This guest commentary was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst. This piece does not necessarily reflect the opinion of Hedgeye.

On Friday, the Federal Housing Finance Agency (FHFA) announced that Fannie Mae and Freddie Mac (aka “the GSEs”) will eliminate the 50bp Adverse Market Refinance Fee for loan deliveries effective August 1, 2021.

FHFA acting director Sandra Thompson has reversed one of the more controversial aspects of her predecessor’s tenure, a welcome sign of normality at this key agency in the world of residential housing finance.

Meanwhile, just a week earlier, our friends at Ginnie Mae suddenly floated a request for public comment on a bizarre proposal for new issuer eligibility standards that would crush many government lenders.

The announcement came late in the day Friday, meaning that Ginnie Mae buried the request on the website. Indeed, we hear that Ginnie Mae originally planned to release the rule without any request for public comment.

The reaction of the industry to the proposal is first and foremost shock and incredulity, especially after four years of uncertainty under Mark Calabria at FHFA. During COVID, Ginnie Mae and the rest of HUD worked closely with the industry.

But now the industry's trust in the willingness of Ginnie Mae to be a source of stability has been badly compromised by a proposal that seems to lack any cohesion or specific rationale.

The Institutional Risk Analyst spoke to a dozen issuers and mortgage bankers in the past week. Most did not believe that Ginnie Mae could possibly be serious about the proposal.

Specifically, the new requirements for issuers of Ginnie Mae MBS seem ill-considered and would cause much damage to the market for government-insured loans.

“The proposal is so contrary to everything that Ginnie Mae and the FHA have said publicly about protecting the value of the government asset,” one prominent industry leader told The IRA. “For Ginnie Mae to act unilaterally on this issue, without new leadership appointed by President Joe Biden is extraordinary.”

For us, the most striking thing about this proposal is that Ginnie Mae’s risk management team ignores the huge strides made by nonbank mortgage firms to de-lever their balance sheets, pay down bank lines and acquire term financing for working capital and financing MSRs.

Under this rule, the mortgage firms that added to capital over the past year would not invest in MSRs and, indeed, would arguably be sellers of servicing. For this reason alone, the Ginnie Mae proposal makes little sense.

“It does not sound like HUD or Secretary Marcia Fudge were consulted on the decision,” says another CEO in the government market. “This proposal will be problematic for smaller issuers, particularly issuers that serve low income, disadvantaged communities.

All of the small lenders that serve highly specialized communities will be gutted and forced to sell servicing assets for nothing. This rule could cost literally tens of billions in losses to banks and nonbanks alike."

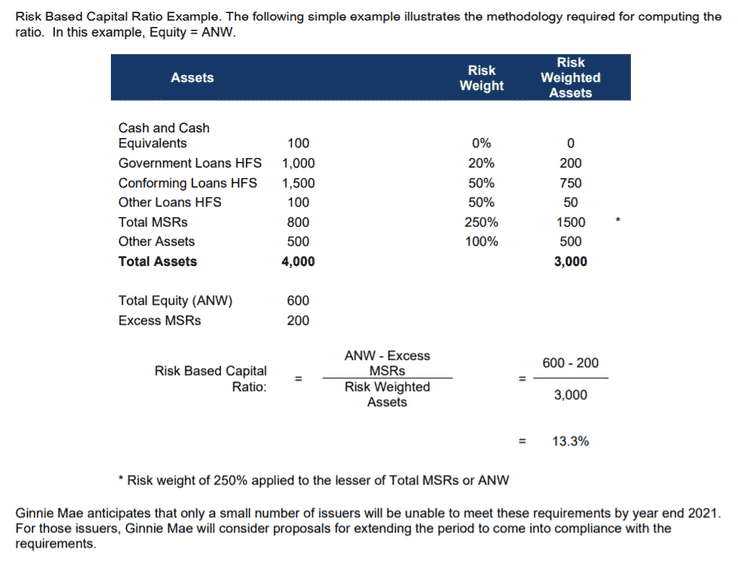

The diagram below illustrates the Ginnie Mae proposal:

First and foremost, the Ginnie Mae proposal penalizes independent mortgage banks (IMBs) for holding MSRs on government-insured loans.

While the proposal is styled as a “risk based” rule, obviously in imitation of the Basle framework for banks, in fact the proposal increases financial risk on the industry while making government servicing assets impossible to hold.

Under the above rule, issuers could own private label MBS or even penny stocks with 5:1 leverage and get better capital treatment than on government MSRs.

The proposal by Ginnie Mae is a significant embarrassment for the agency, if for no other reason than the math behind the numbers makes no sense.

The new rules proposed by the career staff of Ginnie Mae led by Gregory Keith essentially cuts the net worth of most large issuers to 1/3 of the levels calculated under present rules. We are told that Ginnie Mae acted now, before the FHFA acts on its own capital rule, so as to have the regime apply to 2022 issuer financials.

Incredibly, the proposed rule from Ginnie Mae makes it difficult for issuers to employ term debt to finance their business, but then penalizes the ownership of the MSR. The entire proposal illustrates how US policy regarding mortgage issuers has been polluted by the thinking of European regulators, who have a pathological aversion to residential housing finance.

In Europe, for example, payment intangibles such as MSRs do not even exist as assets under IFRS accounting rules. Properly understood, however, MSRs are vital sources of working capital and liquidity for mortgage banks.

Ginnie Mae treats them as a source of risk as do US bank regulators and their counterparts in the EU. Ginnie Mae never actually says what specific risk is driving this process -- other than perhaps the competitive risk to commercial banks posed by more efficient IMBs.

Not only was the MSR given a 250% risk weight under the Ginnie Mae scheme, one executive tells The IRA, but no other assets received this punitive risk weight. Several industry operators told The IRA that the proposal will definitely reduce liquidity in the MSR market.

“To negatively impact excess MSRs makes zero sense,” notes one operator with decades of experience at banks and nonbanks.

“Other than loans held for sale, MSRs are the largest and most valuable capital asset of a mortgage lender.The FHFA calculation of net worth to total assets makes a lot more sense for IMBs. This proposal will hurt issuer profitability and also impact liquidity, which will adversely effect mortgage rates for consumers.”

|

“The basic problem with this proposal comes down to simple math,” notes another industry veteran. “Let’s say you are a mortgage lender and you want to hold MSR. Under this proposal, the most leverage you could put against an MSR would be 30% or half of current levels in the industry. It seems that Ginnie Mae has recognized that MSRs are a risky asset, but reading this supposedly “risk-based” proposal, you’d think that MSRs were the only risky asset. The clear message from Ginnie Mae is do not invest in government servicing assets.” |

“But then you have this bizarre notion of subtracting the excess MSR from the numerator in the capital calculation," continues the executive. "This is the most problematic part of the proposal.It’s hard not to be very critical of Ginnie Mae because this analytical approach simply makes no sense. Anyone who has spent even a little bit of time with the industry data from the MBA knows that under this proposal, many smaller issuers in the government market fail.”

The rule as presented by Ginnie Mae for public comment simply will not work. The “risk based” formula actually reduces industry liquidity by increasing the reserves of IMBs, reserves that the industry cannot use it times of stress, and making government servicing assets worthless.

The mortgage servicing asset, lest we forget, is not only a source of steady cash flow for issuers, but contains embedded optionality in terms of refinance opportunities that is arguably worth more than the fair value of the asset under GAAP. Prudential regulators don't even recognize this extremely valuable optionality, one reason bank lending performance in 1-4s is so poor.

“This is an anti-liquidity proposal,” another prominent Ginnie Mae issuer told The IRA on Friday. “If you really look at where the stress was in the industry last year, it was the REITs. People like Two Harbors (NYSE:TWO) and other hybrid REITs thought that their MBS positions hedged the MSR, but when rates get low enough, the MBS misbehaves too. But instead of focusing on actual risk, Ginnie Mae has decided to reduce the liquidity of all government issuers, large and small.”

The mortgage industry concerns with the proposed Ginnie Mae rule for issuers can be summarized in a couple of points:

-

Risk-based standard: Imposing a bank-like risk-based capital standard for IMBs is a bad idea and does not recognize the difference in sources and uses of capital between depositories and finance companies. Ginnie Mae should encourage IMBs to issue term debt whenever possible and hold government-insured loans and MSRs as a key part of capital.

-

Penalize MSRs: The calculation method excluding certain MSR assets and the 250% “risk weight” for MSRs will destroy the value of government servicing. Given Ginnie Mae’s professed desire to protect value of Ginnie MSRs, why would HUD propose a bank-like capital rule on MSRs? If anything, Ginnie Mae ought to monitor participations in MSRs, but not discourage issuers to retain the asset.

-

Liquidity: The rule penalizes loans held for sale, but does not penalize other assets. Why hold an additional 20bp cash reserve against a government-insured asset that is eligible for pooling into MBS and will be cash in 30 days? Government loans should be zero risk weight and conventionals 20% in line with Basle III, right?? The proposal also penalizes low-risk assets such as prepaid expenses at 100%? Why?

“We are 50 percent below the net worth requirement once the math gets laid out, which is unfathomable to me,” another large issuer told us last Friday. “Ginnie Mae assigns a punitive, 250% risk weight to their own MSR, but then they don’t count term debt in the calculation for capital? That is problematic for every government issuer. We can adjust our business, but the problem is that the math calculations in this rule will be devastating to smaller issuers.”

The combination of changes proposed by Ginnie Mae will make it impossible for IMBs to grow their business.

The prudential regulators, the DOJ and CFPB have already chased the commercial banks out of the government loan market. If now Ginnie Mae chases the independent mortgage banks (IMBs) out, who is going to make government-insured loans or hold government servicing?

Unlike prudential regulators who spend years working with the banking industry on risk-based standards and credit loss benchmarks used for this purpose, Ginnie Mae presents no rational basis for its actions.

They give IMBs credit for cash and take out the grossed-up footing for HECMs and MBS, for example, but there is nothing else "risk based" about this unfortunate proposal.

The REITs that almost went out of business a year ago would look great under the Ginnie Mae proposal, but the government issuers that supported the government market through COVID during 2020 would look awful. One thing Ginnie Mae ought to consider is how many government issuers will be downgraded by Moody’s et al if this proposal goes into effect.

Meanwhile, Ginnie Mae will become entirely dependent upon REITs and banks to own government MSRs as nonbank issuers become mere brokers and sub-servicers. If this proposal were authored by JPMorgan (NYSEJPM) CEO Jamie Dimon and his residential mortgage team, it could not be more perfectly suited to annihilate the non-banks that currently control more than two-thirds of the government loan market.

Not only will this proposal crush the liquidity of government servicing assets, but it will make nonbanks liquidate their portfolios of MSRs into a collapsing market.

But more than any specific point, the real tragedy of this poorly thought-out proposal is that Ginnie Mae has badly damaged its credibility with the mortgage industry.

When you issue a rule that would crush the holders of half of all government MSRs, it tells the people who manage government lenders that you really don’t care about the industry.

The basic political problem facing Ginnie Mae and HUD Secretary Fudge is that they must either withdraw this proposal immediately or continue with a rule that would destroy much of the government loan market.

ABOUT CHRISTOPHER WHALEN

Christopher Whalen is the author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington. Currently, he serves as the editor of The Institutional Risk Analyst.

This piece does not necessarily reflect the opinion of Hedgeye.