Eurozone finance ministers to issue a €110 Billion bailout package for Greece on May 2nd and days later, along with the IMF and World Bank, a €750 Billion package to rescue troubled European nations.

Could Ireland be the next Greece? Certainly the data is pointing in that direction.

----

Italy’s Headwinds

We shorted Italy again today via the etf EWI in the Hedgeye Portfolio, and while our short position is working against us, the fundamentals continue to suggest further economic downside over the intermediate to longer term. We’ve identified three main headwinds:

- Exorbitant debt levels and the magnitude of near-term maturities

- Berlusconi’s divided government

- Aging population

Debt Doldrums

With a debt ratio at 115.2% as of fiscal year 2009, Italy’s debt is of particular concern to us, while its deficit as a percentage of GDP is less worrisome at -5.3%, yet nevertheless above the -3% target rate set by the EMU.

Below we’ve compared the country’s government debt obligations over the next three years. What’s interesting to note is that Italy has a massive obligation over the period, especially next year at €266.6 Billion alone, and its obligations rival those of Germany and France, countries with far larger economies. (Germany’s GDP is ~ 1.6x Italy’s).

If we look at debt maturing over the period as a percent of projected GDP, we find that the PIIGS have a significantly larger share to pay off than their fiscally prudent brothers, especially Germany. While this isn’t a huge surprise, it reinforces the point that countries that want to issue or refinance debt will have to do so in a period of higher costs of capital as yields rise (in some cases to record highs!), which should increase and/or accelerate sovereign default risk.

Berlusconi’s Divide

With regard to Italy we question the country’s ability to materially cut its bloated balance sheet, particularly given the increasingly contentious political backdrop. Remember that back in July PM Silvio Berlusconi expelled his speaker of the Parliament, Gianfranco Fini, and other dissents from his People of the Liberty party, which left his party with a majority coalition.

However, Fini has been increasingly critical of Berlusconi, and rightfully so for Berlusconi continues to make scandalous headlines. The latest scandal concerns his involvement in the release of a teenage belly dancer accused of theft in May.

We view the uncertainty in the government as bearish on the margin. We’ll have our eye on Fini who has found support in both Houses of Parliament and could play an integral role over the next weeks in bringing down Berlusconi’s government.

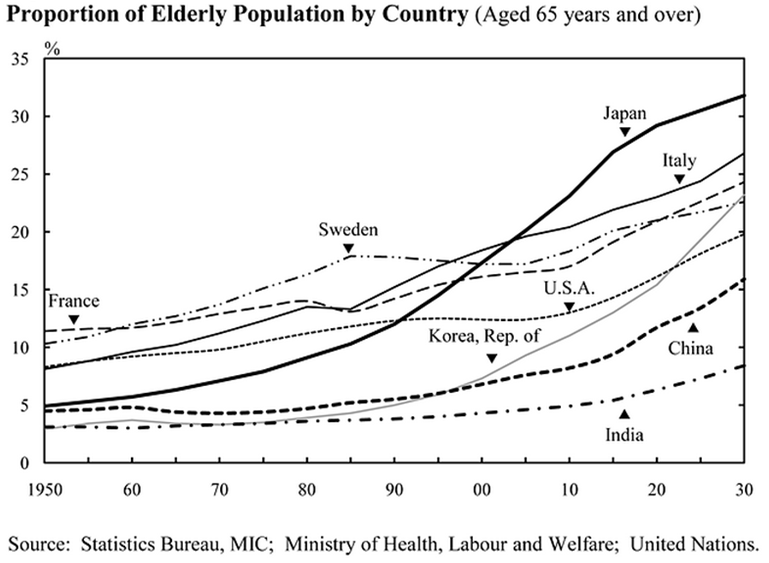

Aging Population

We’ll let the chart below do the talking, but Italy’s aging population must be considered in making an investment position, for it will be a further drag on the social state. The data suggests that in 2015, 21.9% of Italy’s population will be >65, the highest of the Eurozone countries. Moving out to 2020, Italy’s percentage moves to 23.2%, the highest rate of any member country, with Finland and Germany trailing at 22.8% and 22.6% respectively.

Stay tuned as the Macro Team digests the daily interconnected risk.

Matthew Hedrick

Analyst