This note was originally published at 8am this morning, November 04, 2010. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

"It does not require a majority to prevail, but rather an irate, tireless minority keen to set brush fires in people's minds."

-Samuel Adams

While I don’t expect any professional politician in Washington or the manic media that gets paid advertising dollars for stock market cheerleading to call this out for what it is until this stock market is a lot lower, I will. The US Federal Reserve is officially and unequivocally politicized.

Yes, Ben Bernanke himself has admitted that Quantitative Guessing (QG) is “unconventional.” But now he is so politicized that he is compelled to write an Op-Ed for the Washington Post on “What The Fed Did And Why: Supporting The Recovery And Sustaining Price Stability.” The Chinese, Hedgeye, and anyone with real-time market quotes, are sitting here staring at their screens this morning with shock and awe.

The US Dollar is making new lows this morning (down -15% since June!). The modern day Roman Empire’s credibility is burning at the global stake.

Notwithstanding unprecedented timing of the Op-ed (on the day of the Fed’s decision – do you think anyone leaked its contents?), or the fact that the words “US DOLLAR” were not mentioned ONCE in his allegedly objective and politically unbiased analysis, allow me to break down Bernanke’s view for you versus reality:

1. STORYTELLING PREFACE: “Two years have passed since the worst financial crisis since the 1930s…”

KM: That’s always the 1st sentence of the fear-mongering message campaign that will lead you to believe no one notices Wall Street’s 2010 bonus pool.

2. OUTCOME: “These steps helped end the economic free fall and set the stage for a resumption of economic growth in mid-2009…”

KM: Of course, the professional politicians saved us from the crisis they helped create and now we should pay homage to the banks, never earning a rate of return on our hard earned savings again. Fiscal sobriety and conservatism be damned. Get out there and chase some yield folks.

3. MANDATE: “Notwithstanding the progress that has been made…” (we saved you)… “the Federal Reserve’s objectives – its dual mandate, set by Congress – are to promote a high level of employment and low, stable inflation…”

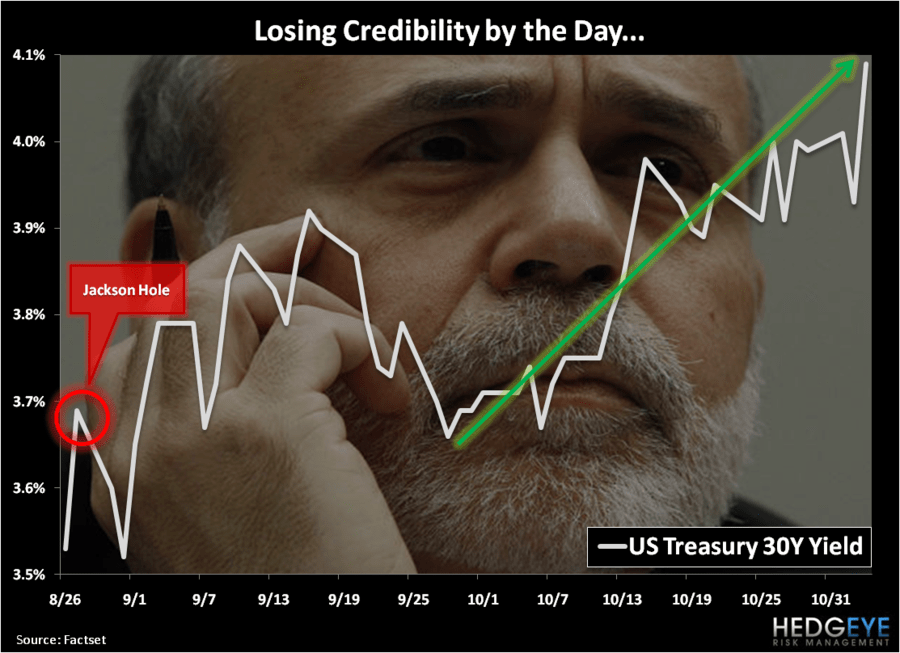

KM: Right, you saved us from the evil-doers and completely screwed up the employment picture by fear-mongering employers to stop hiring. Ok. And now we’re seeing the credibility of the US Dollar collapse and, as a result, global commodity prices hit new YTD highs, DAILY. The CRB Commodities index is up +16.4% since Bernanke’s decision to Burn the Buck on August 27th in Jackson Hole.

4. INFLATION: “Although inflation is generally good, inflation that is too low… can morph into deflation…”

KM: Right, right. China, India, and Australia have raised interest rates in the last few weeks specifically because they (like anyone with real-time quotes) see the inflation implied in expectations. The US Treasury Inflation Protection (TIP) auction yielded -0.55% (lowest EVER) in October (implying outright fear of inflation), but Bernanke keeps Burning the Brush Fire of Fear-Mongering about a great depression that no one in finance has remotely experienced.

5. ECONOMIC STAGNATION: “falling prices and wages, which can contributed to long periods of economic stagnation.”

KM: How about JOBLESS STAGFLATION (sorry PIMCO, we called it first) = US Government sponsored fear-mongering towards employers + inflation. In the 1970s, Jimmy Carter and the Fed’s panderer, Arthur Burns, didn’t get it. This time around, I don’t expect Obama and Bernanke to either. It’s Keynesian theory versus real-time market realities. The problem here isn’t US Consumer reaction to government policy. It’s government policy itself.

6. QE2: “so far looks to be effective again. Stock prices rose and long-term interest rates fell when investors began to anticipate the most recent action… lower mortgages will make housing more affordable … and higher stock prices will boost consumer wealth …”

KM: This is the central narrative fallacy of the Bernanke Brush Fire that really lights up the anxieties of anyone observing growth and inflation data on a globally interconnected basis. Re-read what he’s implying here and your jaw should drop:

A) US Dollar Debauchery – Let’s ignore that chart.

B) Inflation – I’m willfully blind to that chart too and/or whatever any other major country is currently saying on the matter.

C) Stock Market – I fundamentally believe that manipulating its price via investor expectation is what drives this economy.

D) Mortgages – I’m not going to mention that 30-year yields have gone straight UP +65% (from 3.55% to 4.09%) since I moved to QE2 in August.

7. CONFIDENCE: “we are confident that we have the tools to unwind these policies at the appropriate time…”

KM: What a joke. While virtually every central banker in the world (ex the Fiat Fools in Japan and the EU) have hiked interest rates multiple times since the mid-2009 recovery that Bernanke pats himself on the back for, I can assure you that if he couldn’t raise rates with 6% US GDP growth, he’ll likely never be able to “unwind these policies” at any time. Sadly, the global markets may very well do that for him. And that will be it for this QG experiment going bad.

Don’t take my word for it on all of this. I’m just a man who is selling everything and going to cash. Get some real quotes and study the history of countries who attempted to debauch the currency of their citizenry. Then read some Asian newspapers - or something other than the Washington Post.

Overnight, China’s central bank adviser, Xia Bin, said the Fed’s Quantitative Guessing “amounts to uncontrolled money printing.” Even Japan’s bureaucrat PM, Naoto Kan, said this was “the US pursuing weak-dollar policy.” At least those Op-Eds were short and to the point. They also sound just about right.

My immediate term support and resistance levels for the SP500 are now 1186 and 1201, respectively. My SP500 short position (SPY) is -0.96% against me in the Hedgeye Portfolio, and I intend on shorting the market again today on strength. Being early on the short side here is also called being wrong. I get that. I was early in October/November of 2007 too. Remember, market tops are processes, not points.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer